The New Gambling Loss Deduction Rules (2026): The 90% Cap, the Itemizing Trap, and What It Means for Event Contract Traders

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓The One Big Beautiful Bill Act amended Section 165(d) so gambling losses are deductible only up to 90% of losses, capped at winnings, for tax years beginning after December 31, 2025. A break-even year now produces taxable income.

- ✓The deduction is still itemizers-only. With the 2026 standard deduction at $16,100 single and $32,200 married filing jointly, most casual gamblers deduct zero losses, cap or no cap.

- ✓Professional gamblers get hit twice: the TCJA rule folding business expenses into wagering losses is now permanent, and the 90% cap applies to the combined total on Schedule C.

- ✓The cap only applies to losses characterized as gambling. Capital losses on crypto and losses on event contracts filed under ordinary or capital treatment net in full, which makes characterization the highest-stakes question in prediction market taxes.

- ✓Congress has not fixed it. The FAIR BET Act, which would restore the 100% deduction, was blocked in the House, so the 90% cap governs 2026 unless something changes.

Quick answer: Starting with tax years beginning after December 31, 2025, the One Big Beautiful Bill Act rewrote Section 165(d): your gambling loss deduction is now capped at 90% of your losses, and it still cannot exceed your winnings. Break exactly even on $50,000 of wins and $50,000 of losses in 2026 and you deduct only $45,000, leaving $5,000 of taxable phantom income. The deduction also remains itemizers-only, so the majority of taxpayers who take the standard deduction still deduct nothing at all. The cap first hits 2026 returns filed in early 2027; 2025 returns are unaffected. Professional gamblers are caught too, because business expenses now count inside the capped amount. For prediction market and event contract traders, the cap raises the stakes of an old question: if your contracts are financial instruments rather than wagers, none of this applies to you. This guide runs the math on all of it.

For over a century, the deal between gamblers and the tax code was simple, if unforgiving: winnings are income, losses deduct against winnings if you itemize, and you can never deduct your way below zero.

That deal ended on January 1, 2026, and a lot of people who bet, trade event contracts, or do both have not noticed yet. They will notice at filing time in early 2027, when a break-even year produces a tax bill.

Here's the deal: the gambling loss deduction is now capped at 90% of losses, and the cap lands hardest on exactly the people who thought they had nothing to worry about. High-volume bettors who break even. Standard-deduction taxpayers who never itemize. Professional players whose expenses just got swept into the cap. And event contract traders who never decided whether their trading is gambling at all.

We prepare returns for traders and bettors across every platform, and this guide runs the actual numbers: what changed, who pays, how the itemizing trap works, what a session is and why it suddenly matters more, and how the cap interacts with prediction markets and crypto.

Let's get into it.

What Changed: Section 165(d) Before and After

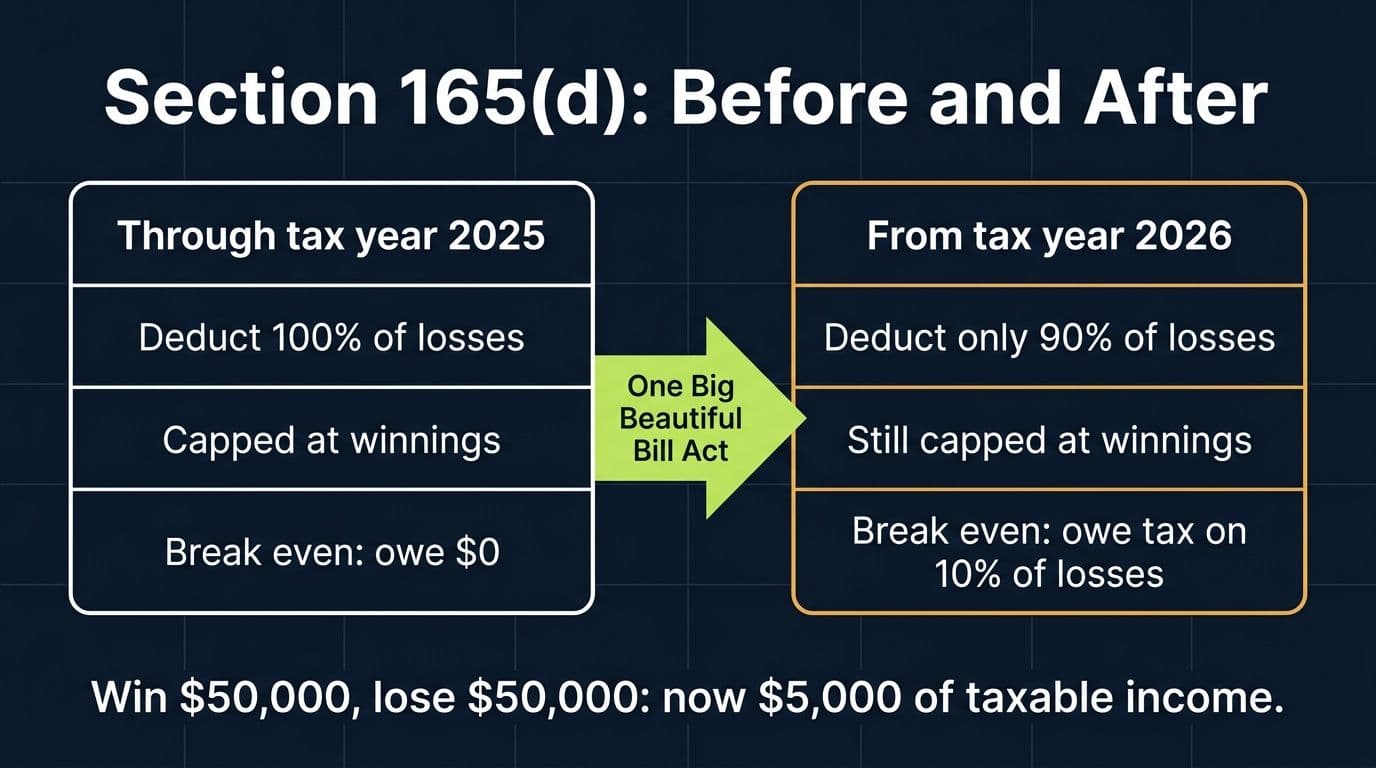

Section 165(d) is the wagering loss rule. Through the 2025 tax year it says losses from wagering transactions are deductible only to the extent of gains from wagering transactions. Win $30,000, lose $30,000, deduct $30,000, owe nothing. The rule was harsh in one direction only: net losses never deduct, but breaking even was tax-neutral.

The One Big Beautiful Bill Act, signed July 4, 2025, changed the formula. For tax years beginning after December 31, 2025, the deduction equals 90% of your losses, and it remains allowed only to the extent of your winnings. Your deduction is now the smaller of two numbers: 90% of losses, or total winnings.

Three mechanical points people get wrong:

- It's 90% of losses, not 90% of winnings. Some early coverage garbled this. If you win $100,000 and lose $80,000, you deduct 90% of $80,000, which is $72,000, and your taxable gambling income is $28,000 instead of $20,000.

- The winnings cap still applies on top. Win $10,000 and lose $50,000, and 90% of losses is $45,000, but you still deduct only $10,000. Net losing years remain nondeductible, same as always.

- The effective date follows tax years, not bets. Losses in December 2025 fall under the old 100% rule on your 2025 return. The same bet placed in January 2026 falls under the cap. Your 2025 return, filed in 2026, is the last one under the old math.

Gambling Loss Deduction: Old Law vs 2026 (Itemizers)

| Scenario | Through Tax Year 2025 | From Tax Year 2026 |

|---|---|---|

| Win $50,000, lose $50,000 | Deduct $50,000, taxable income $0 | Deduct $45,000, taxable income $5,000 |

| Win $100,000, lose $80,000 | Deduct $80,000, taxable income $20,000 | Deduct $72,000, taxable income $28,000 |

| Win $10,000, lose $50,000 | Deduct $10,000, no loss carryover | Deduct $10,000, no loss carryover |

| Take the standard deduction | Deduct $0 | Deduct $0 |

The Phantom Income Problem

The cap's signature effect is tax on money you never made, and it scales with volume, not with profit.

Take a high-volume 2026 bettor who wins $200,000 and loses $200,000 across the year. Economically: exactly zero. Under amended Section 165(d): $200,000 of winnings minus a $180,000 deduction leaves $20,000 of taxable income. At a 24% rate that's $4,800 of federal tax on a year that made nothing. At 37%, it's $7,400.

Notice what drives the number: gross volume. A casual player with $3,000 of wins and $3,000 of losses has $300 of phantom income, an annoyance. A daily bettor or active event contract trader churning six figures of gross winnings has phantom income in the tens of thousands, even in a losing year, because the deduction shrinks while the winnings stay fully countable. The people hurt most are high-frequency players with thin margins, which describes most serious sports bettors and a lot of prediction market traders.

$20,000 taxable on $0 profit

A 2026 bettor with $200,000 of winnings and $200,000 of losses breaks even in reality and still reports $20,000 of income under the 90% cap.

That's the itemizer's version of the problem. The standard-deduction version is worse, and it affects far more people.

The Itemizing Trap Nobody Mentions

Everything above assumed you itemize. Most taxpayers don't, and the 90% cap changed nothing about that part of the rule: gambling losses deduct only on Schedule A. Per IRS Topic 419, you report full winnings as income either way; itemizing is the only path to any loss deduction at all.

For 2026, the standard deduction is $16,100 single and $32,200 married filing jointly. Roughly nine in ten filers take it. For them the loss deduction, capped or not, is theoretical.

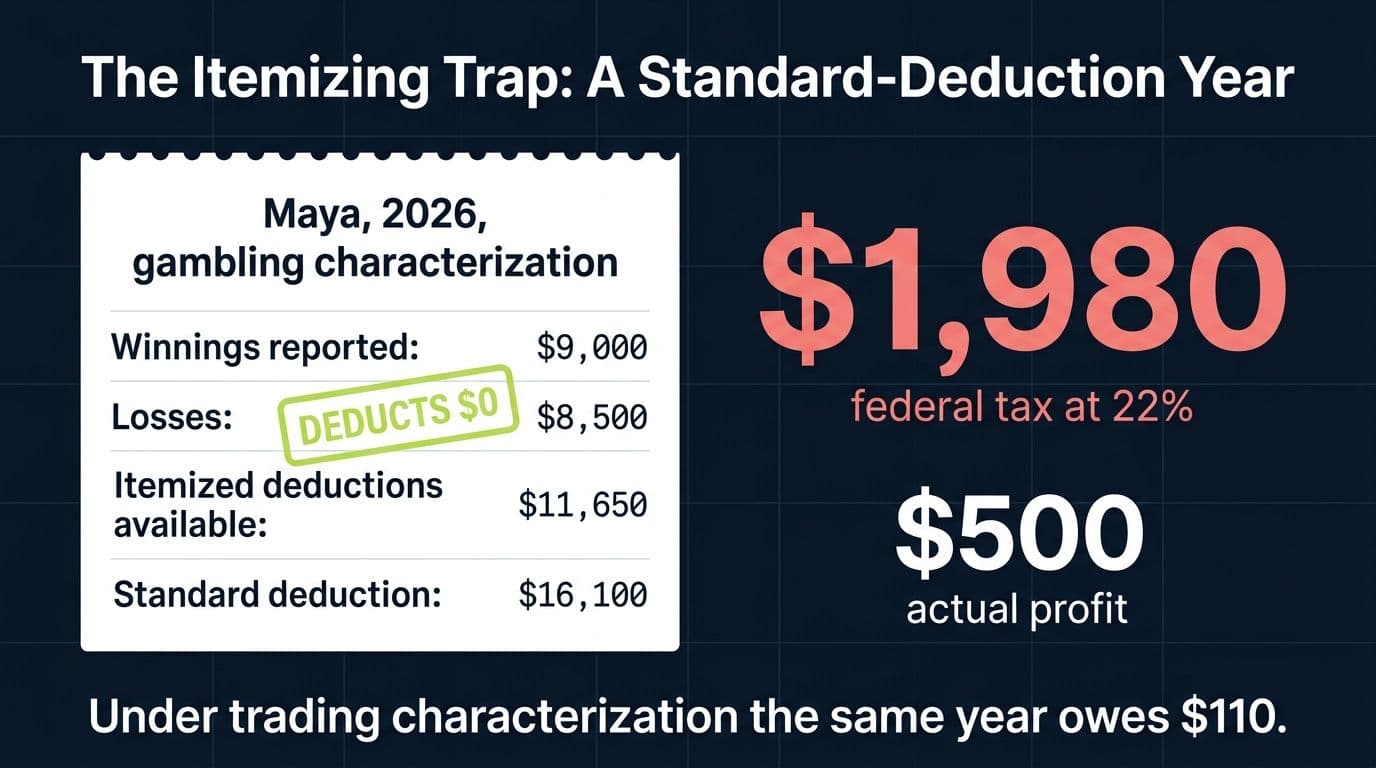

Meet Maya: single, $85,000 salary, 22% bracket, renter, takes the standard deduction every year. In 2026 she gets into sports betting and Kalshi sports contracts, and by December she's won $9,000 and lost $8,500. Real profit: $500.

If her activity is characterized as gambling, her return looks like this. Winnings: $9,000 of income, all of it. Losses: her potential itemized deductions are 90% of $8,500 ($7,650) plus about $4,000 of state taxes, totaling $11,650, which is less than her $16,100 standard deduction. So she takes the standard deduction, exactly as before, and deducts zero gambling losses. Her tax on the activity: $9,000 at 22%, or $1,980, on $500 of actual profit. That's an effective rate just shy of 400%.

The trap has always existed; the 2026 rules just raised the volume at which it bites, because gross winnings are growing across sportsbooks and event platforms while the standard deduction keeps climbing. And it has a mirror image worth seeing clearly: if Maya's Kalshi activity were properly characterized as trading financial contracts rather than wagering, she'd report the $500 net and owe $110. Same year, same trades, eighteen times less tax. Hold that thought for two sections.

“The 90% cap gets the headlines, but the returns I worry about are the standard-deduction filers. They hear losses are deductible, net their own numbers, and report the difference. That has never been how the rule works, and in 2026 the gap between what they report and what the forms show is bigger than ever.”

, Leanne Grant, EA

A Worked Example: An Itemizer's Full 2026 Year

Now the itemizer case, where the cap itself does the damage. Meet Victor: married filing jointly, 24% bracket, with $41,000 of mortgage interest and state taxes, so he itemizes regardless. He bets sports and trades event contracts at volume. His 2026: $120,000 of winnings, $110,000 of losses, net profit $10,000.

Victor's 2026 Year: Old Law vs the 90% Cap (24% Bracket, Itemizer, Gambling Characterization)

| Line | Old Law (Through 2025) | New Law (2026) |

|---|---|---|

| Winnings reported as income | $120,000 | $120,000 |

| Loss deduction | $110,000 | $99,000 (90% of $110,000) |

| Taxable gambling income | $10,000 | $21,000 |

| Federal tax at 24% | $2,400 | $5,040 |

The cap costs Victor $2,640 a year at his volume, a 110% tax increase on the same real profit. Run his year at break-even ($110,000 both directions) and he'd still owe tax on $11,000 he never made. There's also a quieter cost: the extra $11,000 of reported income raises his adjusted gross income, which can shave credits and deductions that phase out with AGI, a second-order hit the headline math hides.

One planning note that follows directly from the effective date: the cap applies to tax years beginning after December 31, 2025, and there is no averaging between years. A bettor who was going to realize heavy gross activity had every reason to do it in 2025; from here forward, the only levers left are session accounting, characterization, and volume itself.

Want Your 2026 Numbers Run Before the IRS Runs Them?

We model gambling and event contract years under every characterization before filing season, so the 90% cap never surprises you in April. Flat fee, handled by a CPA who does this all year.

Book a callWhat Counts as a Session (and Why It Matters More Now)

Here's the technical concept that quietly controls how hard the cap hits: the session.

You don't compute gambling winnings bet by bet. Under the IRS's long-standing approach for casual gamblers, endorsed in Tax Court cases like Shollenberger and IRS legal memoranda for slot play, you net within a gambling session: money out versus money in for one continuous stretch of play at one venue. Walk into a casino with $500, play for three hours, walk out with $800, and you have one $300 session win, not four hundred individual wagers.

Session accounting shrinks both your gross winnings and your gross losses, and under the 90% cap that shrinkage is worth real money. Watch the same slot afternoon computed both ways. Rosa buys in for $100, hits a $2,000 jackpot mid-session (which triggers a W-2G at the new threshold), keeps playing, and cashes out $400 at the end.

- Bet-by-bet framing: $2,000 of winnings, $1,700 of losses. 2026 deduction: 90% of $1,700, or $1,530. Taxable: $470.

- Session framing: one session, in $100, out $400. Taxable: $300, and no loss deduction is needed at all, so the 90% cap never engages and itemizing doesn't matter.

Same afternoon, 36% less taxable income, and the session version survives the standard deduction intact. Multiply that across a year of volume and session discipline becomes the single most valuable recordkeeping habit a 2026 gambler has.

The catch: nobody knows exactly what a session is outside casino floors. The IRS has never defined sessions for online sportsbooks, daily fantasy, or continuous digital markets. Is a day of trading a session? One market? One login? For event contract traders under gambling characterization this is a genuinely unanswered question, one more instability in a characterization that keeps getting more expensive. Whatever position you take, take it consistently and keep contemporaneous logs: dates, platforms, buy-ins, cash-outs, screenshots. The IRS asks for exactly that kind of diary when it examines gambling returns.

Professional Gamblers: The Cap Reaches Schedule C Too

If gambling is your actual trade or business, you file Schedule C, and for years you had one structural advantage: business treatment. The OBBBA took direct aim at it.

Two changes stack. First, the TCJA rule treating business expenses as wagering losses for professionals, which was set to expire after 2025, is now permanent. Travel to tournaments, data subscriptions, entry fees, coaching: all of it counts inside the Section 165(d) limitation, not as freestanding business deductions. Second, the 90% cap applies to that combined pile.

Meet Dre, a professional player: $300,000 of gross winnings, $240,000 of wagering losses, $30,000 of legitimate business expenses. Real economics: $30,000 of profit. His 2026 Schedule C: winnings of $300,000, minus a deduction capped at 90% of the combined $270,000 of losses and expenses, which is $243,000. Taxable: $57,000, nearly double his true profit, and it's self-employment income on top of income tax. Under 2025 law he'd have reported $30,000. The cap manufactures $27,000 of income for Dre out of expenses he genuinely paid.

Professionals still cannot report an overall wagering loss, same as before. What changed is that even solidly profitable professionals now pay tax on a phantom slice, and the phase-out math some pros used to manage (retirement contributions, QBI, ACA subsidies) gets distorted by the inflated AGI. If you file as a pro, 2026 estimated payments need to be rebuilt around the new base.

Event Contract Traders: Does the 90% Cap Even Apply to You?

Now the question this site's readers actually care about. If you trade Kalshi, Robinhood event contracts, or Polymarket US, is your activity even inside Section 165(d)?

Honest answer: the IRS has never said. There is no guidance characterizing event contracts as wagering or as anything else. Practitioners file these under four different frameworks (ordinary income, capital asset, Section 1256, and gambling), and we walk the full decision in our prediction market taxes guide. Most practitioners, us included, do not reach for gambling treatment on regulated exchanges where you trade transferable contracts at market prices against other traders rather than betting against a house. But the argument is live, and it is strongest exactly where the volume is: sports contracts.

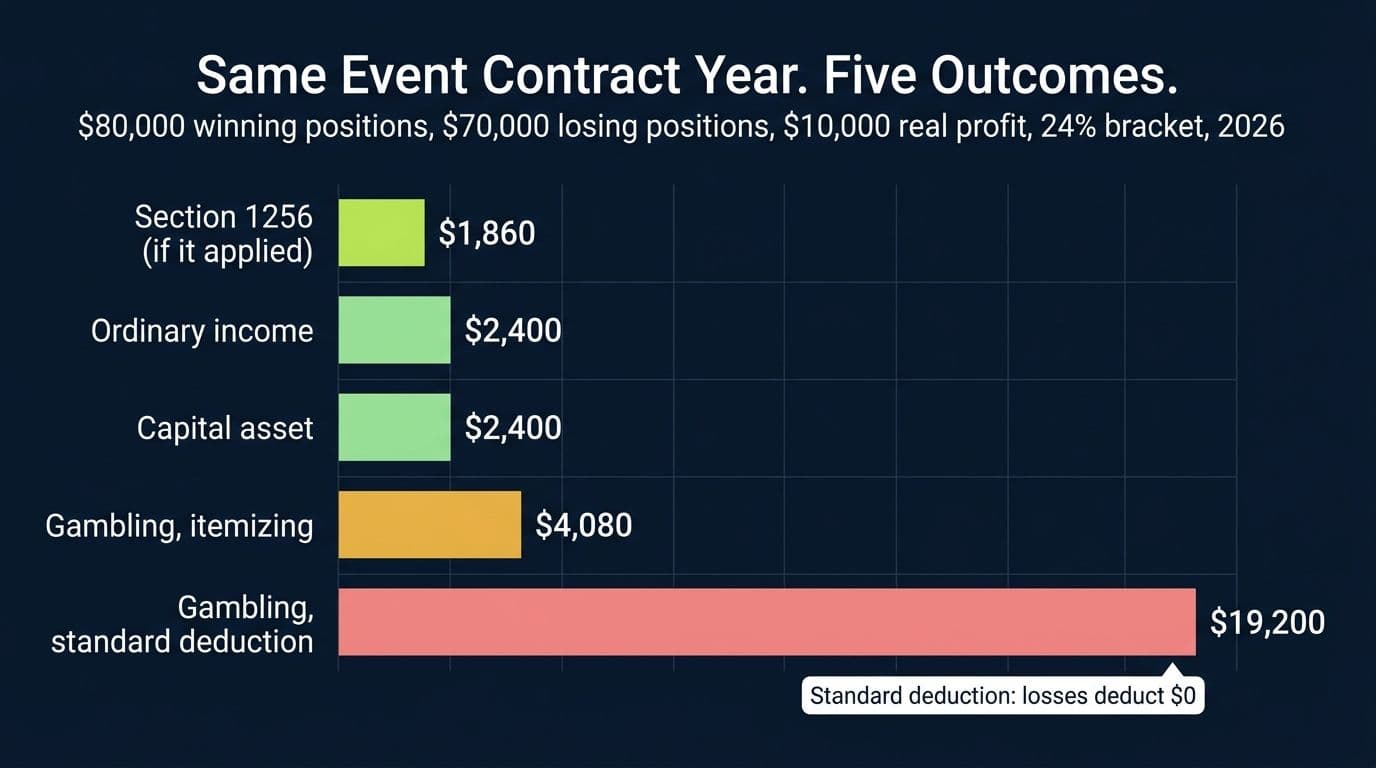

What the 90% cap did is turn that abstract debate into a priced one. Here's the same 2026 event contract year, $80,000 of winning positions and $70,000 of losing ones (net profit $10,000, 24% bracket), under each characterization:

The Same Event Contract Year Under Each Characterization (2026, 24% Bracket)

| Characterization | How Losses Work | Taxable Amount | Federal Tax |

|---|---|---|---|

| Ordinary income | Net within the activity | $10,000 | $2,400 |

| Capital asset | Net against capital gains in full | $10,000 | $2,400 |

| Section 1256 (if it applied) | Net in full, 60/40 rates | $10,000 | $1,860 |

| Gambling, itemizing | 90% of losses, Schedule A | $17,000 | $4,080 |

| Gambling, standard deduction | No deduction at all | $80,000 | $19,200 |

Read the bottom row twice. A standard-deduction trader whose event contracts get swept into gambling characterization pays tax on gross winning positions with nothing against them. That outcome was always technically possible; the 2026 rules just made every step of it more expensive. The financial-instrument characterizations (ordinary, capital, and the unproven Section 1256 position) avoid Section 165(d) entirely: losses net in full, no itemizing requirement, no 90% haircut, no session ambiguity.

Practical takeaways if you trade event contracts:

- Decide your characterization deliberately, with the loss rules in view, and document it. The cap made gambling treatment the most expensive answer by a wider margin than ever.

- Split sports from macro in your records. Sports contracts carry the most wagering-characterization risk. If a future IRS position splits the categories, contemporaneous records are the difference between a clean amended computation and a mess.

- Stay consistent across platforms. Claiming capital treatment on your winning platform and gambling treatment on your losing one is not a strategy, it's an audit finding. Our Kalshi taxes guide covers the per-platform paperwork.

Crypto Losses Are Not Gambling Losses

One boundary worth drawing precisely, because crypto traders keep asking: the 90% cap does not touch crypto trading losses.

Crypto is property. Losses from selling or swapping crypto are capital losses: they offset capital gains in full, then up to $3,000 of ordinary income per year, with indefinite carryforward. None of that runs through Section 165(d), so the 90% cap is irrelevant to a bad trading year. Do not let anyone talk you into reporting crypto trading losses as gambling losses because the activity felt like a casino; the law is settled here in a way it is not for event contracts.

Where crypto and the gambling rules genuinely intersect:

- Crypto casinos and offshore books. If you wager crypto, the gambling rules apply to the wagering layer (winnings as income, losses under the capped Schedule A regime), and there's a second, separate layer: staking your BTC is a disposal of property, with capital gain or loss measured against your basis. Two regimes, one bet, and the recordkeeping burden of both.

- Funding event platforms with crypto. Depositing BTC or USDC into a platform that converts it to dollars is a taxable disposal before you ever trade, an entirely capital-side event.

- Netting confusion. Gambling losses never offset capital gains, and capital losses never offset gambling winnings. In a year where you have both, the two buckets are computed separately and the worst version of each rule applies to its own bucket.

The Reporting Side Also Changed

Two threshold changes arrive alongside the cap, both from the same bill, and both cut the other direction: fewer forms, not more.

The slot machine Form W-2G threshold rises from the ancient $1,200 to $2,000 for payments after December 31, 2025, with inflation indexing after 2026. And the general 1099-MISC information reporting threshold rises from $600 to $2,000 for 2026 payments, which is why fewer prediction market bonus and promo forms will arrive. Treasury has already issued proposed regulations aligning the reporting rules with the statute.

Do not misread the direction of this. Fewer forms means less withholding-style visibility, not less tax. Winnings are taxable from the first dollar, form or no form, and the platforms keep complete records of everything regardless of what they mail you. The combination the 2026 rules actually create is nasty: your gross winnings remain fully reportable while your deduction shrinks, and the paper trail that would have reminded you gets thinner. The taxpayers who reconstruct their year from their own records will file correctly. The ones who wait for forms will understate, and understatement on a KYC'd account is the easiest thing in the world for the IRS to find later.

Will Congress Fix It?

Maybe eventually. Not yet, and you should not file as if it will.

The 90% cap drew bipartisan fire almost immediately. The FAIR BET Act, introduced by Rep. Dina Titus, would restore the full 100% deduction, and the gaming industry has pushed hard for it. But House leadership blocked it from reaching a floor vote, and as of mid 2026 no repeal has passed. Nevada lawmakers and industry groups keep trying, and some version of relief could still move. Until something is signed, the 90% cap is the law for tax year 2026, and estimated payments, withholding decisions, and characterization analysis should all assume it stays.

If a retroactive fix does pass, amended returns can recover the difference. That's a nice option to have. It is not a filing strategy.

What to Do Now: The 2026 Playbook

Seven moves, in order of value:

- Keep session-level records starting today. Dates, platforms, buy-ins, cash-outs, contemporaneous logs. Session accounting is the last legal lever that shrinks both sides of the ledger, and it only works with records.

- Decide your characterization on event contracts deliberately. The gap between gambling and financial-instrument treatment is now the largest single number in prediction market taxes. Get the analysis documented before filing season, not during.

- Check whether you'll actually itemize. If your losses only matter on Schedule A and you're nowhere near $16,100 single or $32,200 joint, plan around the reality that your deduction is zero.

- Rebuild estimated payments on the new base. Phantom income is still income for underpayment purposes. High-volume 2026 players should be paying quarterlies against the capped math now.

- Separate your buckets. Gambling, event contracts, and crypto each carry their own loss regime. Never net across buckets, and never let a platform's aggregate statement do your characterization for you.

- Professionals: rerun everything. With expenses inside the cap, Schedule C pros need new projections for SE tax, retirement contributions, and any AGI-sensitive planning.

- If prior years are wrong, fix them proactively. The 2026 rules bring more IRS attention to the whole category. Amended returns filed before a notice are treated very differently from corrections after one.

Pro Tip

The single cheapest tax move a 2026 bettor can make is a contemporaneous session log. It costs nothing, the IRS's own examination guidance asks for it, and under the 90% cap it routinely saves more than any deduction strategy you can buy in April.

The pattern across every example in this guide: the 2026 rules punish people who let the forms, the platforms, or the defaults decide their tax treatment. The math is knowable in advance, the characterization is a decision with documentation, and every dollar of difference between the best and worst outcome is determined before you file. That's either a warning or an opportunity, depending on when you start.

Get Ahead of the 90% Cap

Flat-fee tax preparation for bettors and event contract traders: sessions reconstructed, characterization documented, estimates rebuilt for the new rules, return signed by a CPA who has done this before.

Book a callFAQ: The 2026 Gambling Loss Deduction Rules

Frequently Asked Questions

Can you still deduct gambling losses in 2026?

Yes, but only 90% of them, only up to your winnings, and only if you itemize. The One Big Beautiful Bill Act amended Section 165(d) for tax years beginning after December 31, 2025, so a break-even year now leaves 10% of your losses stranded as taxable income.

What is the new 90% rule for gambling losses?

Your deduction equals the smaller of 90% of your total gambling losses or your total winnings. Win $100,000 and lose $80,000 in 2026 and you deduct $72,000, paying tax on $28,000 instead of the $20,000 you actually netted.

When does the 90% gambling loss cap take effect?

For tax years beginning after December 31, 2025, which for individuals means calendar year 2026, first reported on returns filed in early 2027. Your 2025 return, filed in 2026, still uses the old 100% rule.

Do you have to itemize to deduct gambling losses?

Yes. Gambling losses deduct only on Schedule A, and that did not change. Winnings are reported as income in full either way. If you take the standard deduction ($16,100 single, $32,200 married filing jointly for 2026), you deduct zero losses.

Can you deduct gambling losses if you take the standard deduction?

No. Losses are an itemized deduction only. A standard-deduction taxpayer with $9,000 of winnings and $8,500 of losses pays tax on the full $9,000 under gambling characterization, which is why characterization matters so much for event contract traders.

What is the W-2G threshold for 2026?

The slot machine threshold rose from $1,200 to $2,000 for payments after December 31, 2025, with inflation indexing after 2026. Fewer forms will arrive, but all winnings remain taxable from the first dollar whether or not a W-2G is issued.

Does the 90% cap apply to professional gamblers?

Yes, and harder. For Schedule C professionals, business expenses now permanently count as wagering losses, and the 90% cap applies to the combined total of losses plus expenses. A profitable professional can owe tax on income well above their true economics.

Do Kalshi or prediction market losses count as gambling losses?

Only if the activity is characterized as gambling, and the IRS has never ruled on that. Most practitioners treat regulated event contracts under ordinary income or capital asset principles, where losses net in full and the 90% cap never applies. The characterization decision is now worth more than ever, and it should be documented.

Are crypto losses subject to the 90% gambling cap?

No. Crypto trading losses are capital losses: they offset capital gains in full plus up to $3,000 of ordinary income per year with carryforward, entirely outside Section 165(d). The cap only reaches crypto when you actually wager it, such as at a crypto casino, and even then only the wagering layer.

How does the IRS know about my gambling winnings?

W-2Gs, 1099s, and payment records all flow to IRS matching systems, and every regulated platform keeps complete KYC'd records the IRS can request. Thresholds rose for 2026, so fewer forms arrive, but the underlying records and your reporting obligation are unchanged.

What records does the IRS require for gambling losses?

A contemporaneous log: dates, venues or platforms, amounts in and out per session, plus supporting documents like statements, tickets, and screenshots. Under the 90% cap, session-level records also directly reduce your taxable phantom income, so they're worth keeping even if you're never examined.

Will the 90% gambling loss cap be repealed?

Unknown. The FAIR BET Act would restore the 100% deduction and has bipartisan support, but it was blocked from a House floor vote and had not passed as of mid 2026. File and plan under the 90% cap; if a retroactive fix passes, an amended return can recover the difference.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Prediction Market Taxes (2026): How Kalshi, Polymarket, Robinhood and Every Major Platform Gets Taxed

How prediction market taxes work on Kalshi, Polymarket, Robinhood and more. A CPA splits platforms by settlement type and shows exactly what to report.

Section 1256 and Event Contracts (2026): Do Kalshi and Prediction Markets Get 60/40 Treatment?

Section 1256's 60/40 rate could cut a prediction market trader's federal bill by a quarter, but no platform reports event contracts that way. A CPA walks the statutory test, the math, and the Form 6781 and Form 8275 mechanics.

Kalshi Taxes (2026): A CPA's Guide to the Forms You'll Get, the One You Won't, and What You Owe

Kalshi sends 1099s for interest, rewards, and crypto conversions, but nothing for your trading profit. A CPA walks through every form, four tax treatments, and one full worked year.