The Ultimate Guide to Crypto Tax (2026 Edition)

By Garrett Taylor, CPA

April 30, 2026 · 32 min read · Updated May 1, 2026

Key Takeaways

- ✓The IRS treats cryptocurrency as property. Every sale, trade, or spend is a taxable event reported on Form 8949.

- ✓Starting in 2026, exchanges must issue Form 1099-DA reporting your transactions directly to the IRS.

- ✓Short-term gains are taxed at 10-37%. Long-term gains at 0%, 15%, or 20%.

- ✓Staking, mining, airdrops, and payments in crypto are ordinary income at fair market value when received.

- ✓Wash sale rules do NOT apply to crypto in 2026, making tax-loss harvesting one of the most powerful strategies available.

“This guide has been reviewed for accuracy by Leanne Grant, Enrolled Agent, specializing in cryptocurrency tax compliance and IRS representation.”

Crypto taxes are confusing. You're not imagining it.

The IRS has issued one official notice about crypto taxation (Notice 2014-21), a handful of FAQs, and a revenue ruling about staking. That's it. Twelve years of a multi-trillion-dollar asset class, and the guidance fits on a few pages.

Meanwhile, you're supposed to figure out the tax treatment of your LP position, your staking rewards, your wrapped ETH, and the NFT you bought.

Here's the good news: once you understand the framework, crypto tax isn't actually that complicated. It's just tedious.

In this guide, I'll walk you through everything using real numbers, real examples, and zero hand-waving.

Let's simplify crypto tax.

What's New for Crypto Tax in 2026

Before we dive into the fundamentals, here's what changed this year. If you filed crypto taxes before, these are the updates that matter.

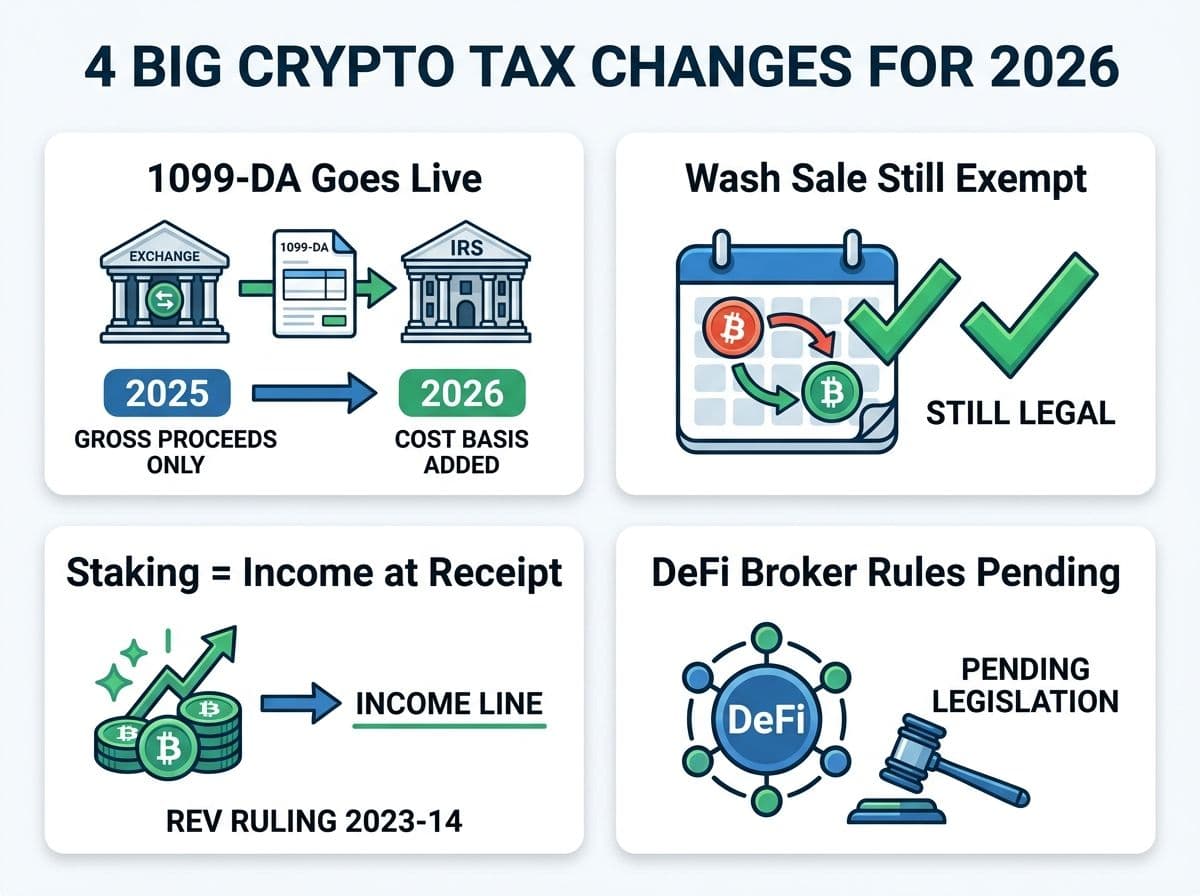

1. Form 1099-DA Goes Live for 2025 Tax Year

This is the biggest change in crypto tax history. Starting with 2025 transactions (reported in 2026), exchanges must issue Form 1099-DA, similar to a 1099-B for stocks. For 2025, exchanges report gross proceeds only. Starting with 2026 transactions, they must also report cost basis if your crypto meets certain requirements.

What this means for you: The IRS will know exactly how much you received from crypto sales. If your return doesn't match, you'll get a CP2000 notice.

2. Wash Sale Proposals (Still Pending)

Multiple bills have proposed extending wash sale rules to crypto, which would prevent you from selling at a loss and immediately rebuying. As of April 2026, none have passed. Crypto is still exempt from wash sale rules. But this could change. This creates a continuing opportunity for tax-loss harvesting strategies in crypto portfolios. That said, transactions should be driven by legitimate investment and profit-motivated objectives rather than solely for tax avoidance purposes, as the IRS may still scrutinize abusive or purely artificial loss-generation activity.

3. Jarrett v. US (Staking Ruling Update)

The Jarrett case challenged whether staking rewards should be taxed at creation or at disposition. The IRS refunded the Jarretts' tax on staking rewards, but then issued Revenue Ruling 2023-14 confirming that staking rewards are taxable as ordinary income when received. The IRS position is clear: staking rewards are ordinary income at receipt.

4. DeFi Broker Rules

The IRS finalized regulations extending broker reporting requirements to DeFi front-end platforms However, this is being challenged legally, and implementation timelines may shift.

The Basics: How the IRS Classifies Crypto

Here's the foundation everything else builds on:

The IRS treats cryptocurrency as property. Not currency. Not a security. Property.

This means every crypto transaction is treated the same as selling a piece of real estate or a trading card. When you sell, trade, or dispose of crypto, you calculate the difference between what you paid (cost basis) and what you received (proceeds). The difference is your capital gain or loss.

This classification comes from IRS Notice 2014-21, and it hasn't changed since. Bitcoin, Ethereum, Solana, meme coins, stablecoins, NFTs, governance tokens are all property.

Why this matters: You can't just report your total crypto gains for the year. You have to report every individual transaction on Form 8949, with the date acquired, date sold, proceeds, cost basis, and gain or loss for each one. For someone with 500 trades, that's 500 line items.

Pro Tip

**This is why crypto tax software exists.** Nobody reports 500 transactions by hand. Tools like Koinly, CoinTracker, and CoinLedger automate the Form 8949 generation.

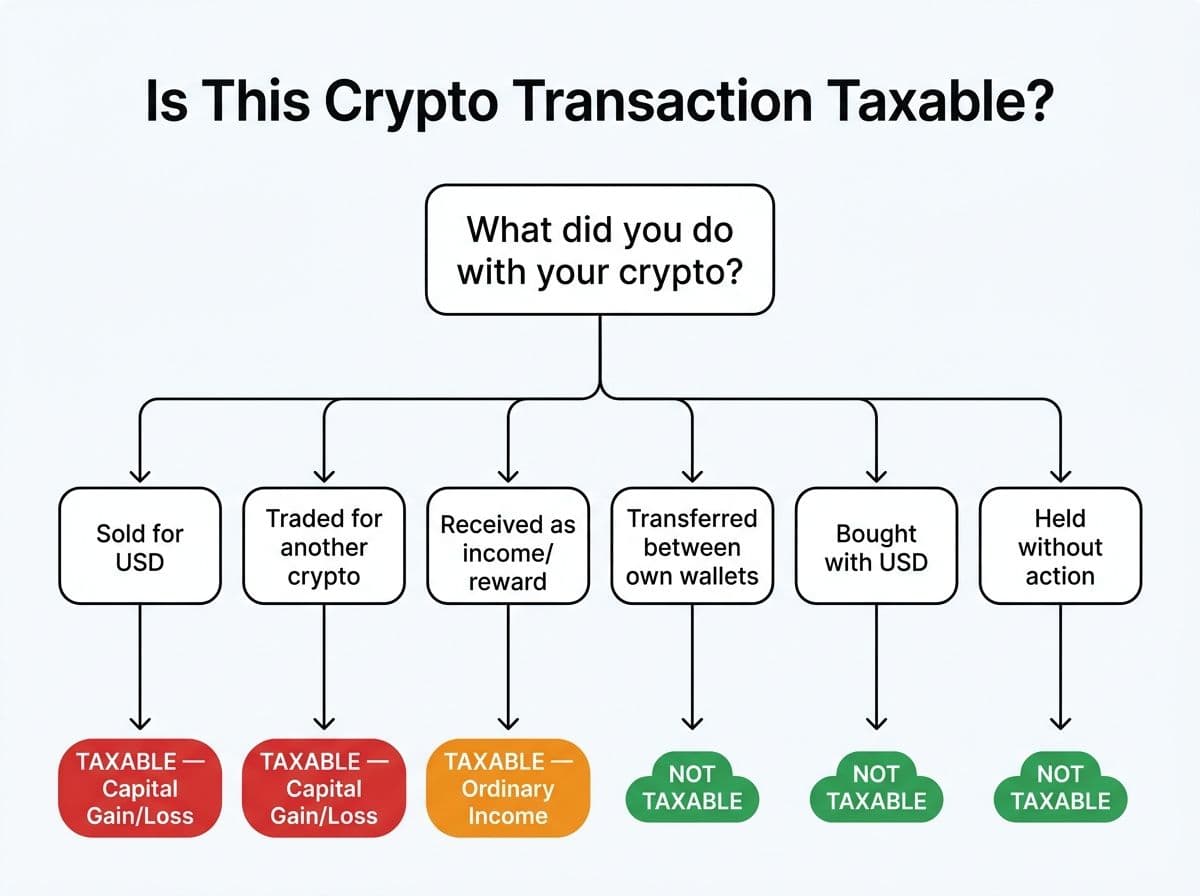

Taxable Events vs. Non-Taxable Events

Not everything you do with crypto triggers a tax. Here's the definitive list.

Crypto Taxable vs Non-Taxable Events

| Taxable (You Owe Tax) | Non-Taxable (No Tax) |

|---|---|

| Selling crypto for USD | Buying crypto with USD |

| Trading one crypto for another (BTC → ETH) | Holding crypto (no disposal) |

| Spending crypto on goods/services | Transferring crypto between your own wallets |

| Receiving crypto as payment for work | Gifting crypto (up to $19,000 per year per recipient in 2026) |

| Mining rewards received | Receiving crypto as a gift |

| Staking rewards received | Donating crypto to a qualified charity |

| Airdrops received | Soft forks (no new tokens received) |

| Hard forks (new tokens received) | Moving crypto between exchanges |

| Earning yield/interest on crypto | Buying crypto with another fiat currency |

| Selling NFTs | |

| Liquidity pool fees earned |

The key principle: If you dispose of crypto (sell, trade, spend) or receive crypto as compensation/rewards, you owe tax. If you're just buying, holding, or moving crypto between your own accounts, no tax is triggered.

Worked example:

You bought 2 ETH at $2,000 each in January 2025 ($4,000 total). In June, you traded 1 ETH for 0.05 BTC when ETH was worth $3,200. In November, you sent your remaining 1 ETH from Coinbase to your Ledger wallet.

- January purchase: Not taxable. You're just buying.

- June trade: Taxable. You disposed of 1 ETH. Your gain is $3,200 (FMV at trade) minus $2,000 (cost basis) = $1,200 capital gain. Short-term because you held less than 1 year.

- November transfer: Not taxable. You're moving crypto between your own wallets.

Cost Basis Methods Explained

Your cost basis is what you paid for a crypto asset. When you sell, your gain or loss is:

Proceeds - Cost Basis = Capital Gain (or Loss)

Simple in theory. Complex in practice, because you probably bought the same crypto at different prices over time.

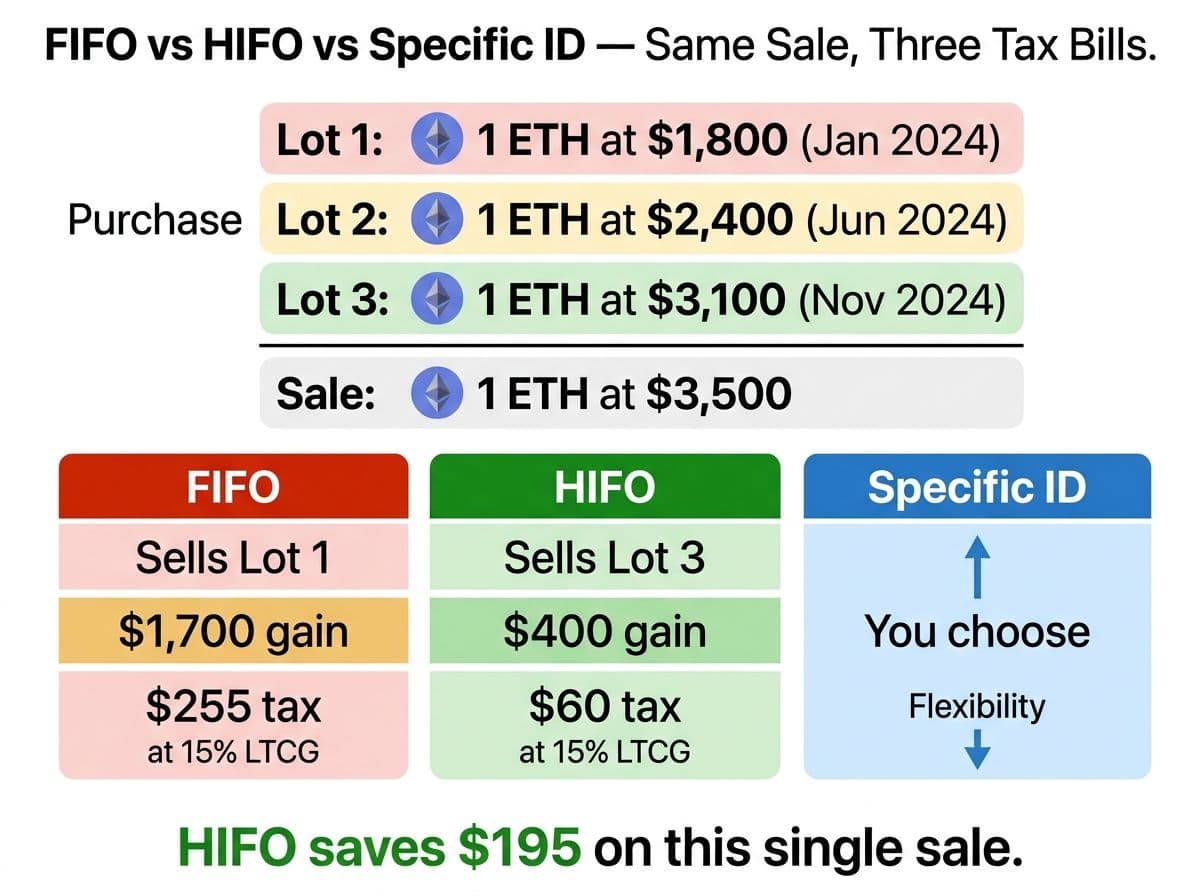

Example: You bought ETH three times:

- Lot 1: 1 ETH at $1,800 (January 2024)

- Lot 2: 1 ETH at $2,400 (June 2024)

- Lot 3: 1 ETH at $3,100 (November 2024)

Now you sell 1 ETH at $3,500 (July 2025). Which lot are you selling?

FIFO (First In, First Out)

You sell the oldest lot first. Selling Lot 1: $3,500 - $1,800 = $1,700 gain. Long-term (held over 1 year), so taxed at 0-20%.

HIFO (Highest In, First Out)

You sell the highest-cost lot first. Selling Lot 3: $3,500 - $3,100 = $400 gain. Short-term, but much smaller gain. (on chart it shows long term rate)

Specific Identification

You choose which lot to sell. Maximum control. You might pick Lot 2 if it produces a long-term gain at a moderate amount.

Pro Tip

We use HIFO for most clients because it minimizes current-year tax. But Specific ID gives us the most flexibility. FIFO is the default if you don't elect a method, and it's almost never the optimal choice. **Talk to your CPA about this before filing.** The right method can save you thousands.

Pro Tip

Once you choose a method and file with it, the IRS expects consistency. You can change methods, but don’tflip between FIFO and HIFO year to year without professional guidance.

Capital Gains: Short-Term vs. Long-Term

How long you hold crypto before selling determines your tax rate.

Short-term capital gains (held 1 year or less): Taxed at your ordinary income tax rate (10%-37%).

Long-term capital gains (held more than 1 year): Taxed at preferential federal tax rates of 0%, 15%, or 20%.

2026 Long-Term Capital Gains Tax Rates (federal)

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $49,450 | $49,451 - $545,500 | Over $545,501 |

| Married Filing Jointly | Up to $98,900 | $98,901 - $613,700 | Over $613,700 |

| Head of Household | Up to $66,200 | $66,201 - $579,600 | Over $579,601 |

| Married Filing Separately | Up to $49,450 | $49,451 - $306,850 | Over $306,851 |

Plus: If your modified adjusted gross income exceeds $200,000 (single or HOH), $125,000 (MFS) or $250,000 (MFJ), you owe an additional 3.8% Net Investment Income Tax (NIIT) on top of any applicable capital gains tax.

Worked example:

You're single with $120,000 in W-2 income. You sell BTC you held for 14 months and realize a $50,000 long-term capital gain.

Your long-term capital gains are taxed at 15%,resulting in approximately $7,500 of federal tax. Your total income ($170,000) is under the NIIT threshold, so you would not owe the additional 3.8% Net Investment Income Tax (NIIT).

Now imagine you sold after holding the BTC for only 10 months instead. Because the gain is short-term, it is taxed at ordinary income tax rates.If taxed at a 24% ordinary income tax rate, the same $50,000 would reslt in approximately $12,000 of federal taxThat's roughly $4,500 more in tax just for selling 4 months early.

$4,500

potential tax savings on a $50,000 gain by holding crypto for more than one year (long-term vs short-term rate differential at the 24% bracket).

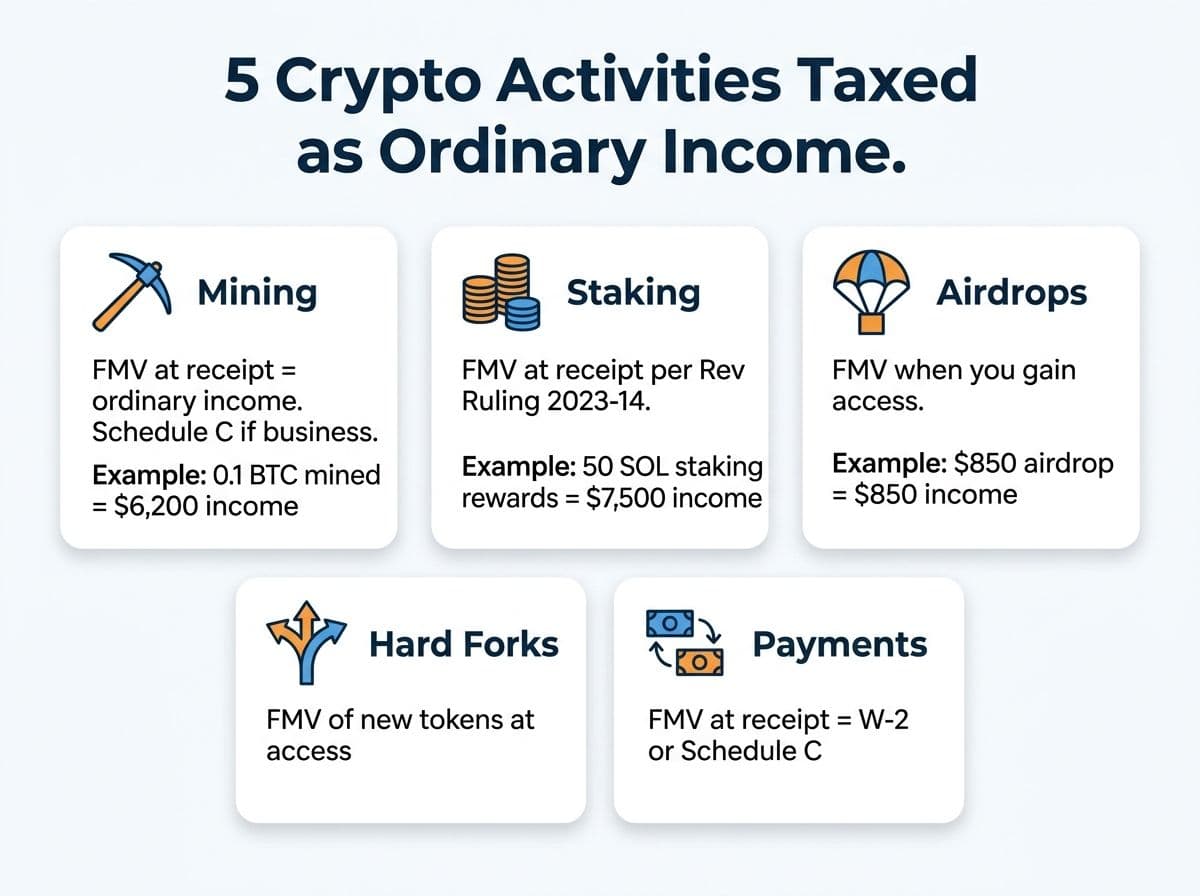

Ordinary Income Events: Mining, Staking, Airdrops, and More

Not all crypto tax is capital gains. These events are taxed as ordinary income at your regular tax rate:

Mining Income

If you mine crypto, the fair market value of tokens at the time you receive them is ordinary income. If mining is your trade or business, report on Schedule C and pay self-employment tax (15.3%). If it's a hobby, report on Schedule 1.

Example: You mine 0.1 BTC over the year. At the time of each mining reward, BTC is worth various amounts totaling $6,200 in FMV. You report $6,200 as mining income.

Staking Rewards

Per Revenue Ruling 2023-14 and the Jarrett v. US outcome, staking rewards are taxable as ordinary income at the FMV when you receive them. When you later sell the staked tokens, you recognize a capital gain or loss based on the difference between your cost basis ( the FMV recognized as income when received) and the sale price.

Example: You stake ETH and earn 0.5 ETH in rewards. At receipt, ETH is worth $3,000. You report $1,500 as staking income. Your cost basis in those 0.5 ETH is $1,500. If you later sell at $3,500 per ETH, you have a $250 capital gain.

Airdrops

Airdrops are ordinary income at FMV when you gain dominion and control over the tokens. If you can access them, they're income — even if you didn't ask for them.

Hard Forks

When a hard fork creates new tokens you can access, the FMV at the time of receipt is ordinary income. Your cost basis in the new tokens is the FMV reported as income.

Crypto as Payment

If you receive crypto as payment for goods or services, the FMV at the time of receipt is ordinary income. For employees, it should appear on your W-2. For contractors, report on Schedule C.

DeFi Tax Treatment

DeFi is the most complex area of crypto taxation. The IRS hasn't issued specific DeFi guidance, so we rely on existing tax principles applied to new technology. Here's how we handle it in our practice.

Token Swaps (DEX Trading)

Trading one token for another on a DEX (Uniswap, Jupiter, etc.) is a taxable event, same as on a centralized exchange. The gain or loss is calculated on the token you disposed of.

Liquidity Pool (“LP”) Deposits and Withdrawals

Adding liquidity: When you deposit tokens into an LP, you receive LP tokens in return. The prevailing CPA position is that this is a taxable event and will be treated as a trade.

Removing liquidity: When you withdraw liquidity, you surrender (dispose of) your LP tokens in exchange for the underlying assets in the pool. If LP deposits are treated as taxable exchanges, then LP withdrawals are generally treated as taxable dispositions as well. Any difference between your adjusted basis in the LP tokens and the fair market value of the tokens received upon withdrawal would generally result in a capital gain or loss.

LP fees earned: Fees that accumulate in the pool are likely taxed as ordinary income when claimed or when they increase your share.

Yield Farming

Tokens earned through yield farming (governance tokens, reward tokens) are ordinary income at FMV when received. When you later sell those reward tokens, you pay capital gains on the change in value.

Bridging (ETH on Ethereum → ETH on Arbitrum): More debatable. Cross-token bridges (ETH → bridged-ETH with a different contract) may be trades subject to capital gains tax. It depends on the situation.

Lending and Borrowing

Lending: Interest earned is ordinary income at FMV when received. Returning principal is not taxable.

Borrowing: Taking a loan against your crypto is not a taxable event (you haven't disposed of anything). But if your collateral gets liquidated, that's a taxable disposal.

NFT Taxes

NFTs are property for tax purposes, but they have unique complications.

Buying an NFT with Crypto

This is two events: (1) you disposed of the crypto used to buy (capital gain/loss), and (2) you acquired the NFT with a cost basis equal to the FMV at purchase.

Selling an NFT

The gain or loss is the sale price minus your cost basis. Standard capital gains rates apply based on holding period.

The 28% Collectibles Question

Are NFTs collectibles? If so, long-term capital gains are taxed at a maximum of 28% instead of the standard 20%. The IRS hasn't definitively ruled on all NFTs, but Notice 2023-27 indicated that certain NFTs may be treated as collectibles (specifically digital art and similar items).

If your crypto is lost, stolen, or becomes worthless, you may still be able to claim a tax deduction, but the rules are nuanced and continue to evolve. The IRS’s 2025 digital asset tax guidance memo reinforced that taxpayers must carefully document losses and establish that the activity was entered into with a profit motive.

Theft and Scam Losses

Since the Tax Cuts and Jobs Act (2018), personal theft losses are generally deductible only if they result from a federally declared disaster. As a result, many individual crypto thefts, hacks, phishing attacks, and rug pulls are not deductible as personal casualty losses.

However, crypto held for investment or profit may still give rise to a deductible loss in certain situations. The 2025 IRS tax memo emphasized that losses connected to transactions entered into for profit may qualify for deduction under existing tax principles, even where the loss results from fraud or scams. Taxpayers should maintain clear documentation showing the investment intent, the nature of the scam or theft, and the amount lost.

If you are operating a crypto-related business, such as a mining operation or qualifying trading business, theft losses connected to the business may also be deductible on Schedule C.

NFT Creator Taxes

If you create and sell NFTs, the income is likely ordinary income (self-employment), not capital gains. Report on Schedule C. You owe self-employment tax.

Royalties

Ongoing royalties from NFT secondary sales are ordinary income when received.

Stablecoin Transactions

Yes, stablecoin transactions can be taxable.

USDC, USDT, DAI, and other stablecoins are property for tax purposes. Trading one stablecoin for another (USDC → USDT) is technically a taxable event. In practice, the gain or loss is usually near zero, but you still need to report it.

Where stablecoins create real tax events:

- Swapping crypto for USDC = selling crypto (gain/loss on the crypto)

- Earning interest on stablecoins = ordinary income

- A stablecoin depegging and selling at a loss = capital loss (looking at you, UST)

Pro Tip

Yes, every USDC-to-USDT swap is technically reportable. In practice, if the gain/loss is a few cents per transaction, most CPAs report them but acknowledge the gain is de minimis. The IRS is unlikely to pursue you for a $0.02 gain on a stablecoin swap. But, you should report it.

Lost, Stolen, and Worthless Crypto

Since the Tax Cuts and Jobs Act (2018), theft losses for individuals are only deductible if the theft qualifies as a federally declared disaster. Recently, the IRS released Chief Counsel Advice Memorandum 202511015, which provides guidance on what crypto scam losses may qualify as deductible losses under IRC § 165.

Worthless Crypto

If a token goes to zero and is truly worthless (no trading volume, project abandoned), you can claim a capital loss by "abandoning" the property. Document when and why you determined it was worthless. Some practitioners recommend selling the dust for a negligible amount to create a clear disposal event.

Example: You bought $5,000 of a token that rug-pulled. It's now untradeable and worth $0. You document the abandonment and claim a $5,000 capital loss.

Gifting and Donating Crypto

Gifting

You can gift up to $19,000 per person per year (2026) without gift tax implications. The recipient takes your cost basis and holding period (carryover basis). If the FMV at gift is less than your basis, special rules apply.

Tax planning angle: Gifting appreciated crypto to family members in lower tax brackets can reduce overall family tax burden. Any future gain recognized may be taxed at the recipient’s lower tax rate.

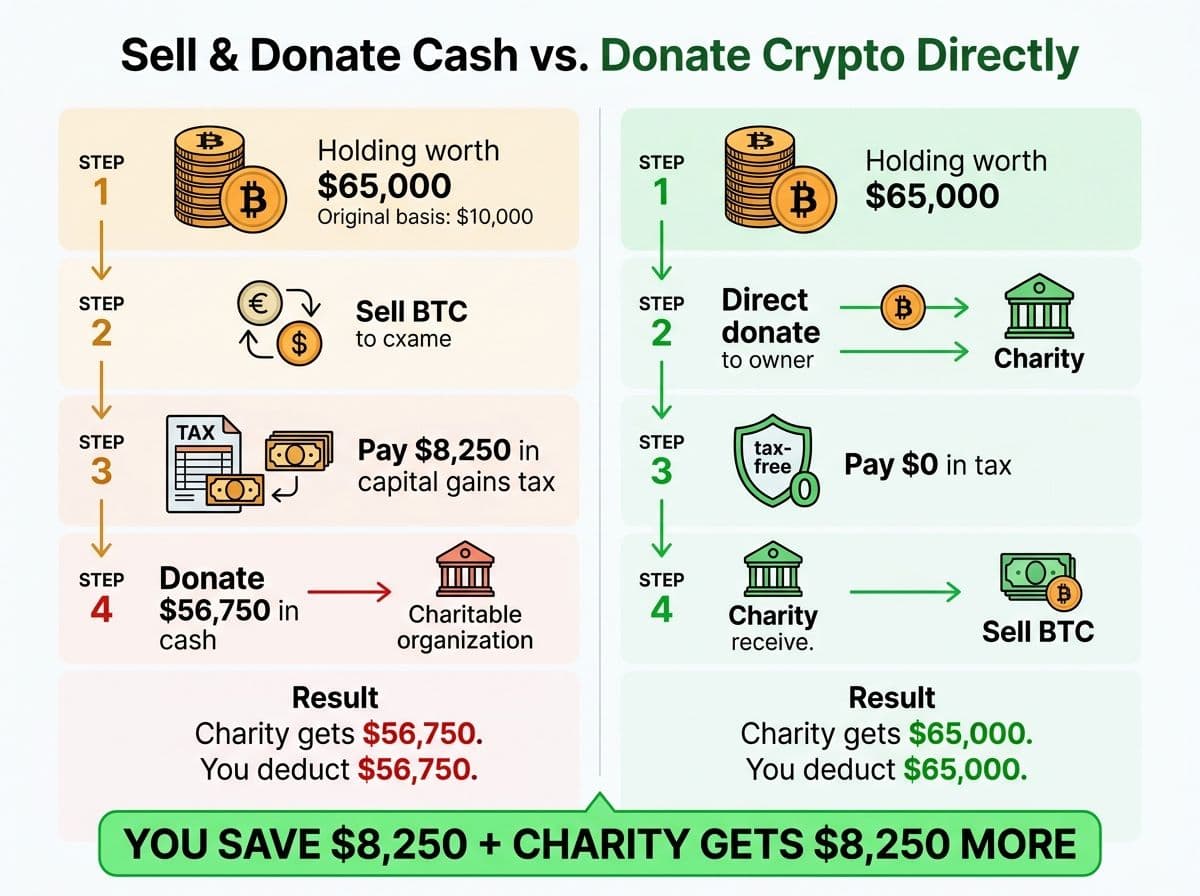

Donating to Charity

Donating appreciated crypto held over 1 year to a qualified 501(c)(3) lets you deduct the full FMV without paying capital gains on the appreciation. This is one of the most tax-efficient charitable giving strategies available.

Example: You bought 1 BTC at $10,000. It's now worth $65,000. If you sell and donate the cash, you owe ~$8,250 in capital gains tax (15% on $55,000), then donate $56,750. If you donate the BTC directly, you deduct the full $65,000 and pay $0 in capital gains. You save $8,250 and the charity gets more.

$8,250

tax savings by donating appreciated BTC directly to charity instead of selling first, on a $55,000 gain at 15% long-term capital gains rate.

Reporting Forms Walkthrough

Here's exactly which forms you need and what goes where.

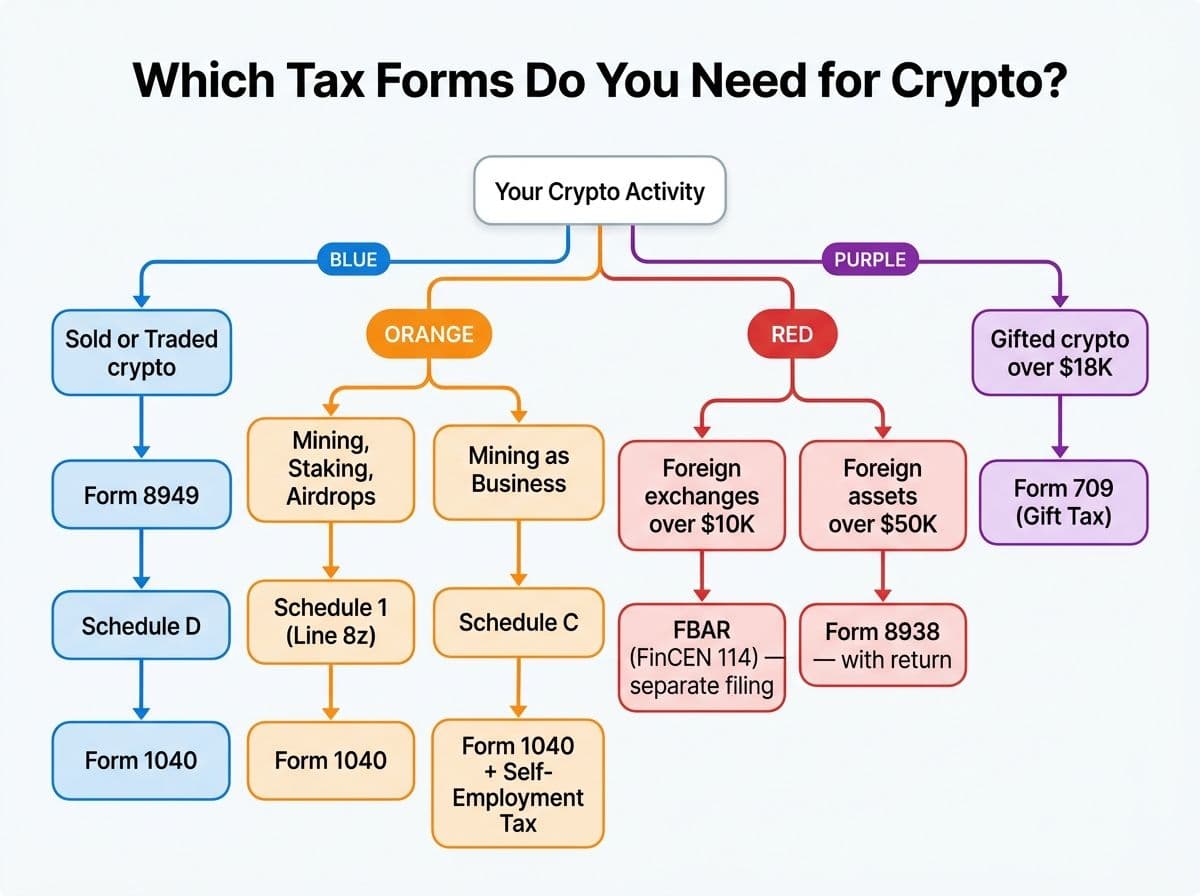

Form 8949 — Sales and Other Dispositions of Capital Assets

Every individual crypto transaction gets its own line on Form 8949. Columns include: description, date acquired, date sold, proceeds, cost basis, and gain or loss. If you have 500 transactions, that's 500 lines.

Schedule D — Capital Gains and Losses

Summary form. Totals from Form 8949 flow here. Reports your net short-term and long-term capital gains.

Schedule 1 — Additional Income

Mining income (non-business), staking rewards, airdrops, and other crypto income go on Schedule 1, Line 8z (Other income).

Schedule C — Profit or Loss from Business

If mining, staking, or NFT creation is your trade or business. Reports revenue and deductible expenses. Triggers self-employment tax (15.3%).

FBAR (FinCEN Form 114) — Foreign Bank Accounts

If you hold crypto on a foreign exchange (Binance, Bybit, KuCoin, etc.) and the aggregate value of all foreign financial accounts exceeds $10,000 at any point during the year, it is recommended to file an FBAR. This is a separate filing with FinCEN, not the IRS. Penalties for non-filing are severe: $10,000+ per violation.

Form 8938 — Statement of Specified Foreign Financial Assets

Similar to FBAR but filed with your tax return and has higher thresholds ($50,000 for single, $100,000 for MFJ at year-end). Some foreign exchanges may trigger this requirement.

Pro Tip

**Do not skip the FBAR.** If you traded on Binance (not Binance.US), Bybit, KuCoin, MEXC, or any non-US exchange and had over $10,000 in total foreign account value, you have an FBAR filing obligation. Penalties for willful non-filing can reach $100,000 or 50% of account balance per year. This is one of the most commonly missed crypto tax obligations.

[Internal link: How to Choose a Crypto Tax CPA → /blog/how-to-choose-crypto-tax-cpa] (links don't work)

Penalties and How to Fix Prior Years

What happens if you don't file crypto taxes?

Failure to file penalty: 5% of unpaid tax per month, up to 25% maximum.

Failure to pay penalty: 0.5% of unpaid tax per month, up to 25% maximum.

Accuracy-related penalty: 20% of the underpayment if the IRS determines negligence or substantial understatement.

Fraud penalty: 75% of the underpayment if the IRS determines intentional fraud.

Criminal penalties: Up to $250,000 and 5 years in prison for willful tax evasion. (This is rare but real — the IRS has a dedicated crypto enforcement team.)

How to fix prior years

Step 1: Gather all your historical transaction data. Go back to every exchange you've ever used and download complete history.

Step 2: Run the data through crypto tax software to calculate gains, losses, and income for each prior year.

Step 3: File amended returns (Form 1040-X) for each year that needs correction.

Step 4: Apply for penalty abatement using "reasonable cause" (first-time penalty abatement, or argue that the complexity and lack of IRS guidance constitutes reasonable cause).

Step 5: Pay any back taxes owed. The IRS offers installment agreements if you can't pay in full.

Pro Tip

**Voluntary disclosure is almost always better than waiting.** If you have unreported crypto from prior years, coming forward voluntarily dramatically reduces your penalty exposure compared to getting caught. We've helped dozens of clients through this process. The IRS treats voluntary disclosers far more favorably than those caught through 1099-DA matching.

State-by-State Crypto Tax Notes

Most states follow federal treatment, but there are important exceptions:

No state income tax: Alaska, Florida, Nevada, New Hampshire (dividends/interest only), South Dakota, Tennessee (dividends/interest only), Texas, Washington, Wyoming. If you live here, you only owe federal crypto tax.

California: Follows federal treatment but has the highest state income tax rate (13.3%). No special crypto provisions. All crypto gains are taxed at ordinary income rates at the state level (California doesn't distinguish between short and long-term capital gains).

New York: Follows federal treatment. State income tax up to 10.9%, plus NYC residents face an additional 3.876%.

States watching: Several states are considering crypto-specific legislation, including digital asset exemptions and mining incentives. Colorado and Wyoming are generally the most crypto-friendly.

International and Expat Considerations

FBAR and Form 8938

If you use foreign exchanges (any exchange not based in the US), you may have FBAR and Form 8938 filing obligations. See the Reporting Forms section above.

US Expats

US citizens and green card holders owe US tax on worldwide income, including crypto gains, regardless of where they live. You may qualify for the Foreign Earned Income Exclusion on employment income, but this does not apply to capital gains or investment income from crypto.

Foreign Tax Credits

If you pay tax on crypto gains in another country, you may be able to claim a foreign tax credit against your US tax liability to avoid double taxation.

Glossary

Cost Basis: What you paid for a crypto asset, including fees. Used to calculate capital gain or loss when you sell.

Capital Gain: The profit when you sell crypto for more than your cost basis.

Capital Loss: The loss when you sell crypto for less than your cost basis. Can offset gains and up to $3,000 of ordinary income per year. Unused losses carry forward indefinitely.

FIFO: First In, First Out. The oldest lot is sold first.

HIFO: Highest In, First Out. The highest-cost lot is sold first (usually minimizes current-year tax).

Specific Identification: You choose which lot to sell.

Fair Market Value (FMV): The price at which crypto would trade between a willing buyer and seller.

Taxable Event: Any crypto action that triggers a tax obligation (sale, trade, spend, receive as income).

1099-DA: New tax form (2025+) that exchanges must issue reporting your crypto transactions.

CP2000: An IRS notice proposing changes to your return based on information they received that doesn't match what you filed.

Wash Sale: Selling at a loss and rebuying within 30 days. Currently does NOT apply to crypto.

Free Crypto Tax Health Check

Not sure where you stand? Send us your exchange data and we'll tell you exactly what you owe, what you've been missing, and how to optimize. 15-minute call, no commitment, no sales pitch.

Book Your Free ReviewFrequently Asked Questions

Do I have to pay taxes on crypto?

Yes. The IRS treats cryptocurrency as property. Every time you sell, trade, or spend crypto, you realize a capital gain or loss that must be reported.

How much tax do I owe on crypto?

Short-term gains (held under 1 year) are taxed at 10-37% federally. Long-term gains (over 1 year) at 0%, 15%, or 20% federally. Plus 3.8% NIIT if income exceeds $200K single.

What happens if I don't report crypto on my taxes?

The IRS receives data from exchanges via 1099-DA. If they find unreported income, you'll get a CP2000 notice plus penalties ranging from 5-75%.

Is trading one crypto for another taxable?

Yes. Swapping BTC for ETH is a taxable event. You must calculate gain or loss on the crypto you disposed of.

Are staking rewards taxed?

Yes. Per Revenue Ruling 2023-14, staking rewards are ordinary income at fair market value when received.

Do wash sale rules apply to crypto?

Not currently. As of April 2026, crypto is exempt from wash sale rules, meaning you can sell at a loss and immediately rebuy.

What is Form 1099-DA?

A new tax form starting 2025 requiring exchanges to report crypto transactions to the IRS. For 2026 transactions, cost basis reporting is also required.

Do I need to report crypto if I just held?

No taxable event if you only bought and held without selling, trading, or earning rewards. But you must answer Yes to the 1040 crypto question.

Is donating crypto tax-deductible?

Yes. Donating appreciated crypto held over 1 year lets you deduct full FMV without paying capital gains on the appreciation.

Do I have to file an FBAR for foreign crypto exchanges?

If aggregate foreign account values exceed $10,000 at any point during the year, you must file FinCEN Form 114. Penalties for non-filing are severe.

Can I deduct crypto losses?

Yes. Capital losses offset gains dollar-for-dollar. Excess losses deduct up to $3,000 of ordinary income per year, with unlimited carryforward.

How does the IRS know I have crypto?

Via 1099-DA reporting, John Doe summonses to exchanges, and Operation Hidden Treasure. With 1099-DA matching, hiding crypto is nearly impossible.

What's the best cost basis method for crypto?

HIFO minimizes current-year tax. Specific ID gives maximum flexibility. FIFO is the default but almost never optimal. Consult a CPA.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

How to Choose a Crypto Tax CPA in 2026 (From a CPA Who Files 500+ Crypto Returns a Year)

A CPA's guide to finding the right crypto tax professional. 10 interview questions, real pricing, red flags, and when you need a CPA vs EA vs tax attorney.

Best Crypto Tax Software 2026: A CPA's Honest Review of Every Major Platform

A CPA who files 500+ crypto returns reviews Koinly, CoinTracker, CoinLedger, CoinTracking, ZenLedger, and Summ. No affiliate links. Just honest verdicts.

Koinly Guide: A Crypto Tax CPA's Complete Walkthrough (2026)

A CPA's step-by-step Koinly walkthrough. Learn how to set up Koinly, avoid the 7 most common errors, and know when DIY is enough vs. when you need a pro.