Section 1256 and Event Contracts (2026): Do Kalshi and Prediction Markets Get 60/40 Treatment?

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Section 1256 contracts get marked to market at year end and taxed on a 60/40 split: 60% long-term and 40% short-term regardless of holding period, which caps the top blended federal rate near 28% instead of 37%.

- ✓Event contracts arguably qualify because they trade on CFTC-designated contract markets, but they must also fit one of Section 1256's enumerated contract types, and that question has no IRS ruling, no case law, and credible arguments on both sides.

- ✓The Dodd-Frank swap exclusion in Section 1256(b)(2)(B) is the strongest argument against 60/40 treatment, because the CFTC has described event contracts as binary options that are swaps in other contexts.

- ✓No prediction market platform reports event contracts in the Section 1256 section of any 1099. Robinhood explicitly leaves them out of its 1099-B, and Kalshi issues no trading 1099 at all.

- ✓Section 1256 is a package, not a rate: year-end mark to market taxes open positions on unrealized gains, and a documented position with a Form 8275 disclosure is the only defensible way to claim it.

Quick answer: Maybe, and nobody can honestly promise you more than that. Section 1256 gives qualifying contracts a blended 60% long-term, 40% short-term capital gains rate, which usually beats ordinary income treatment by a wide margin. Kalshi, ForecastEx, Rothera, and Polymarket US all operate CFTC-designated contract markets, which satisfies one prong of the statute. But whether a binary event contract fits any of Section 1256's enumerated contract types is genuinely unresolved: the CFTC has described event contracts as binary options that are swaps in other contexts, and the Dodd-Frank swap exclusion may knock them out entirely. No platform reports event contracts as Section 1256 contracts on any 1099. If you claim 60/40 treatment, do it as a documented position with a written analysis and consider a Form 8275 disclosure. This guide walks the full statutory test, the math on both sides, and the mechanics of Form 6781 if you take the position.

Every tax season we get some version of the same email: "I saw that futures traders pay a special 60/40 rate. I traded event contracts on a CFTC-regulated exchange. Do I get the rate?"

It's the right question. The answer is worth real money, the internet is full of confident claims in both directions, and the IRS has said exactly nothing.

Here's the deal: Section 1256 event contracts treatment is an unproven legal position, not a checkbox. The exchanges are regulated enough to keep the argument alive, the statute is ambiguous enough that nobody has won it, and the paperwork you receive actively points the other way. We prepare returns for prediction market traders every season, and we have filed documented Section 1256 positions. We have also talked plenty of traders out of them.

This guide walks through what Section 1256 actually says, the two-part test a contract has to pass, the honest case for and against event contracts, one trader's year priced under every treatment, and the Form 6781 and Form 8275 mechanics if you decide the position fits your facts.

Let's get into it.

What Is a Section 1256 Contract? The 60/40 Deal Explained

Section 1256 is a special tax regime Congress built in 1981 for exchange-traded derivatives. It does two unusual things.

First, mark to market: every Section 1256 contract you hold on December 31 is treated as sold at fair market value on that day. You pay tax on unrealized gains and deduct unrealized losses, then adjust your basis so nothing gets double counted when the position actually closes.

Second, the 60/40 split: all gains and losses from Section 1256 contracts are treated as 60% long-term capital gain or loss and 40% short-term, no matter how long you held the position. Hold a futures contract for eleven minutes and 60% of the gain still gets long-term rates.

That second rule is the prize. Short-term gains are taxed at ordinary rates, up to 37%. Long-term gains top out at 20%. Blend them 60/40 and the maximum federal rate on 1256 gains lands around 28%, and for most traders it lands much lower. There's a bonus too: net Section 1256 losses can be carried back three years against prior 1256 gains, the only loss carryback ordinary investors ever see.

The regime exists because traditional futures are already marked to market daily by clearinghouses, with cash moving in and out of margin accounts every night. Congress decided to tax the economics the way the market already measured them, and threw in the 60/40 blend to keep effective rates reasonable on instruments that turn over constantly.

The whole fight over prediction markets is whether a binary event contract belongs to that regime. Everything below is that fight.

~28% vs 37%

The top blended federal rate on Section 1256 gains versus the top ordinary rate. On a $100,000 profit year, the difference approaches $9,000 before state tax.

The Statutory Test: How a Contract Actually Qualifies

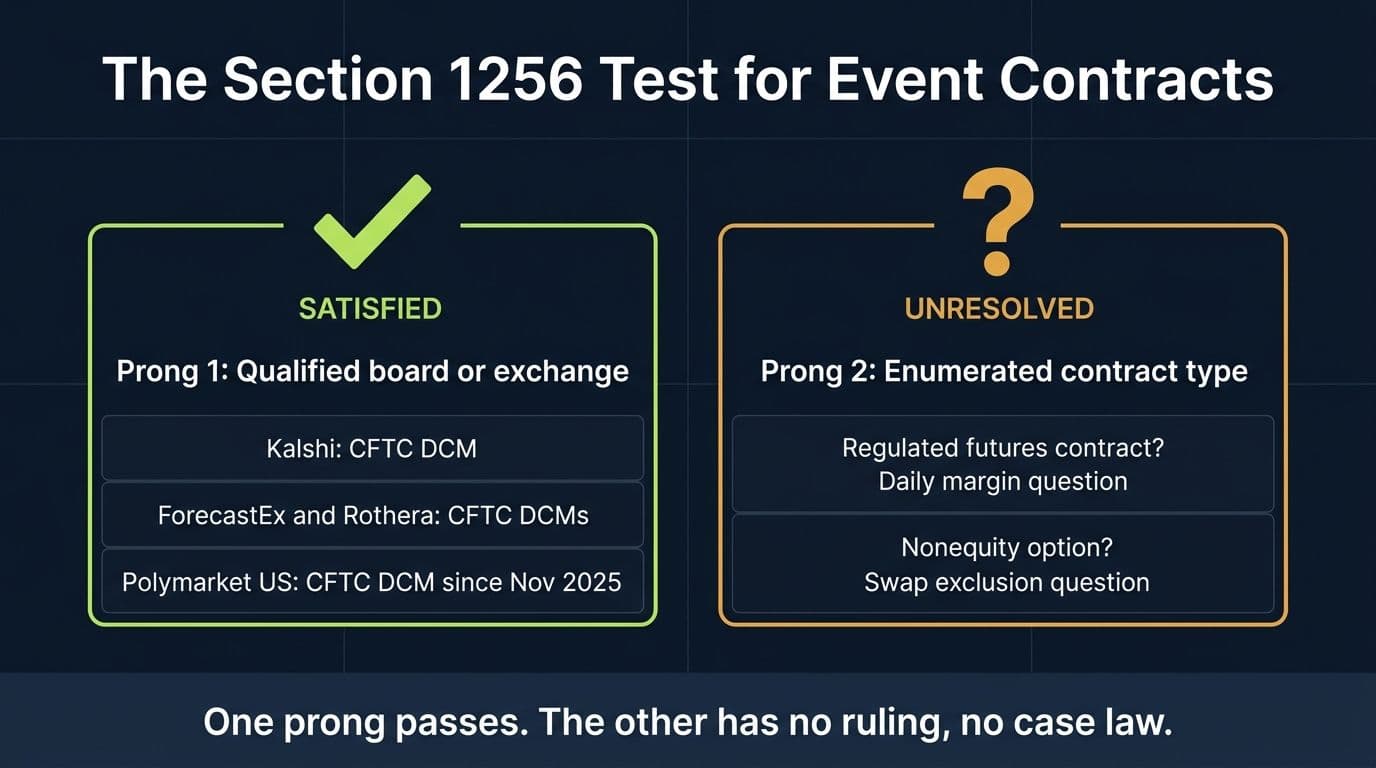

Section 1256 does not cover "things traded on regulated exchanges." It covers a specific list. Under Section 1256(b)(1), a Section 1256 contract means one of five things:

- A regulated futures contract

- A foreign currency contract

- A nonequity option

- A dealer equity option

- A dealer securities futures contract

Event contracts are not foreign currency contracts and retail traders are not dealers, so the argument runs through two doors: regulated futures contract or nonequity option. Each door has its own definition, and both definitions share one requirement.

The Shared Requirement: A Qualified Board or Exchange

Both doors require the contract to trade on, or be subject to the rules of, a qualified board or exchange. Section 1256(g)(7) defines that as a national securities exchange registered with the SEC, a domestic board of trade designated as a contract market by the CFTC, or any other exchange the Treasury designates.

This is the prong the prediction market industry actually satisfies, and it's worth being precise about why. KalshiEX LLC is a CFTC-designated contract market. So are ForecastEx LLC and Rothera Exchange and Clearing LLC, the venues behind Robinhood's event contracts. Since November 2025, Polymarket US runs on a designated contract market as well. You can verify any of them on the CFTC's designated contract markets list.

So when someone says "Kalshi is a regulated exchange, therefore 60/40," they are quoting the half of the test that passes. A designated contract market is exactly what the statute means by a qualified board or exchange. If the analysis stopped there, this article would be two paragraphs long.

It doesn't stop there.

Door One: Regulated Futures Contract

Section 1256(g)(1) defines a regulated futures contract as a contract that trades on a qualified board or exchange and "with respect to which the amount required to be deposited and the amount which may be withdrawn depends on a system of marking to market."

That second clause describes variation margin: the daily cash settlement system where a futures clearinghouse credits winners and debits losers every night based on the settlement price.

Here's the problem for event contracts: most are fully collateralized binary contracts. You pay the full price up front (say $0.45 per contract), your maximum loss is capped at what you paid, and no money moves in or out of your account until you sell or the contract settles. Whether that structure "depends on a system of marking to market" in the statutory sense is a genuinely open question. Exchanges do publish daily settlement prices, and clearinghouses do mark positions for risk purposes, but the daily cash flow mechanism the definition seems to describe mostly is not there.

Door one is not closed. It's just not the confident walk-through some commentary suggests.

Door Two: Nonequity Option

Section 1256(g)(3) defines a nonequity option as any listed option that is not an equity option, and Section 1256(g)(5) defines a listed option as any option traded on, or subject to the rules of, a qualified board or exchange.

This is the door most serious pro-1256 analysis uses. The argument: a binary event contract is economically an option (a fixed payout contingent on an outcome, purchased for a premium), the CFTC itself has repeatedly described event contracts as binary options, the contracts are listed on qualified exchanges, and an option on "will the Fed cut rates" is certainly not an equity option. Chain those together and you get a nonequity option, which is a Section 1256 contract.

It's a real argument. It's also the argument that walks directly into the statute's biggest trap.

The Case Against: Binary Options, Swaps, and Section 1256(b)(2)(B)

In 2010, Dodd-Frank added Section 1256(b)(2)(B), which excludes from Section 1256 treatment "any interest rate swap, currency swap, basis swap, interest rate cap, interest rate floor, commodity swap, equity swap, equity index swap, credit default swap, or similar agreement."

Two words carry the whole fight: similar agreement.

The CFTC has described event contracts as binary options, and in its Dodd-Frank rulemakings it treated binary options as falling within the statutory swap definition when they are not otherwise excluded. The Treasury regulations under Section 1256 punt on the details, and the legislative history says the exclusion was meant to sweep in contracts that function like swaps regardless of label. If a cash-settled binary contract on an occurrence or nonoccurrence is a "similar agreement," Section 1256 treatment is dead on arrival no matter which door you came through, because the swap exclusion overrides both.

The counterargument is respectable too: the enumerated swaps in 1256(b)(2)(B) are all bilateral, periodic-payment instruments, and a fully paid, exchange-listed binary contract that clears through a designated contract market looks more like a listed option than like a credit default swap. On this reading, the exclusion targets the over-the-counter swap book, not standardized contracts listed on a qualified exchange.

Nobody has litigated it. The IRS has issued no ruling, no notice, no regulation on event contracts specifically. KPMG's analysis of CFTC-regulated sports event contracts treats the classification as an open question with materially different outcomes on each side, and that remains the honest state of the law in 2026. On the optimistic end, a widely cited Forbes piece argued prediction markets are the tax-advantaged way to gamble on sports precisely because of the 60/40 theory. Both can't be right, and no authority has picked.

One more layer of mess: if event contracts are not Section 1256 contracts and are not capital assets either, some contracts could even land in gambling treatment, which after the One Big Beautiful Bill Act caps loss deductions at 90% of losses for 2026. The characterization ladder has more than two rungs, and we priced all of them in our prediction market taxes guide.

What the Platforms Themselves Are Telling You

Statutes are one signal. The paper trail is another, and it points one direction.

No prediction market platform reports event contracts as Section 1256 contracts. Real futures brokers report regulated futures in the Section 1256 section of a 1099-B, with the aggregate profit and loss and year-end marks computed for you. That's what the reporting regime looks like when a broker believes the instrument qualifies.

Now compare. Kalshi issues no 1099 covering your event contract trading at all; you get a profit and loss statement the platform itself labels as not tax advice (our Kalshi taxes guide covers the full form list). Robinhood issues an Event Contracts Annual Statement and explicitly keeps event contracts out of the Section 1256 section of its 1099-B, even though it reports actual regulated futures there for the same customers. Polymarket US issues nothing for the trades either.

That tells you what the platforms' counsel concluded: not proven. It doesn't mean the position is wrong. Broker reporting categories are conservative by design, and brokers have been slow before. But it means that if you file Form 6781 with event contract gains on it, you are asserting a characterization that no form the IRS received supports. The IRS computer sees a 6781 with numbers no broker reported. That's not fatal. It is exactly why documentation and disclosure matter, and we'll get to both.

“When a client asks me for the 60/40 rate, my first question is whether they can show me the analysis, not the spreadsheet. A Section 1256 position on event contracts filed without a memo is not a tax position. It's a hope with a form number.”

, Leanne Grant, EA

Platform by Platform: Where the Argument Is Strongest

The Section 1256 analysis is not one question; it's one question per venue, because the qualified exchange prong depends entirely on where the contract is listed.

The Section 1256 Argument by Platform (2026)

| Platform | Qualified Exchange Prong | Contract-Type Prong | Overall Posture |

|---|---|---|---|

| Kalshi | Yes, CFTC-designated contract market | Unresolved | Strongest argument, still unproven |

| Robinhood event contracts | Yes, routes to Kalshi, ForecastEx, Rothera (all DCMs) | Unresolved, and Robinhood excludes them from 1256 reporting | Same argument, weaker paper trail |

| Polymarket US (post Nov 2025) | Yes, designated contract market | Unresolved | Plausible for US DCM trades only |

| Polymarket offshore (pre 2026 activity) | No | Moot | No credible 1256 argument |

| Offshore crypto platforms (perps, offshore books) | No | Moot | No credible 1256 argument |

Notice what the table implies for traders with history: the same person can have Kalshi trades with a live 1256 argument and offshore trades with none. Characterization runs contract by contract and venue by venue. A single "I use 60/40 for my prediction markets" policy that sweeps in offshore activity is indefensible on its face, and it's the first thing an examiner would notice.

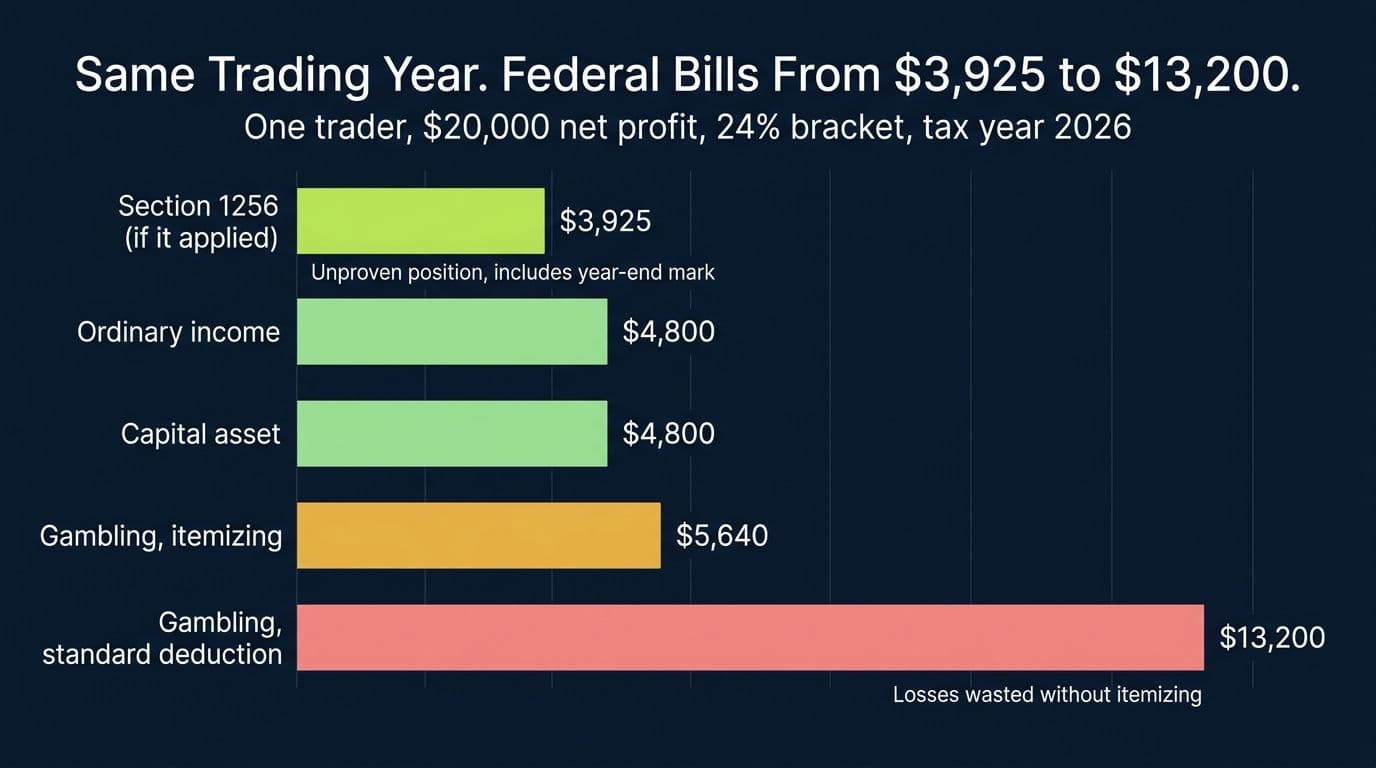

The Worked Example: Priya's Year Under Every Treatment

Numbers make the stakes concrete. Meet Priya: 24% federal bracket, files single, and an active Kalshi trader. During 2026 she closes positions with total proceeds of $68,000 against $48,000 of cost and fees, for a realized net profit of $20,000. On December 31 she also holds one open position: 5,000 contracts of a March Fed-cut market bought at $0.40 ($2,000 total), trading at $0.62 at year end, an unrealized gain of $1,100.

Here's her identical year under each candidate treatment. The Section 1256 row assumes the position survives scrutiny, uses the 60/40 split, and applies a 15% long-term capital gains rate; it also includes the year-end mark on her open position, because mark to market is part of the package.

Priya's 2026 Year: Federal Tax Under Each Treatment (24% Bracket)

| Treatment | What's Taxed | Federal Tax |

|---|---|---|

| Section 1256 (if it applied) | $21,100 ($20,000 realized + $1,100 year-end mark), split 60/40 | $3,925 |

| Ordinary income | $20,000 net profit on Schedule 1 | $4,800 |

| Capital asset (short-term) | $20,000 net gain on Form 8949 | $4,800 |

| Gambling, itemizing | $55,000 winnings less $31,500 (90% of $35,000 losses) | $5,640 |

| Gambling, standard deduction | Full $55,000 winnings, losses wasted | $13,200 |

The 1256 math: 60% of $21,100 is $12,660 taxed at 15% ($1,899), and 40% is $8,440 taxed at 24% ($2,026). Total $3,925, an effective rate of 18.6% even after paying tax on $1,100 she hasn't collected yet. Against ordinary treatment she saves about $875 this year, and the spread widens fast in higher brackets: at the top rates (37% ordinary, 20% long-term) the 60/40 blend saves roughly $10 per $100 of profit.

Two honest footnotes. The gambling rows treat each position as its own wager because the IRS has never defined a session for exchange-traded contracts, and they assume Priya's gross winning positions were $55,000 against $35,000 of losing ones. And the 1256 row taxes her open position's unrealized gain this year; her basis adjusts so 2027 doesn't tax it twice.

Want This Table Run on Your Actual Trading Year?

Garrett has filed prediction market returns under every treatment on this table, with the analysis documented. Bring your trade history and get a number, not a guess.

Book a callMark to Market: The Part of the Package Nobody Wants

Traders find Section 1256 because of the 60/40 rate. They forget it comes bolted to mark-to-market accounting, and the two are not separable.

If your event contracts are Section 1256 contracts, then every open position on December 31 is deemed sold at fair market value. Priya's $1,100 unrealized gain gets taxed in 2026 even though the market doesn't resolve until March 2027. If the position had been down $1,100 instead, she'd deduct the loss now, at 60/40 character.

For most event contract traders this is a modest effect, because positions resolve in days or weeks and year-end open interest is small. But it cuts hardest exactly when people want the treatment most: a trader sitting on large unrealized December gains in a longer-dated market (an election market that settles in November of next year, say) would owe tax on paper profits that could evaporate by spring. You cannot claim 60/40 on your closed trades and skip the year-end mark on your open ones. It's one regime, applied to everything that qualifies, every year, consistently.

That consistency requirement deserves its own sentence: Section 1256 is not an election you toggle when it helps. If the contracts qualify, they qualify in loss years too, and if you claimed the treatment last year, reverting this year because mark to market got expensive is the kind of pattern that turns a gray-area position into an examination issue.

How to Report: Form 6781 Mechanics

Suppose you and your advisor conclude the position is supportable and you take it. Here's how the reporting actually works.

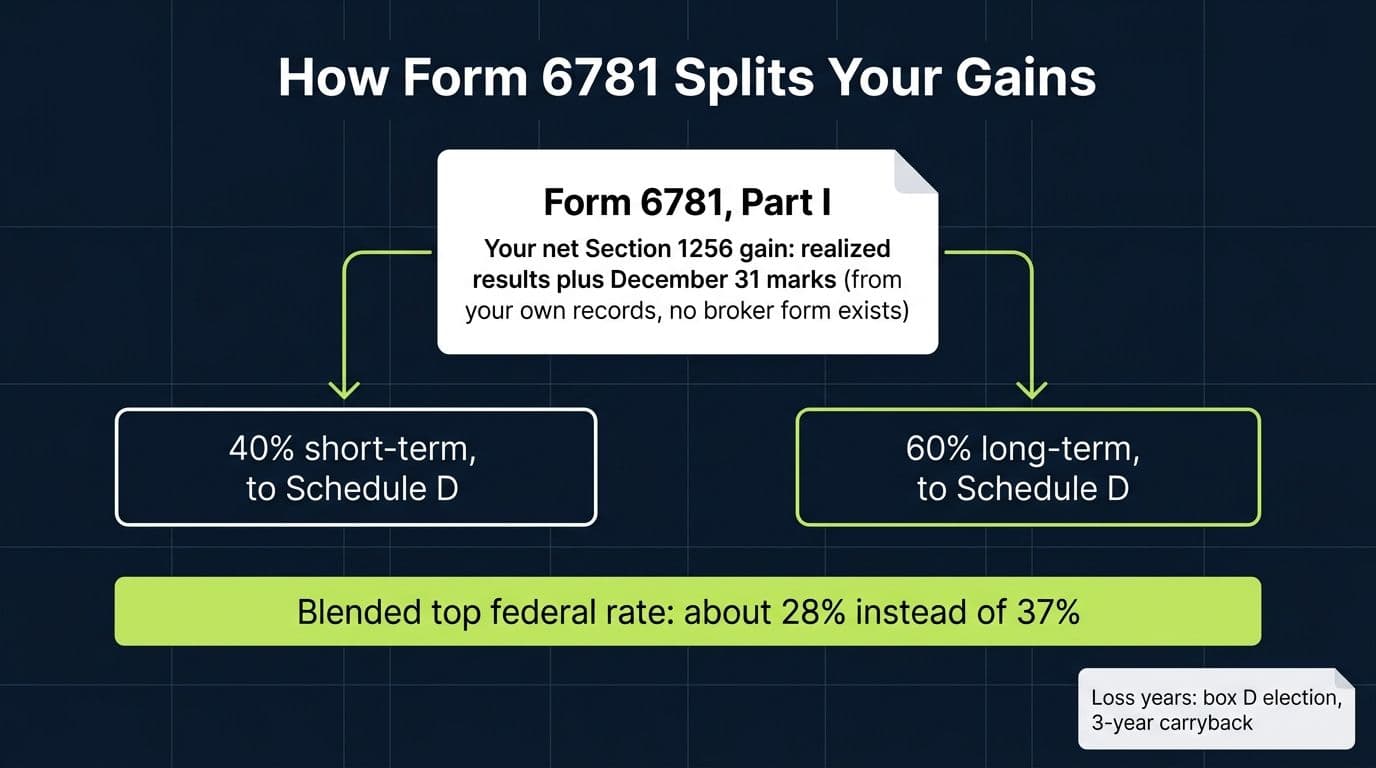

Section 1256 gains and losses go on Form 6781, Gains and Losses From Section 1256 Contracts and Straddles. For a straightforward trader the flow is short:

- Part I, Line 1: list each account or contract group with its loss in column (b) and gain in column (c). Because no platform sends you a 1256-formatted 1099-B, you attach your own computation built from trade history exports: realized results plus the December 31 mark on open positions.

- Lines 2 through 7: net everything to a single number. This is also where the loss carryback election interacts (more below).

- Line 8: 40% of the net flows to Schedule D as short-term capital gain or loss.

- Line 9: 60% flows to Schedule D as long-term. The blended rate happens automatically from there.

Next year, reverse the marks: positions taxed at $0.62 on December 31 have their basis adjusted, so only movement after year end is taxed when they settle.

Practical notes from returns we've actually filed. Keep the export files, not just the summary, because your Form 6781 numbers won't match any IRS-received document and you want the reconstruction to be trivial if asked. Compute the year-end marks from the exchange's official settlement prices and save a screenshot or export of those too. And report interest, bonuses, and any crypto-funding gains separately; they are not 1256 items even if the trades are.

Losses: The Three Year Carryback Nobody Else Gets

Section 1256 comes with one more feature worth understanding before you decide anything: net 1256 losses can be carried back three years, but only against prior Section 1256 gains, with the 60/40 character preserved. You make the election by checking box D on Form 6781 and filing an amended return for the carryback year.

Say Priya takes the position in 2026, pays tax on $21,100, and then has a brutal 2027: a net Section 1256 loss of $9,000. She can carry that loss back against her 2026 1256 gains and recover roughly $1,674 of 2026 tax (60% of $9,000 at 15% plus 40% at 24%). No other retail loss regime offers that; capital losses only carry forward, and gambling losses die the year they happen.

The asymmetry to notice: the carryback only helps if your prior-year gains were also 1256 gains. A trader who used ordinary treatment in 2026 and switches theories in 2027 to harvest a carryback has built a consistency problem an examiner can see from across the room. Whatever you choose, the loss rules are one more reason to choose once.

For completeness: under the other treatments, capital losses offset capital gains plus $3,000 of ordinary income per year with carryforward, ordinary-treatment losses net within the activity, and gambling losses deduct only for itemizers, only against winnings, and only up to 90% of losses from 2026. We break that last regime down in our gambling loss deduction guide, because for event contract traders the loss rules are where characterization stops being academic.

Form 8275: How to Take an Unproven Position Without Inviting Penalties

Everything above says the same thing: the Section 1256 position on event contracts is arguable and unproven. Tax law has a specific tool for exactly that situation, and almost nobody outside the profession knows it exists.

Form 8275, the Disclosure Statement, lets you flag a return position that isn't supported by clear authority. Disclosure matters because of how accuracy-related penalties work: if the IRS later disagrees with a significant position, a 20% substantial-understatement penalty can apply, but adequate disclosure of a position with a reasonable basis generally protects you from it. You'd still owe the tax difference and interest if you lose the argument. You would not owe the penalty, and you've converted "aggressive filer" into "taxpayer who told us exactly what they were doing."

What we put behind a Section 1256 event contract position in practice:

- A written memo, prepared before filing, walking the statute: qualified exchange satisfied (with the DCM designations named), the door relied on (usually nonequity option), and the honest treatment of the swap exclusion.

- Form 8275 identifying the position, the contracts, and the amounts.

- Consistent application: all qualifying venues, all positions, marks included, both directions, every year.

- Clean separation of non-1256 income: interest, bonuses, and anything from venues that fail the exchange prong.

Whether the position is worth taking at all is a facts question. The rate benefit scales with your bracket and your profit; the costs are the year-end mark, the documentation burden, and living with unresolved law. At $2,000 of profit in the 22% bracket, 60/40 saves about $110 and is rarely worth the apparatus. At $200,000 of profit in the top bracket, it's worth roughly $20,000 a year, and the apparatus is cheap by comparison. That's the honest frame: this is a position you buy with documentation, and it has a price floor.

Pro Tip

If a preparer offers you 60/40 treatment on event contracts without mentioning mark to market, the swap exclusion, or Form 8275, they have not done the analysis. The rate is the last step of this position, not the first.

Should You Take the Position?

Straight talk, the way we'd give it across a desk.

The Section 1256 position is probably not for you if: your profits are small, you take the standard deduction and just want simplicity, you can't produce clean trade-level records, or your activity is mostly on venues that fail the exchange prong. Report ordinary income or a capital position and sleep fine; on most facts the rate difference is modest.

The position deserves a real conversation if: you're in a high bracket with five or six figures of event contract profit on CFTC-designated exchanges, you can document everything, you understand the year-end mark, and you're prepared to hold the position consistently, including through loss years where the carryback becomes your friend. On those facts, the annual savings justify professional analysis several times over.

Either way, do not improvise it. The gap between a defensible Section 1256 position and a penalty exposure is a memo, a disclosure form, and consistency. Those are cheap. Reconstructing them after an IRS notice is not.

Get the Section 1256 Analysis Done Right

Flat-fee preparation for prediction market traders: characterization analyzed and documented, Form 6781 and Form 8275 handled, marks computed, return signed by a CPA who has taken this position and defended it.

Book a callFAQ: Section 1256 and Event Contracts

Frequently Asked Questions

What is a Section 1256 contract?

A contract on the statutory list in Section 1256(b): regulated futures contracts, foreign currency contracts, nonequity options, dealer equity options, and dealer securities futures contracts. Qualifying contracts are marked to market at year end and taxed on a 60/40 split, 60% long-term and 40% short-term, regardless of holding period.

What is the 60/40 rule for Section 1256 contracts?

All Section 1256 gains and losses are treated as 60% long-term and 40% short-term capital gain or loss no matter how long you held the contract. Because long-term rates top out at 20% while ordinary rates reach 37%, the blend caps the effective federal rate near 28% and usually lands well below it.

Do Kalshi event contracts qualify for Section 1256 treatment?

Unresolved. Kalshi is a CFTC-designated contract market, which satisfies the qualified board or exchange requirement, but whether binary event contracts fit any of Section 1256's enumerated contract types has no IRS ruling or case law behind it. It's a defensible documented position for some traders, not a default.

Are event contracts regulated futures contracts?

Arguably not in the technical sense. Section 1256(g)(1) requires that deposits and withdrawals depend on a system of marking to market, which describes daily variation margin. Most event contracts are fully collateralized binaries with no daily cash settlement, so the stronger pro-1256 argument usually runs through the nonequity option definition instead.

What is the swap exclusion in Section 1256(b)(2)(B)?

A Dodd-Frank provision that excludes swaps and similar agreements from Section 1256 treatment. Because the CFTC has described event contracts as binary options that are swaps in other contexts, the exclusion is the strongest argument against 60/40 treatment for prediction markets. Whether an exchange-listed binary contract is a similar agreement is the unresolved core of the whole question.

Does Kalshi report trades as Section 1256 contracts?

No. Kalshi issues no 1099 covering event contract trading profits at all, just a profit and loss statement plus narrow forms for interest, rewards, and crypto transfers. If you claim Section 1256 treatment, your Form 6781 numbers come from your own records, not from any broker form.

Does Robinhood report event contracts under Section 1256?

No. Robinhood reports actual regulated futures in the Section 1256 section of its 1099-B but explicitly keeps event contracts out of it, providing only an Event Contracts Annual Statement that it labels as not a substitute tax reporting form. That reporting choice is a meaningful signal about how platform counsel reads the law.

Do Polymarket trades qualify for Section 1256?

Only trades on Polymarket US, which has operated as a CFTC-designated contract market since November 2025, can even reach the argument. Pre-2026 offshore Polymarket activity fails the qualified exchange prong outright, so no credible Section 1256 position exists for it.

Where do I report Section 1256 contracts on my tax return?

On Form 6781. Part I nets your gains and losses including the December 31 mark on open positions, then 40% flows to Schedule D as short-term and 60% as long-term. Interest, bonuses, and other side income are reported separately.

How does mark to market work for event contracts under Section 1256?

Every position still open on December 31 is treated as sold at fair market value that day, so unrealized gains are taxed and unrealized losses deducted in the current year, with basis adjusted so nothing is taxed twice. You cannot claim the 60/40 rate on closed trades and skip the year-end mark on open ones.

Can Section 1256 losses be carried back?

Yes. Net Section 1256 losses can be carried back up to three years, but only against prior Section 1256 gains, with the 60/40 character preserved. You make the election by checking box D on Form 6781 and amending the earlier return. It's the only retail loss carryback in the code.

Do I need to file Form 8275 to claim 60/40 on event contracts?

It's not mandatory, but we recommend it. Form 8275 discloses a position that lacks clear authority, and adequate disclosure of a reasonable-basis position generally protects you from the 20% substantial-understatement penalty if the IRS later disagrees. Pair it with a written analysis prepared before you file.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Prediction Market Taxes (2026): How Kalshi, Polymarket, Robinhood and Every Major Platform Gets Taxed

How prediction market taxes work on Kalshi, Polymarket, Robinhood and more. A CPA splits platforms by settlement type and shows exactly what to report.

Kalshi Taxes (2026): A CPA's Guide to the Forms You'll Get, the One You Won't, and What You Owe

Kalshi sends 1099s for interest, rewards, and crypto conversions, but nothing for your trading profit. A CPA walks through every form, four tax treatments, and one full worked year.

Robinhood Prediction Market Taxes (2026): The Statement You Get, the 1099 You Don't, and What You Owe

Robinhood issues no 1099 for event contracts, just an Annual Statement the IRS never sees. A CPA explains the form gap, four tax treatments, and a full worked year.

The New Gambling Loss Deduction Rules (2026): The 90% Cap, the Itemizing Trap, and What It Means for Event Contract Traders

From 2026, gambling losses deduct at only 90%, itemizers only. A CPA runs the phantom income math, the standard deduction trap, the session question, and what event contract and crypto traders should do about it.