Prediction Market Taxes (2026): How Kalshi, Polymarket, Robinhood and Every Major Platform Gets Taxed

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓All prediction market profits are taxable income. No platform withholds taxes, and no minimum threshold makes small wins exempt.

- ✓The settlement rail is the key tax fact: fiat-settled platforms (Kalshi, Robinhood, PredictIt, ForecastEx) pay dollars and issue some forms; crypto-settled platforms (Polymarket, Limitless, SX Bet, Drift BET) pay USDC and issue none.

- ✓Kalshi provides a P&L statement plus limited 1099s (INT, MISC, B, DA) but no comprehensive 1099 for event contract trading profits. Robinhood issues no 1099 for event contracts at all.

- ✓The IRS has not ruled on characterization: capital asset, ordinary income, gambling, and Section 1256 treatments are all in play.

- ✓From tax year 2026, the One Big Beautiful Bill Act caps gambling loss deductions at 90%, which can create taxable phantom income for break-even traders.

Pro Tip

Written by Garrett Taylor, CPA (License #133092). Reviewed by Leanne Grant, EA (#00167954-EA). Last updated: July 2, 2026.

Quick answer: Yes, prediction market winnings are taxable, on every platform, at any amount. But your tax season looks completely different depending on one thing: whether your platform settles in dollars (Kalshi, Robinhood, PredictIt, ForecastEx) or in crypto (Polymarket, Limitless, Drift BET). Fiat platforms send some tax forms and keep things simple. Crypto-settled platforms send nothing and add a whole second tax layer.

Prediction markets went mainstream fast. You can now trade the Fed, the World Cup, and the weather on your phone, and Americans put over $3.3 billion into Polymarket's 2024 presidential markets alone.

The tax rules did not go mainstream with them.

Here's the problem: the IRS has never said how prediction market winnings should be taxed. Not for Kalshi, not for Polymarket, not for the Robinhood contracts riding on top of Kalshi's exchange. Meanwhile the platforms send you anywhere from partial tax forms to absolutely nothing.

We file returns for prediction market traders across every major platform, and in this guide we'll give you the map: which platforms send which forms, how the crypto-settled exchanges differ from the dollar ones, what the four possible tax treatments are, and a worked example showing the same bet taxed on two different rails.

Let's get into it.

Are Prediction Market Winnings Taxable?

Yes. Every time.

Section 61 of the tax code taxes all income from whatever source derived, and there's no carve-out for event contracts. If you bought a Yes contract for $0.40 and it settled at $1.00, the $0.60 is income. If you sold a position early at a profit, that's income too.

Three things people get wrong immediately:

- There's no $600 free pass. The $600 figure is a form-issuance threshold for platforms, not a tax exemption for you. Income is taxable from dollar one.

- No form does not mean no tax. Most prediction market activity generates no comprehensive 1099 anywhere. The reporting obligation is yours either way.

- Nothing is withheld. Unlike a paycheck, your winnings arrive gross. Big year? Plan for the bill, and consider estimated payments.

So the "do I owe taxes" question is easy. The real questions are what forms exist, what rate applies, and how losses work. All three depend on which platform you're using. Which brings us to the split that organizes this entire guide.

The One Question That Decides Your Tax Season: How Does Your Platform Settle?

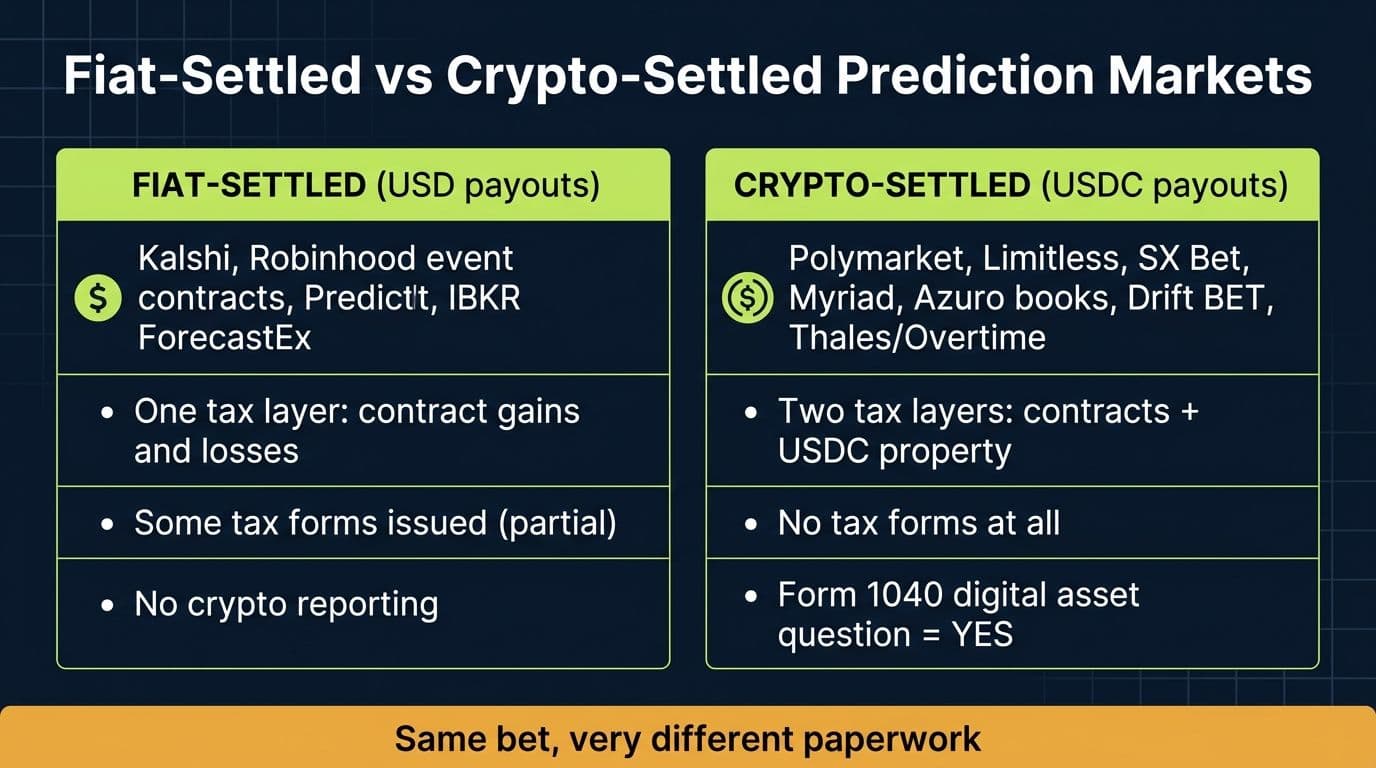

Forget the platform marketing. For prediction market taxes, every platform belongs to one of two families:

Fiat-settled platforms pay you in US dollars. You deposit dollars, you win dollars, you withdraw dollars. Tax-wise there's exactly one thing happening: gains and losses on event contracts.

Crypto-settled platforms pay you in cryptocurrency, almost always the stablecoin USDC. And because the IRS treats digital assets as property, every USDC movement is itself a potential tax event. You get the event contract layer plus a crypto layer stacked on top, and you'll answer "yes" to the Form 1040 digital asset question.

Here's the full map as of 2026:

Prediction Market Platforms by Settlement Type (2026)

| Platform | Settlement | Regulated? | Tax Forms Issued | Crypto Tax Layer? |

|---|---|---|---|---|

| Kalshi | USD | CFTC DCM | P&L statement; 1099-INT, 1099-MISC, 1099-B, 1099-DA in limited cases | Only if you deposit/withdraw crypto |

| Robinhood event contracts | USD | CFTC (via Kalshi + Robinhood Derivatives) | None for event contracts; annual statement only | No |

| PredictIt | USD | CFTC no-action letter | 1099-MISC at $600+ net profit | No |

| Interactive Brokers ForecastEx | USD | CFTC DCM | Consolidated 1099 (1099-MISC quirks, see below) | No |

| Polymarket | USDC (Polygon) | CFTC DCM since Nov 2025 | None | Yes |

| Limitless Exchange | USDC (Base) | Offshore/on-chain | None | Yes |

| SX Bet | USDC | Offshore/on-chain | None | Yes |

| Myriad | Crypto (Abstract/Linea) | On-chain | None | Yes |

| Azuro-based books | USDC/USDT pools | On-chain protocol | None | Yes |

| Drift BET | USDC (Solana) | On-chain | None | Yes |

| Thales / Overtime | Crypto (Optimism/Arbitrum) | On-chain | None | Yes |

Bold takeaway: if your payout arrives in USDC, you have crypto taxes now, even if you never touched Bitcoin in your life.

Let's walk each family.

Fiat-Settled Platforms: Taxes on Kalshi, Robinhood, PredictIt and ForecastEx

Kalshi Taxes: What You Actually Get (and Don't)

For the form-by-form breakdown, a full worked trading year, and the filing workflow, see our complete Kalshi taxes guide.

Kalshi is the flagship US prediction market: a CFTC-regulated Designated Contract Market that settles everything in dollars. Because "Kalshi taxes" generates more searches than any other platform, let's be surgical about what Kalshi actually provides, straight from Kalshi's own documentation:

- A Profit and Loss (PnL) statement summarizing your trading activity: profits, losses, and fees, calculated FIFO. Find it under Account, then Tax Info. This is your best starting document, but it is not an IRS information return.

- 1099-INT if Kalshi paid you interest on cash balances.

- 1099-MISC for credits and rewards (referral bonuses and promos), not trading profits.

- 1099-B covering proceeds from broker transactions involving crypto transfers.

- 1099-DA for digital asset transactions, issued through its custodian ZeroHash, if you funded with crypto.

Notice what's missing? Kalshi does not issue a comprehensive 1099 covering your event contract trading gains. Plenty of articles claim Kalshi "sends a 1099 if you profit $600+." That's not how it works. The 1099-MISC covers promos, and your actual trading P&L arrives on a statement, not an IRS form.

What that means practically: download your full trade history, compute net profit (proceeds minus cost, minus fees), and report it yourself. Most Kalshi filers report the net figure as Other Income on Schedule 1, Line 8z, or take a capital asset position on Form 8949. Some take the aggressive Section 1256 position (more below).

Pro Tip

Even when a Kalshi form does arrive, reconcile it against your own records before filing. A 1099-MISC for a $700 referral bonus is rewards income; don't accidentally double-count it inside your trading P&L.

Robinhood Prediction Market Taxes: The Form That Never Comes

Robinhood's event contracts run through Robinhood Derivatives LLC, a CFTC-registered futures commission merchant, and execute on Kalshi's exchange. Dollars in, dollars out, familiar app.

Here's what surprises people: Robinhood has stated it will not issue 1099s for event contract trades. You get an "Event Contracts Annual Statement" instead, which Robinhood itself labels as not a substitute tax reporting form.

So despite trading on the most mainstream brokerage app in America, you're in the same self-reporting position as a Kalshi trader: export the statement, compute net gain or loss, pick a defensible treatment, report it. The trades don't appear on the consolidated 1099 that covers your Robinhood stocks.

PredictIt Taxes

PredictIt, the academic-rooted political market, is the one platform that does send a profit-based form: a 1099-MISC if your net profit hits $600 or more in a calendar year (net of losses and fees). Below $600, no form, but the income is still reportable. PredictIt income generally lands on Schedule 1 as other income.

Interactive Brokers ForecastEx

ForecastEx is a CFTC-designated contract market owned by Interactive Brokers, offering yes/no forecast contracts through IBKR accounts. You'll get IBKR's consolidated 1099 package, but be careful: traders have found ForecastEx proceeds reported on 1099-MISC at $1.00 per contract regardless of what they actually received, which can wildly overstate income if you don't adjust. Report the true economics (actual proceeds minus actual cost) and keep documentation showing how your numbers reconcile to the form.

Action steps for fiat platform traders:

- Download every platform's year-end statement and full trade export in January.

- Compute net P&L yourself; never assume a form is complete or correct.

- Note which forms went to the IRS (they get matched) and reconcile before filing.

Crypto-Settled Platforms: Where Prediction Market Taxes Get Complicated

Now the other family. Polymarket, Limitless Exchange, SX Bet, Myriad, Azuro-based sportsbooks, Drift BET on Solana, Thales and Overtime: all of these settle positions in crypto, usually USDC.

That single design choice triggers three tax consequences that fiat traders never face:

1. Every payout is a crypto acquisition. Win 2,500 USDC and you now hold property with a $2,500 cost basis. Sell it, swap it, or spend it later and that's a second taxable disposal. Our guide to crypto-to-crypto trades covers why each hop matters.

2. No forms, ever. None of these platforms issues a 1099 of any kind. Polymarket, even after becoming a CFTC-regulated US exchange in January 2026, still issues no 1099-B, 1099-DA, or W-2G. The reconstruction burden is 100% yours, position by position, from on-chain data.

3. The IRS still sees you. Every trade lives permanently on a public blockchain, and the moment your USDC touches a KYC exchange like Coinbase, the exchange's Form 1099-DA reports your proceeds to the IRS, usually with a blank cost basis. Unexplained proceeds are precisely what triggers automated mismatch notices. If one already found you, here's how to respond to an IRS crypto notice.

Polymarket is by far the biggest of these, and it deserves its own deep dive: the four-framework analysis, a full 10-position worked filing, and the 1099-DA off-ramp trap are all covered in our complete guide to Polymarket taxes.

Pro Tip

"Crypto gambling taxes" shortcuts on Reddit often suggest reporting only your final cash-out. That's wrong on both layers: the contract gains were taxable when positions settled, and the USDC disposals are taxable when they happen. Reporting only the off-ramp understates income in the trading years and mismatches the blockchain record.

How Is Prediction Market Income Characterized? (The Honest Answer)

Here's the uncomfortable truth at the center of prediction market taxes: the IRS has never issued guidance saying which tax regime these contracts belong to. Thomson Reuters ran a piece in June 2026 on the IRS's silence on prediction market winnings in which a Baker Tilly tax principal predicted the question is "probably headed to the Supreme Court."

Until then, four frameworks compete. In brief:

The Four Candidate Tax Treatments for Prediction Market Winnings

| Treatment | Reported On | Rate | Loss Rules |

|---|---|---|---|

| Ordinary income (common default) | Schedule 1, Line 8z | 10-37% | Net losses generally deductible |

| Capital asset | Form 8949 + Schedule D | Short-term = ordinary; long-term 0/15/20% | Offset gains; $3,000/yr vs ordinary income; carryforward |

| Gambling | Schedule 1 + Schedule A | 10-37% on gross winnings | Itemizers only; 90% cap from 2026 |

| Section 1256 | Form 6781 | 60/40 blend (max ~28%) | Netted; 3-year carryback |

The framework fight matters most in two places:

The Section 1256 question, which is strongest for Kalshi-style platforms. Section 1256 gives regulated futures contracts a blended 60% long-term / 40% short-term rate with mark-to-market accounting. Kalshi offers its contracts on a CFTC-designated exchange, and commentators (including a widely cited Forbes analysis calling prediction markets the tax-advantaged way to gamble on sports) have argued the 60/40 treatment applies. But it's genuinely unsettled: the CFTC has classified event contracts as binary options that are swaps, and the Dodd-Frank swap exclusion in Section 1256(b)(2)(B) may knock them out. KPMG's analysis treats the classification as an open question with materially different outcomes on each side. If you take a 1256 position, document the analysis and consider a Form 8275 disclosure.

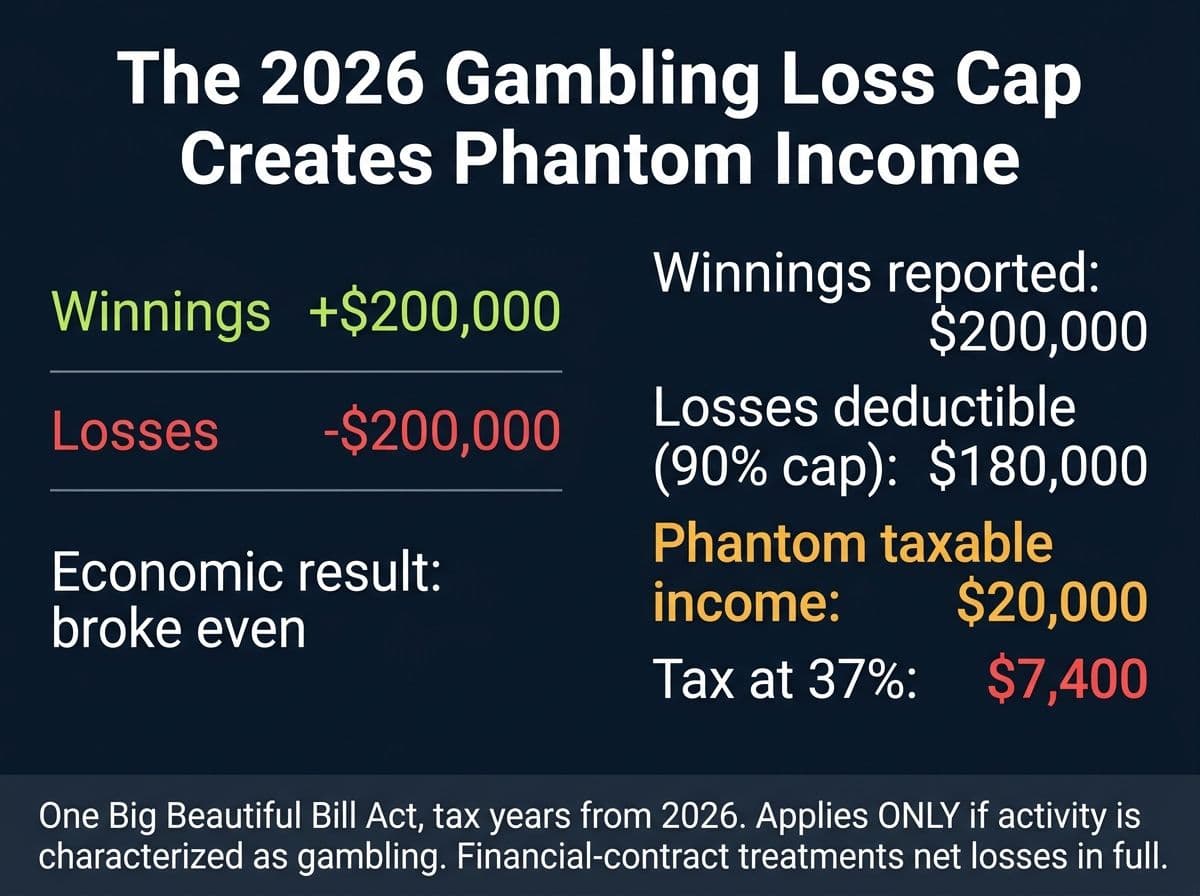

The gambling question, which is now expensive to lose. A March 2026 Ipsos poll found 61% of Americans think prediction market trading is closer to gambling than investing. If the IRS or courts agree, winnings are ordinary income under the gambling income rules, and losses deduct only for itemizers, only against winnings. And starting with 2026 returns, the One Big Beautiful Bill Act caps the gambling loss deduction at 90% of losses.

Watch the phantom income that creates:

Win $200,000, lose $200,000, break exactly even. Under 2026 gambling treatment you report $200,000 of winnings but deduct only $180,000 of losses. You owe tax on $20,000 you never made: $7,400 at a 37% marginal rate. Financial-contract characterization (ordinary, capital, or 1256) avoids the cap entirely because gains and losses net in full. That asymmetry is already pushing sports bettors from sportsbooks toward event contracts, and it's why the characterization fight has real stakes.

“On identical facts, the gap between the best and worst characterization can be a five-figure tax difference. Nobody can promise you the IRS's answer, because there isn't one yet. What a good CPA gives you is a position your records can defend.”

, Garrett Taylor, CPA

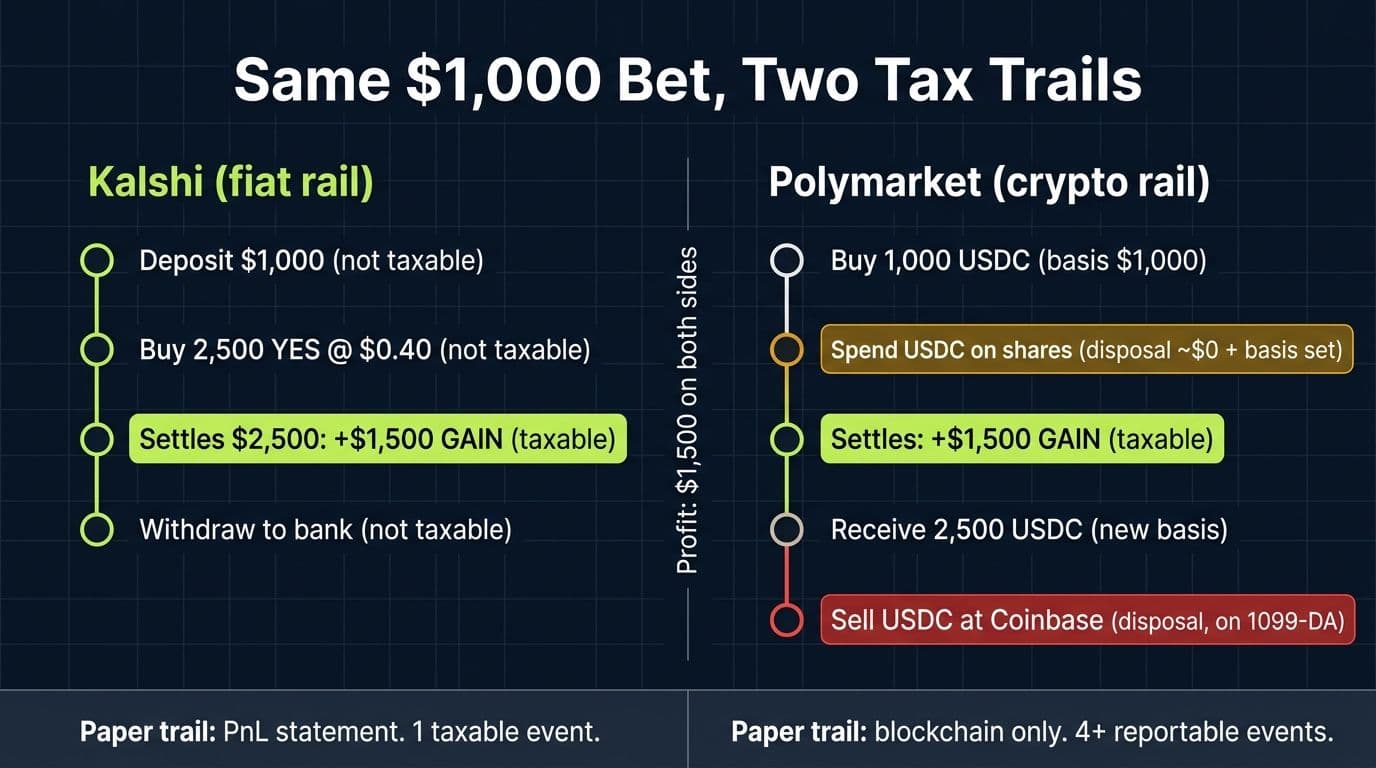

Worked Example: The Same $1,000 Bet on Kalshi vs Polymarket

Let's make the settlement split concrete with one bet, two platforms.

Jordan puts $1,000 into "Team USA reaches the semifinal: YES" at $0.40 per contract, once on Kalshi, once on Polymarket. That's 2,500 contracts each. Team USA delivers. Both positions settle at $1.00, paying $2,500 each. Economic profit: $1,500 per platform. Identical bets, identical profits.

Now the tax paperwork:

On Kalshi (fiat rail):

- Deposit $1,000 by bank transfer. Not a taxable event.

- Buy 2,500 YES at $0.40. Not a taxable event (basis established: $1,000).

- Settlement pays $2,500. Taxable event: $1,500 gain.

- Withdraw to bank. Not a taxable event.

- Paper trail: Kalshi PnL statement shows the profit. No 1099 for the trade. Jordan reports $1,500 on Schedule 1 (or Form 8949 under a capital position). Done.

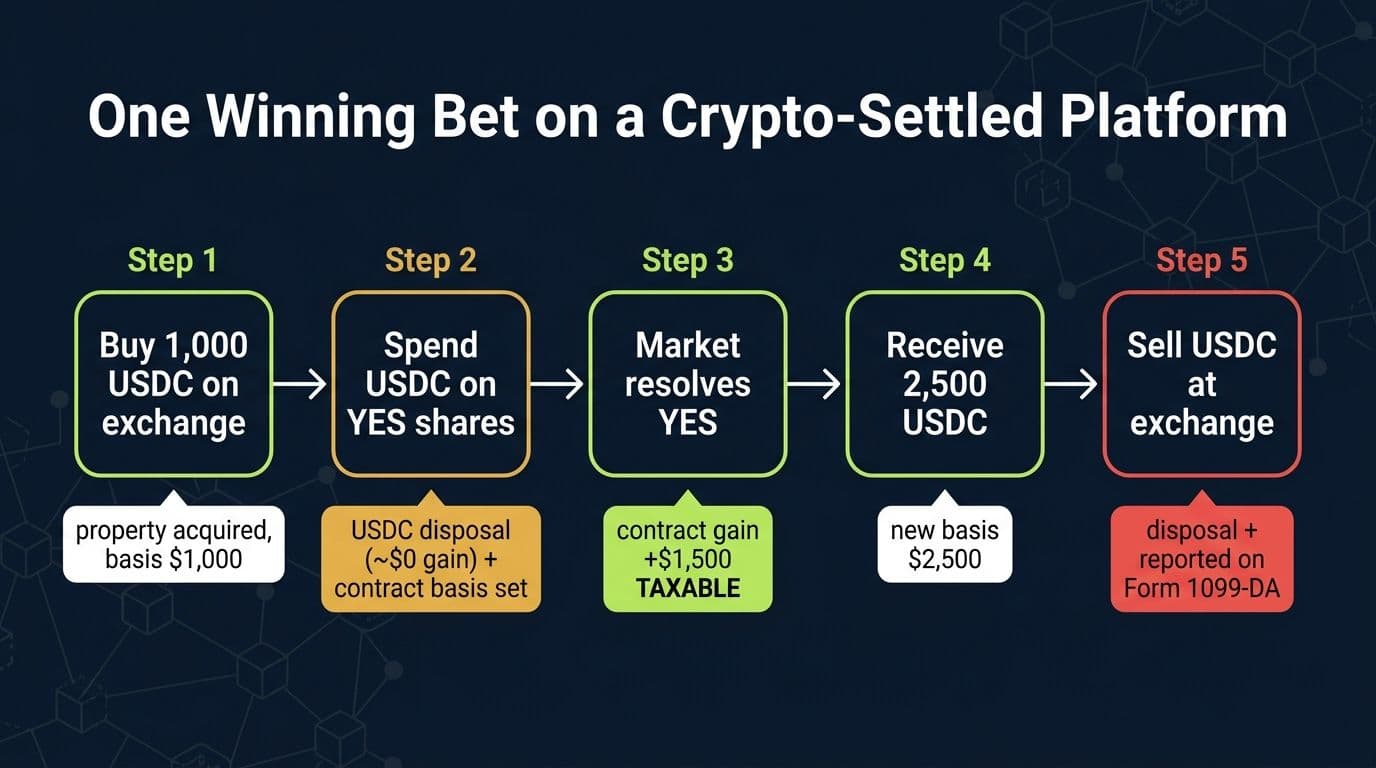

On Polymarket (crypto rail):

- Buy 1,000 USDC on Coinbase for $1,000. Acquisition of property, basis $1,000.

- Bridge to Polygon and spend USDC on 2,500 YES shares. Two things happen: a disposal of the USDC (gain roughly $0 since the peg held) AND basis of $1,000 established in the contracts.

- Settlement pays 2,500 USDC. Taxable event: $1,500 gain on the contracts, plus acquisition of 2,500 USDC with a fresh $2,500 basis.

- Send USDC back to Coinbase and sell for $2,500. Disposal of property (gain roughly $0), and Coinbase reports $2,500 of proceeds to the IRS on Form 1099-DA, likely with a blank basis field since the USDC arrived from an external wallet.

- Jordan reports the $1,500 contract gain, reports the USDC disposals, and checks "yes" on the digital asset question. Records come from the Polygon blockchain and Polymarket trade history, because no form summarizes any of it.

Same profit. Same tax owed (under matching treatments). Roughly four times the reporting surface on the crypto rail, plus an IRS-visible off-ramp that must reconcile with the return. That's the practical meaning of "prediction market taxes depend on settlement type."

Trading on Both Rails?

Garrett files prediction market returns across Kalshi, Robinhood, Polymarket and the on-chain platforms, with the crypto layer reconciled to the blockchain. One conversation now beats a mismatch notice later.

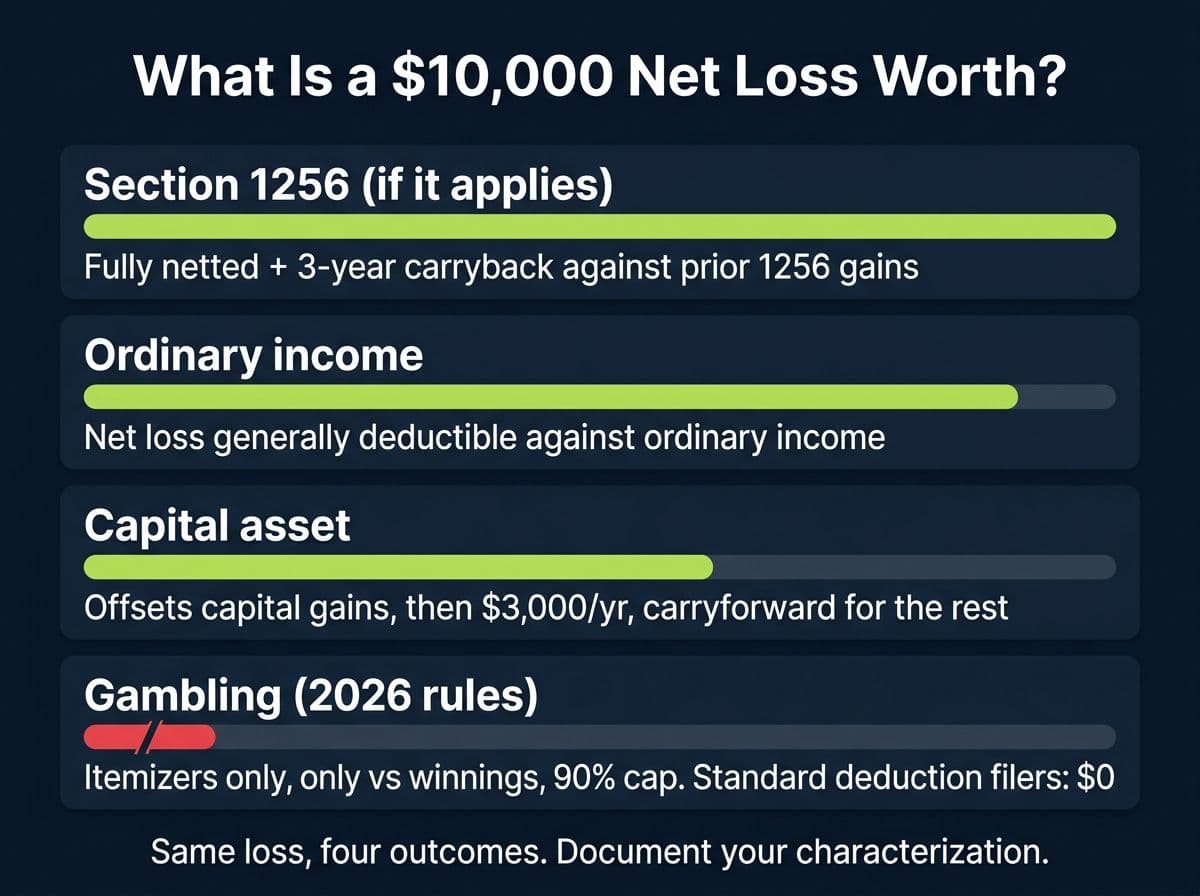

Book a callHow Losses Work on Prediction Markets (Read Before Year-End)

A losing year hurts twice if you file it wrong. Loss treatment by characterization:

- Ordinary income treatment: net trading losses are generally deductible against ordinary income, without the gambling limitations.

- Capital treatment: losses offset capital gains from anywhere (stocks, crypto, other markets), then $3,000 per year against ordinary income, with indefinite carryforward.

- Gambling treatment: losses help only if you itemize, only against winnings, and only up to 90% of losses starting in 2026. Standard-deduction filers get nothing.

- Section 1256 (if it applies): losses net fully and can be carried back three years against prior 1256 gains, the only framework with a carryback.

Two extras worth knowing. First, the wash sale rule doesn't currently reach event contracts or crypto, so exiting a losing position and re-entering doesn't void the loss under present law (the same logic as crypto wash sales). Second, on crypto-settled platforms your losses only exist if your cost basis is documented, which is a records problem, not a law problem. Choose and document a basis method before the trade count gets away from you; our cost basis guide shows how.

State Taxes on Prediction Markets: The Quiet Second Bill

Federal characterization is only half the fight. States are moving faster and more aggressively than the IRS:

- States that tax gambling winnings gross with no loss deduction are brutal if gambling characterization applies: $60,000 of wins and $55,000 of losses can mean state tax on the full $60,000.

- New Jersey and others don't conform to some federal treatments, so a Section 1256 or long-term capital position at the federal level may not translate.

- Kentucky enacted a 14.25% excise tax on prediction market operators in April 2026 (now in litigation), and the New York attorney general is pushing to have event contracts declared gambling. Where states land will shape your state return.

If you moved states mid-year or trade at volume in a high-tax state, this deserves a professional look before you file, not after.

Common Prediction Market Tax Mistakes

The recurring five, across every platform:

- Assuming no form means no tax. The top mistake on both rails.

- Trusting a platform form as complete. Kalshi's 1099-MISC covers rewards, not P&L. ForecastEx 1099s can overstate proceeds. Reconcile everything.

- Ignoring the crypto layer on USDC-settled platforms. The 1099-DA off-ramp mismatch is how the IRS finds these accounts.

- Mixing frameworks opportunistically. Capital treatment for wins and gambling treatment for losses is not a position, it's an audit finding.

- Reconstructing a year of on-chain trades in April. Start in January. Or better, now.

Action steps:

- List every platform you touched this year and classify it: fiat-settled or crypto-settled.

- Pull trade exports and year-end statements from each.

- For crypto rails, pull wallet histories and match every on-ramp and off-ramp.

- Pick one characterization per activity, write down why, and apply it consistently.

- If your volume is five figures or the framework choice moves real money, get a specialist. Here's what a crypto-savvy CPA costs and how to choose one.

93% notice reduction

Across 200+ IRS crypto and digital asset notices we've handled, nearly all were resolved with reconstructed records and a documented, consistent reporting position.

Prediction markets sit inside your bigger tax picture too. If you also hold crypto, stake, or trade DeFi, start with our complete crypto tax guide to see how it all fits together.

Get Your Prediction Market Year Handled

Flat-fee filing for prediction market and crypto traders: records reconstructed, framework documented, return signed by a CPA who does this every season.

Book a callFAQ: Prediction Market Taxes

Frequently Asked Questions

Do you have to pay taxes on Kalshi?

Yes. All Kalshi profits are taxable income regardless of amount, and Kalshi withholds nothing. Download your PnL statement and trade history, compute net profit, and report it. Most filers use Schedule 1 (ordinary income) or Form 8949 (capital treatment); some take an aggressive Section 1256 position with professional support.

Does Kalshi give tax forms?

Partially. Kalshi provides a Profit and Loss statement in the app, plus 1099-INT for interest, 1099-MISC for credits and rewards, 1099-B for crypto transfer proceeds, and 1099-DA for digital asset transactions through ZeroHash. It does not issue a comprehensive 1099 covering your event contract trading profits.

Will Kalshi send me a 1099?

Only in specific situations: interest paid (1099-INT), promotional credits or rewards (1099-MISC), or crypto-related transactions (1099-B or 1099-DA). Your trading P&L itself does not arrive on a 1099, so never wait on a form before calculating what you owe.

Do I get taxed if I made less than $600?

Yes. The $600 figure is a reporting threshold that determines when platforms like PredictIt issue a 1099-MISC. It is not an income exemption. All prediction market profit is taxable from the first dollar, form or no form.

Does Robinhood send a 1099 for prediction markets?

No. Robinhood has stated it will not issue 1099s for event contract trades. You receive an Event Contracts Annual Statement, which Robinhood labels as not a substitute tax reporting form. You must compute and report gains yourself, separately from your Robinhood stock 1099.

Do you pay taxes on Polymarket?

Yes, and Polymarket adds a crypto layer: winnings arrive in USDC, which the IRS treats as property, and the platform issues no tax forms at all. See our full guide to Polymarket taxes for the four-framework analysis and a complete worked filing.

Are prediction markets taxed like sports betting?

Not necessarily, and that's the fight. Sportsbook winnings are clearly gambling income with W-2G withholding rules and the new 90% loss cap. Prediction market platforms argue their contracts are CFTC-regulated financial instruments that net gains and losses in full. The IRS hasn't ruled, which is why identical bets can produce different tax outcomes on different rails.

Can you deduct prediction market losses?

Usually, but the path depends on characterization. Capital treatment: offset gains plus $3,000 a year with carryforward. Ordinary treatment: net losses generally deductible. Gambling treatment: itemizers only, capped at 90% of losses from 2026. Section 1256, where it applies, allows full netting and a three-year carryback.

Are PredictIt winnings taxable?

Yes. PredictIt issues a 1099-MISC when your net profit reaches $600 in a year, and the income is generally reported as other income on Schedule 1. Below $600 you get no form, but the income remains reportable.

How much capital gains tax will I pay on $100,000 of prediction market profit?

If treated as short-term capital gains or ordinary income (the usual case, since contracts resolve quickly), roughly $24,000 to $35,000 federal depending on your bracket, plus state tax. If Section 1256 treatment applied, the 60/40 blend would cap the effective federal rate near 28% and often lands lower. At this size, characterization is worth a professional conversation before filing.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Polymarket Taxes (2026): A CPA's Guide to Reporting When There's No 1099

Polymarket sends no 1099, but your winnings are still taxable. A CPA explains the forms, the four tax treatments, and the USDC layer, with worked numbers.

The Ultimate Guide to Crypto Tax (2026 Edition)

The most comprehensive crypto tax guide online, written by a CPA who files 500+ crypto returns a year. Every taxable event, form, strategy, and 2026 update.

Crypto Cost Basis Methods: FIFO vs Specific ID vs HIFO

Compare FIFO, LIFO, HIFO, and Specific ID for crypto taxes. Worked example shows how the same sale produces 4 different tax bills. Updated for Rev. Proc. 2024-28 and 1099-DA.

Kalshi Taxes (2026): A CPA's Guide to the Forms You'll Get, the One You Won't, and What You Owe

Kalshi sends 1099s for interest, rewards, and crypto conversions, but nothing for your trading profit. A CPA walks through every form, four tax treatments, and one full worked year.