Fake NFT Minting Scam (2026): How to Write Off the Loss

By Garrett Taylor, CPA

June 22, 2026 · 10 min read

Key Takeaways

- ✓✓A fake NFT minting scam loss is usually a deductible theft loss under §165(c)(2) when you minted with a profit motive. IRS Chief Counsel Memo 202511015 supports it.

- ✓Fake mint sites charge real crypto for gas and platform fees, show fabricated sales and balances, then block withdrawals behind more fees before disappearing.

- ✓Your deduction is the cost basis of the crypto you actually paid, including gas fees. The fake on-screen sale proceeds are fiction and are not deductible.

- ✓✓Claim the loss in the year of discovery on Form 4684 Section B, then carry it to Schedule A. A theft loss is usually better than a worthless-NFT capital loss.

- ✓Save the mint site, the contract address, your gas-fee transactions, and file an IC3 report. The same records prove the theft and anchor the deduction year.

“The art was never sold and the balance was never real. The only real money was the crypto the creator paid in gas and fees to a contract built to take it.”

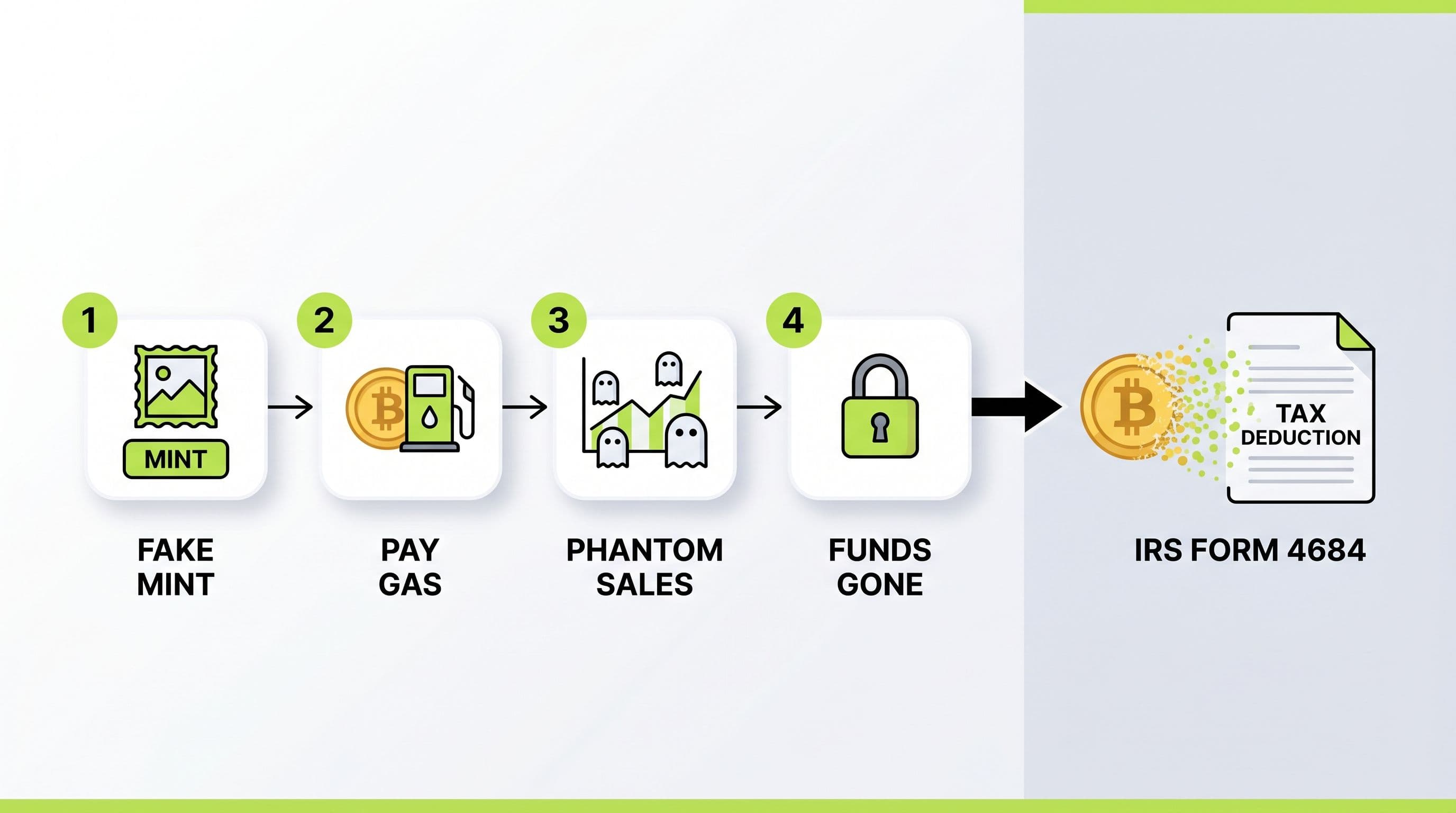

A fake NFT minting scam targets creators and collectors who want to mint and sell digital art. The site promises to handle minting and sales for a fee paid in crypto. You mint, you see sales roll in, the balance grows, and then you cannot withdraw a cent. The sales were fabricated. The fees were real and gone.

Most victims write off the loss as the cost of a bad bet. If you minted as an investment activity, that is often the wrong conclusion. A fake NFT minting scam loss can qualify as a deductible theft loss. This guide explains how the scam works and how the deduction works. For the full framework, see our crypto scam tax deduction guide.

What Is a Fake NFT Minting Scam?

A fake NFT minting scam uses a fraudulent minting platform to extract crypto from creators under the cover of fees. The site looks like a real launchpad. It charges gas and platform fees in crypto to mint your work, then displays fake sales and profits to keep you minting and paying. When you try to cash out the displayed proceeds, the platform demands more fees, taxes, or gas, and ultimately vanishes.

How the Crypto Actually Leaves

There are two common mechanics. In the fee version, you knowingly pay crypto for gas and minting, and the fabricated sales lure you into paying more. In the malicious-contract version, the act of connecting your wallet and approving a mint transaction grants a drainer access, which sweeps your assets. Many fake mint sites blend both.

Pro Tip

**Phantom sales are the tell.** A real marketplace lets you withdraw genuine proceeds without prepaying gas, fees, or taxes to unlock them. If your 'sales' balance keeps rising but every withdrawal triggers another crypto payment, the proceeds are not real.

Who Fake NFT Minting Scams Target

A fake NFT minting scam usually targets creators, not speculators. The victim is an artist or designer who wants to turn their work into sellable NFTs and is willing to pay gas and platform fees to do it. That willingness to pay fees is exactly what the scam exploits. Every fee feels like a normal cost of minting, so paying more never sets off alarms the way a pure investment deposit might.

The fabricated sales add a second hook. Seeing your art 'sell' for real money is intoxicating, and it pushes creators to mint more and pay more gas to capture the demand. The artist ends up funding their own loss one fee at a time, convinced they are scaling a real business.

Because the crypto leaves as fees rather than as one big deposit, victims often underestimate the total. Adding up every gas and platform payment is usually the first time they see the real size of the loss, and the real size of the potential deduction.

Red Flags of a Fake NFT Minting Site

- A minting platform you were invited to privately rather than an established marketplace.

- Fees, gas, or taxes that must be paid in crypto before you can withdraw proceeds.

- A sales balance that climbs quickly with buyers you cannot verify.

- A connect-wallet and approve step pushed with urgency or a countdown.

- No verifiable team, no audited contract, and support that only lives in a chat window.

Is a Fake NFT Minting Loss Tax Deductible?

In most cases, yes, when you minted as an investment or income-producing activity. The crypto you paid in gas and fees was taken through fraud, which is theft, and you parted with it intending to profit from selling NFTs. That puts the loss under §165(c)(2). IRS Chief Counsel Memo 202511015, released in Q1 2025, supports treating crypto scam losses this way.

As with the other scam types, the loss falls under §165(c)(2), the profit-transaction provision, not the personal theft rules the Tax Cuts and Jobs Act suspended through 2025. If you were minting purely as a personal hobby with no profit intent, the analysis is harder, which is why intent matters.

The Three Tests, Applied to Fake NFT Minting

Test 1: Theft Under State Law

Taking your crypto through fabricated sales and bogus fee demands is fraud and false pretenses, which is theft under any state's law. This test is met.

Test 2: Profit Motive

You must have minted with the intent to sell NFTs for profit, not as a pure hobby. A creator paying gas to mint and list work for sale is engaged in a profit-motivated activity, which satisfies the test.

Test 3: Year of Discovery

You claim the loss in the year you discovered the scam with no reasonable prospect of recovery, typically the year withdrawals failed permanently and the platform disappeared.

How Much Can You Deduct? Cost Basis of What You Paid

Your deduction is the cost basis of the crypto you actually paid the platform, including gas and minting fees, reduced by any recovery. The fake sale proceeds the platform displayed never existed and are never deductible.

What counts toward the deduction

| Item | Deductible? |

|---|---|

| Crypto paid in gas and minting fees | Yes, at your cost basis |

| Crypto paid in fake 'withdrawal taxes' | Yes, added to basis of crypto paid |

| The fake on-screen sale proceeds | No, fabricated and never real |

| Assets swept by a malicious mint contract | Yes, theft loss at cost basis |

A Worked Example

Say you are an illustrator. Over two months you pay a fake NFT minting platform the crypto equivalent of $9,000 in gas and platform fees, drawn from crypto that cost you $6,500. The site shows $40,000 in sales. When you try to withdraw, it demands a $2,000 'gas top-up,' which you pay from crypto that cost you $1,500. Then the platform vanishes. Your deductible theft loss is your cost basis in the crypto you paid, which is $6,500 plus $1,500, for $8,000. The $40,000 in sales was fabricated and is not part of the calculation.

You report the $8,000 on Form 4684 Section B in the year you discovered the scam. If it exceeds your income that year, the remainder carries forward under §172.

Theft Loss vs. Worthless NFT

If you simply bought an NFT that later became worthless, that is generally a capital loss when you dispose of it. A fake NFT minting scam is different. The crypto you paid was taken by fraud, which is a theft loss under §165(c)(2) on Form 4684 Section B. A theft loss is usually more favorable than a capital loss because it is an ordinary deduction. If your loss instead came from a fake mint page that drained your wallet on connect, the mechanics overlap with a crypto phishing wallet attack.

How to Report the Loss

- Total the cost basis of all crypto you paid the platform, including gas and any fake fees.

- Report the theft on Form 4684 Section B, with basis in, fair market value after the theft of zero, and any recovery.

- Carry the loss to Schedule A as an itemized deduction, reducing AGI on Form 1040.

- If the loss exceeds income, track the §172 carryforward for future years.

The full reporting walkthrough in the pillar guide applies to NFT minting losses without change.

Documentation You Need

- The minting site URL and full-page screenshots of your account and 'sales.'

- The smart contract address and every gas and fee transaction hash.

- Records showing the crypto you paid and its cost basis.

- Screenshots of the blocked withdrawals and additional fee demands.

- An IC3 report and police report filed soon after discovery.

Pro Tip

**Pull the contract address from the block explorer.** The on-chain record of your gas payments and the mint contract is permanent even after the website is gone. Save those transaction hashes now, because they are the backbone of a defensible theft-loss claim.

Lost Crypto to a Fake NFT Mint? Let's Talk.

If a fake NFT minting platform took your crypto in 2024, 2025, or 2026, you may have a deductible theft loss under §165(c)(2) and IRS Chief Counsel Memo 202511015. I can review the facts and build a defensible position memo. Bring me your details and I will tell you straight whether the deduction works.

Talk to GarrettFrequently Asked Questions

Frequently Asked Questions

Is a fake NFT minting scam loss tax deductible?

In most cases, yes, if you minted with a profit motive. The crypto taken through fraudulent fees and fake sales is a theft loss under §165(c)(2), reported on Form 4684 Section B. IRS Chief Counsel Memo 202511015 supports the position.

How much of an NFT minting scam loss can I deduct?

You deduct the cost basis of the crypto you actually paid, including gas and minting fees, reduced by any recovery. The fake on-screen sale proceeds were never real and are not deductible.

Is this a theft loss or a worthless-NFT capital loss?

It is a theft loss. A worthless NFT you bought and later disposed of is a capital loss, but crypto taken from you by a fraudulent mint platform is a theft loss on Form 4684 Section B, which is usually more favorable.

What if connecting my wallet drained it during the mint?

Then the loss is a theft loss as well, measured at the cost basis of the assets swept. The mechanics overlap with phishing wallet drainers, but the tax treatment under §165(c)(2) is the same.

What year do I claim the loss?

You claim it in the year you discovered the scam with no reasonable prospect of recovery, usually the year withdrawals failed and the platform went offline.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Crypto Scam Tax Deduction (2026): A CPA's Guide to Writing It Off

If you lost crypto to a pig butchering scam, phishing attack, or rug pull, you probably have a deductible loss. IRS Chief Counsel Memo 202511015 made the rules clear in 2025. Most CPAs still won't file it. Here's the framework that works.

Crypto Phishing Scam (2026): Claiming the Wallet-Drain Loss on Your Taxes

A crypto phishing scam can empty a wallet in one signature. If the drained crypto was held for investment, that loss is often deductible. Here is how the theft-loss rules apply and how to claim it.

Fake Crypto Investment Platform Scam (2026): Deducting the Loss

A fake crypto investment platform shows you climbing profits you can never withdraw. If you invested for profit, that loss is often deductible. Here is how the theft-loss rules apply.