Kalshi Taxes (2026): A CPA's Guide to the Forms You'll Get, the One You Won't, and What You Owe

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

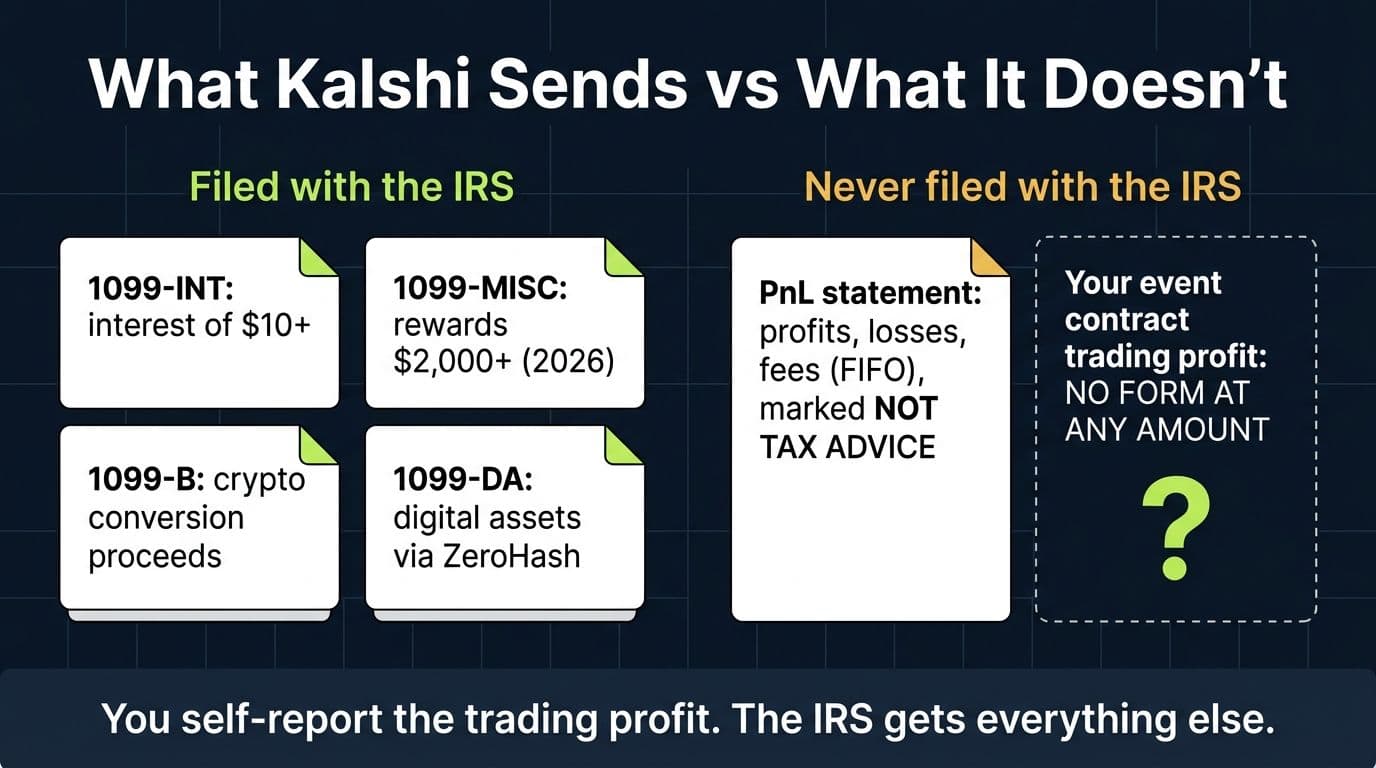

- ✓Kalshi issues 1099-INT, 1099-MISC, 1099-B, and 1099-DA forms in limited situations, but no comprehensive 1099 for event contract trades. Your trading P&L arrives on a statement, not an IRS form.

- ✓Everything Kalshi does report goes to the IRS too. The gap between what the IRS sees (interest, rewards, crypto conversions) and what it doesn't (your trading profit) is where filing mistakes happen.

- ✓The IRS has issued no guidance on event contracts. Filers choose between ordinary income, capital asset, Section 1256, and gambling treatment, and the choice changes the bill.

- ✓Depositing crypto into Kalshi is a taxable event: ZeroHash converts your BTC or USDC to dollars on arrival, and that conversion is a disposal of property.

- ✓From 2026, the One Big Beautiful Bill Act caps gambling loss deductions at 90% and raises the 1099-MISC threshold from $600 to $2,000, so even fewer Kalshi forms will arrive.

Pro Tip

Written by Garrett Taylor, CPA (License #133092). Reviewed by Leanne Grant, EA (#00167954-EA). Last updated: July 2, 2026.

Quick answer: Yes, Kalshi winnings are taxable, and Kalshi withholds nothing. The platform sends a few narrow tax forms (1099-INT for interest, 1099-MISC for rewards, 1099-B and 1099-DA for crypto conversions), but no form covers your actual event contract trading profit. You calculate that yourself from your trade history and PnL statement, then report it under one of four possible tax treatments. This guide walks through every form, a full worked year, and the exact numbers under each treatment.

You had a good year on Kalshi. You called the Fed, the weather, maybe a championship.

Then tax season arrived, and nothing in your Kalshi account adds up to anything a tax return recognizes. A PnL statement that says "not tax advice." Maybe a tiny 1099-INT. Nothing that mentions the thousands you actually made trading.

Here's the deal: Kalshi taxes confuse people precisely because Kalshi sends some forms but not the one that matters. We prepare returns for prediction market traders every season, and the Kalshi tax filings we review have a distinctive failure mode: people report what the forms show and skip what the forms don't. The IRS eventually notices the difference.

In this guide to Kalshi taxes, we'll walk through every document Kalshi issues and what each one covers, the four possible tax treatments and what each costs, one trader's complete year from trade log to filed forms, and the crypto and interest wrinkles almost nobody mentions.

Let's dig in.

Do You Have to Pay Taxes on Kalshi? (Yes, From the First Dollar)

Start with the rule that settles most questions about Kalshi taxes: under Section 61 of the tax code, all income is taxable unless Congress specifically exempts it. There is no exemption for event contracts, prediction markets, or "it was only a few hundred bucks."

So every profitable Kalshi outcome is income: a contract bought at $0.55 that settles at $1.00, a position sold early for more than you paid, interest on your cash balance, a referral bonus. All of it is taxable whether or not a form arrives, whether or not you withdrew to your bank, and whether you made $50 or $50,000. The $600 figure people quote is a form-issuance threshold for platforms, not a tax exemption for you. (And as we'll see, for 2026 that threshold isn't even $600 anymore.)

One more thing traders coming from W-2 jobs miss: Kalshi withholds no taxes. Every dollar of profit arrives pre-tax. If your winnings are large, the IRS expects quarterly estimated payments along the way, not one big check in April.

720 searches a month

More Americans search for Kalshi tax answers than for any other prediction market platform, and the IRS still hasn't published a single sentence of guidance on how event contracts are taxed.

What Tax Forms Does Kalshi Send? The Complete List

Kalshi differs from both a stock brokerage (comprehensive 1099-B) and Polymarket (nothing at all). It sits in the middle: four narrow forms, one statement, and a gap where the main form should be. Straight from Kalshi's own documentation, users who hit IRS reporting thresholds receive:

Every Tax Document Kalshi Provides (2026)

| Document | What It Covers | When You Get It | Filed With the IRS? |

|---|---|---|---|

| Form 1099-INT | Interest paid on your cash and position collateral | Interest of $10 or more for the year | Yes |

| Form 1099-MISC | Credits and rewards (referral bonuses, promos) | $600+ for 2025; $2,000+ for 2026 payments | Yes |

| Form 1099-B | Proceeds from crypto transfer transactions | If you deposited or converted crypto | Yes |

| Form 1099-DA | Digital asset reporting from ZeroHash | If you moved crypto through ZeroHash | Yes |

| PnL statement | Your trading profit, loss, and fees summary | Always available in Account, under Tax Info | **No** |

Each form has a trap in it, so let's take them one at a time.

Form 1099-INT: The Interest Form

Kalshi pays interest on your account, and not just on idle cash: under its APY program, interest accrues daily on your cash balance plus the value of your open positions, at a variable rate (3.25% as of this writing) passed through from Kalshi's banking partners and paid monthly. Leave $20,000 on the exchange through a season of trading and it earns the whole time, win or lose.

Nice feature, and taxable exactly like a savings account: ordinary interest income, no characterization debate. At $10 or more for the year, Kalshi sends a 1099-INT and files a copy with the IRS, and over $1,500 of total interest from all sources puts it on Schedule B.

The trap: interest income is completely separate from your trading P&L. It doesn't offset trading losses and doesn't belong inside your net profit calculation. And because interest is the one Kalshi number the IRS always sees, it anchors your account's existence in their systems. Report everything else accordingly.

Form 1099-MISC: The Rewards Form (and the Threshold That Just Changed)

Referral bonuses, deposit promos, and credits are ordinary income, reported on a 1099-MISC if you cross the threshold.

Here's what most guides haven't caught up with: the threshold changed. For 2025, platforms issued 1099-MISC forms at $600 or more. The One Big Beautiful Bill Act raised that to $2,000 for payments made in 2026, with inflation indexing after. So a $700 referral bonus generated a form in 2025 and generates nothing in 2026. It's still fully taxable either way. The form threshold changed; your obligation didn't.

Form 1099-B and 1099-DA: The Crypto Conversion Forms

These two confuse Kalshi traders more than everything else combined, so let's be precise. Kalshi's 1099-B does not cover your event contract trades. It covers proceeds from crypto transfer transactions: when you fund your account with bitcoin, USDC, SOL, or another supported asset, Kalshi's crypto partner ZeroHash converts it to dollars, and that conversion is a broker transaction with reportable proceeds. The 1099-DA is the digital asset version of the same reporting, issued through ZeroHash.

If you've never touched the crypto deposit option, you'll never see either form. If you have, there's a full section below on why that deposit was a taxable event all by itself.

The PnL Statement: Useful, Official-Looking, and Not a Tax Form

Your Profit and Loss statement lives in the Account tab under Tax Info. It summarizes trading profits, losses, and fees using first-in, first-out (FIFO) accounting. It is the single most useful document Kalshi gives you, and it is not filed with the IRS and not tax advice (Kalshi says so itself). Treat it as a starting point you verify against your full trade history, not a number you copy onto a return unexamined.

The Form That Never Arrives

Now the punchline. Notice what's missing: there is no comprehensive 1099-B or any other form covering your event contract trading activity. Not at $600 of profit, not at $600,000.

Plenty of articles claim "Kalshi sends a 1099 if you profit $600 or more." That's wrong: the $600 (now $2,000) threshold belongs to the 1099-MISC for bonuses and rewards. Your actual trading profit, the thing you're on Kalshi to make, rides on no form at all.

Which raises the obvious question.

Does Kalshi Report to the IRS?

Partially, and the shape of "partially" matters.

What the IRS receives: every 1099 Kalshi issues to you also goes to the IRS. Interest, rewards over the threshold, crypto conversion proceeds. The IRS also knows the account is KYC'd to your Social Security number, because Kalshi is a CFTC-regulated exchange with full identity verification.

What the IRS doesn't receive: any contract-level record of your trading. No proceeds, no basis, no net profit from event contracts.

Some traders read that gap as safety. We read it as the opposite. The partial forms create a visible trailhead: a 1099-INT for $142 tells the IRS an account exists and holds real money, and an examiner who pulls the thread gets to ask what else that account did. Meanwhile the reporting burden legally sits with you either way, on a regulated exchange that keeps complete records and can produce them under summons.

The honest framing: Kalshi reports enough to make you findable, and not enough to make your return for you. That combination only works out if you self-report properly.

“The Kalshi returns that go wrong are almost never fraud. They're people who reported the 1099-INT because a form showed up and skipped the trading profit because no form did. The IRS doesn't grade on which income came with paperwork.”

, Leanne Grant, EA

How Are Kalshi Winnings Taxed? The Four Possible Treatments

Here's the uncomfortable truth at the center of Kalshi taxes: the IRS has never said how event contracts are taxed. No revenue ruling, no notice, nothing. Business Insider put the question to tax economists in early 2026 and got shrugs; practitioners quoted by the trade press predict the classification fight ends up in court.

So we work from existing law, which offers four candidate frameworks. We covered the full cross-platform analysis in our prediction market taxes pillar guide; here's the Kalshi-specific version.

The Four Possible Tax Treatments of Kalshi Trading

| Treatment | Where It Goes | Loss Rules | Kalshi-Specific Note |

|---|---|---|---|

| Ordinary income | Schedule 1, Line 8z | Net losses generally deductible | The conservative default most filers use |

| Capital asset | Form 8949 + Schedule D | Offset gains; $3,000/yr vs ordinary income; carryforward | Nearly all Kalshi gains are short-term anyway |

| Section 1256 | Form 6781, 60/40 split | 3-year carryback of net losses | Strongest argument of any platform, still unsettled |

| Gambling | Schedule 1 + Schedule A | Itemizers only; 90% cap from 2026 | Least favorable; most practitioners avoid electing it |

Ordinary Income: The Conservative Default

Compute net profit (total proceeds minus total cost, minus fees), report it as Other Income on Schedule 1, Line 8z, labeled something like "Kalshi event contract trading." Taxed at your ordinary rate, with losses netting against gains within the activity.

Simple, defensible, low mismatch risk. Its cost: no preferential rates, ever. For most Kalshi traders that cost is zero, because positions resolve in days and short-term capital rates equal ordinary rates anyway.

Capital Asset: The Brokerage Analogy

A Kalshi contract is a transferable right you bought for consideration and disposed of by sale or settlement. Treat it as a capital asset under Section 1221 and each position goes on Form 8949, flowing to Schedule D.

The rate usually matches ordinary treatment (short holding periods mean short-term rates). The real difference is losses: capital losses offset capital gains from anything, stocks, crypto, other contracts, plus $3,000 a year against ordinary income, with indefinite carryforward. A losing Kalshi year and a winning stock year get to talk to each other.

Section 1256: The Kalshi-Shaped Question Mark

This is the treatment people email us about, because the upside is real. Section 1256 taxes qualifying regulated futures contracts on a 60/40 split: 60% long-term, 40% short-term, regardless of holding period, with mark-to-market at year end on Form 6781 and a three-year carryback for net losses.

The argument for Kalshi is stronger than for any other prediction market: it's a CFTC-regulated Designated Contract Market with standardized, exchange-traded contracts. A widely cited Forbes analysis went as far as calling prediction markets the tax-advantaged way to gamble on sports on exactly this theory.

The argument against: the CFTC has classified event contracts as binary options that are swaps, and Section 1256(b)(2)(B), added by Dodd-Frank, excludes most swaps from 60/40 treatment. KPMG's analysis treats the question as genuinely open with materially different outcomes on each side.

Two practical notes if you're tempted:

- 1256 is a package, not a rate. Mark-to-market means positions still open on December 31 get taxed on unrealized gains. Traders who want the 60/40 rate rarely think about the year-end mark.

- Take it as a documented position, not a vibe. Written analysis, consistent application, and consider a Form 8275 disclosure. Every 1256 return we've filed for a prediction market trader had a memo behind it.

Gambling: The Expensive Characterization

If Kalshi trading is wagering, winnings are ordinary income and losses fall under Section 165(d): deductible only if you itemize, only against winnings, and, from tax year 2026 under the One Big Beautiful Bill Act, only up to 90% of losses.

That 90% cap creates phantom income. Win $80,000 and lose $80,000 on Kalshi in 2026 under gambling treatment and you still have $8,000 of taxable income, because only $72,000 of the losses count. Break even in reality, pay tax anyway.

Most practitioners, us included, don't reach for gambling treatment on a regulated exchange where you're trading transferable contracts at market prices rather than betting against a house. But the characterization question is live (several commentators think sports event contracts especially look like wagers), so the framework belongs on this list, and the OBBBA math belongs in your risk assessment.

Pro Tip

Whichever treatment you choose, choose once and stay consistent. Reporting wins under capital treatment and losses under some other theory is the single fastest way to turn a gray area into an audit problem.

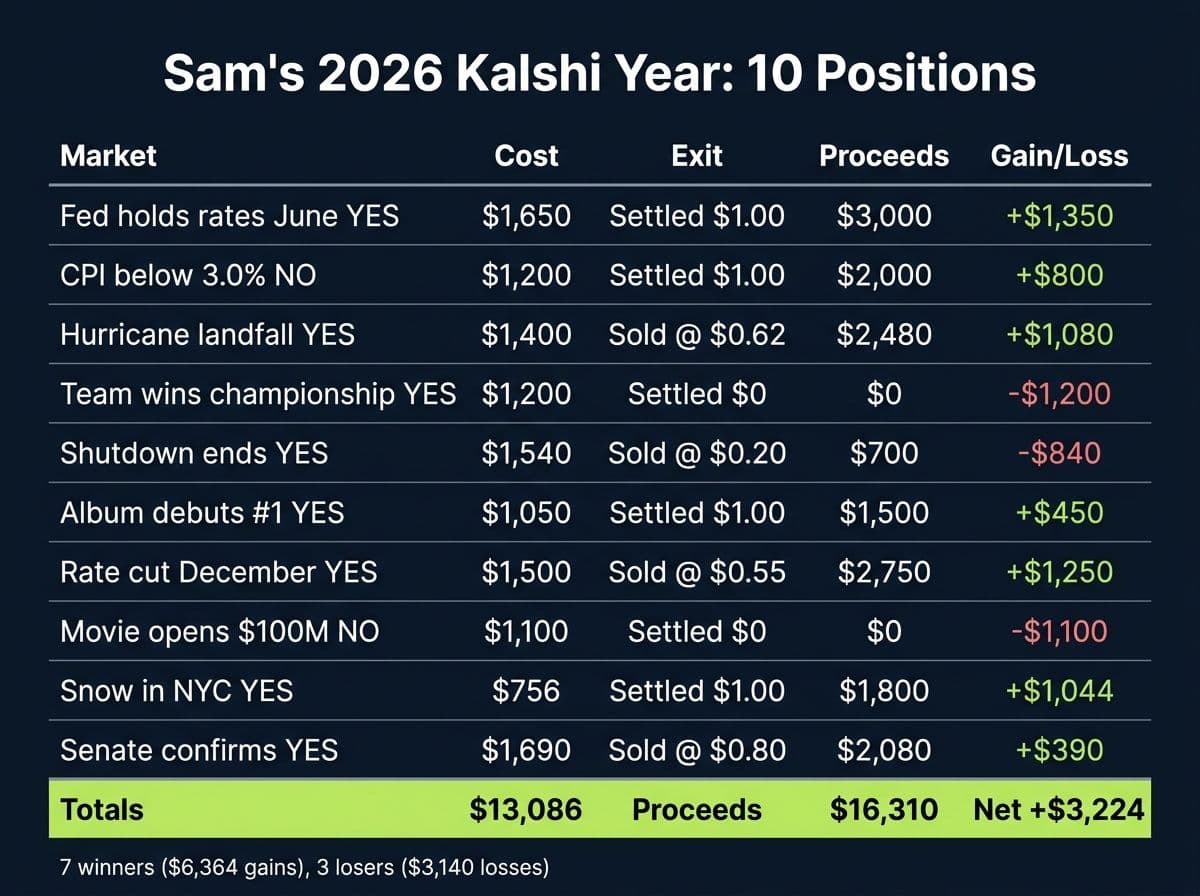

A Worked Example: Sam's Complete Kalshi Year

Theory tells you the options. Numbers tell you what they cost. Let's build a realistic Kalshi year and file it every possible way.

Meet Sam: single filer, $85,000 W-2 salary, 22% federal bracket. In 2026 Sam deposits $8,000 by bank transfer plus 0.02 BTC (bought years ago for $600, worth $2,000 on deposit day), trades 10 event contract positions, earns $142 of interest, and collects a $250 referral bonus.

Here's the trading year:

Sam's 2026 Kalshi Trade Log

| # | Market | Contracts | Cost | Exit | Proceeds | Gain/Loss |

|---|---|---|---|---|---|---|

| 1 | Fed holds rates in June: YES | 3,000 @ $0.55 | $1,650 | Settled $1.00 | $3,000 | +$1,350 |

| 2 | CPI below 3.0% in May: NO | 2,000 @ $0.60 | $1,200 | Settled $1.00 | $2,000 | +$800 |

| 3 | Hurricane landfall by Sept: YES | 4,000 @ $0.35 | $1,400 | Sold @ $0.62 | $2,480 | +$1,080 |

| 4 | Team wins championship: YES | 2,500 @ $0.48 | $1,200 | Settled $0 | $0 | -$1,200 |

| 5 | Shutdown ends by Oct 15: YES | 3,500 @ $0.44 | $1,540 | Sold @ $0.20 | $700 | -$840 |

| 6 | Album debuts #1: YES | 1,500 @ $0.70 | $1,050 | Settled $1.00 | $1,500 | +$450 |

| 7 | Rate cut in December: YES | 5,000 @ $0.30 | $1,500 | Sold @ $0.55 | $2,750 | +$1,250 |

| 8 | Movie opens above $100M: NO | 2,200 @ $0.50 | $1,100 | Settled $0 | $0 | -$1,100 |

| 9 | Snow in NYC by Dec 25: YES | 1,800 @ $0.42 | $756 | Settled $1.00 | $1,800 | +$1,044 |

| 10 | Senate confirms nominee: YES | 2,600 @ $0.65 | $1,690 | Sold @ $0.80 | $2,080 | +$390 |

| **Totals** | **$13,086** | **$16,310** | **+$3,224** |

Seven winners produced $6,364 of gains, three losers produced $3,140 of losses. Net trading profit: $3,224 (figures shown net of Kalshi's trading fees, which belong in your calculation).

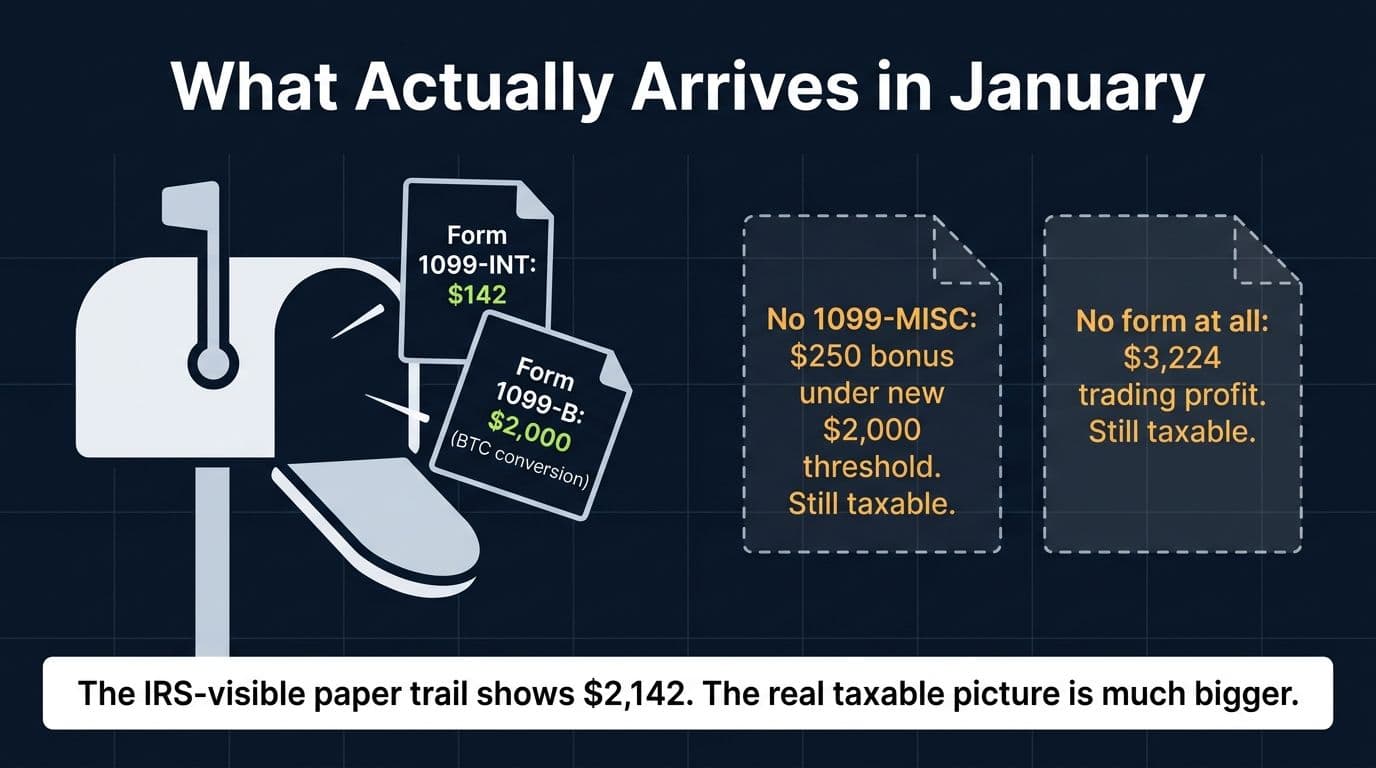

What Actually Arrives in January

Here's Sam's January tax mail, the part that surprises people:

- Form 1099-INT for $142. Arrives, and the IRS has a copy.

- Form 1099-B for $2,000. The BTC deposit. ZeroHash converted Sam's bitcoin to dollars on arrival, and that conversion is reportable proceeds. The IRS has a copy.

- No 1099-MISC. Sam's $250 bonus is under the new $2,000 threshold. Still taxable.

- Nothing for the $3,224 trading profit. The PnL statement sits in the Tax Info tab, unfiled and unofficial.

So the IRS-visible paper trail shows $2,142 of activity, while Sam's actual taxable picture adds $3,224 of trading profit plus a $1,400 capital gain hiding inside that BTC deposit (next section). A return that only reports what the forms show misses most of the income.

Sam's Return, Line by Line (Capital Asset Treatment)

Say Sam files under capital treatment:

- Form 8949, Part I, Box C (short-term, no 1099-B received): all 10 positions, one row each. Totals flow to Schedule D: $16,310 proceeds, $13,086 basis, $3,224 net short-term gain.

- Form 8949, Part II (long-term): the BTC deposit. Proceeds $2,000, basis $600, $1,400 long-term gain. This row reconciles the ZeroHash 1099-B.

- Interest line: the $142 of Kalshi interest.

- Schedule 1, Line 8z: the $250 referral bonus.

- Form 1040 digital asset question: Sam answers Yes (the BTC disposal makes this unambiguous).

Federal tax on the Kalshi activity: $3,224 x 22% = $709 on trading, $1,400 x 15% = $210 on the BTC gain, ($142 + $250) x 22% = $86 on interest and bonus. Total: about $1,005.

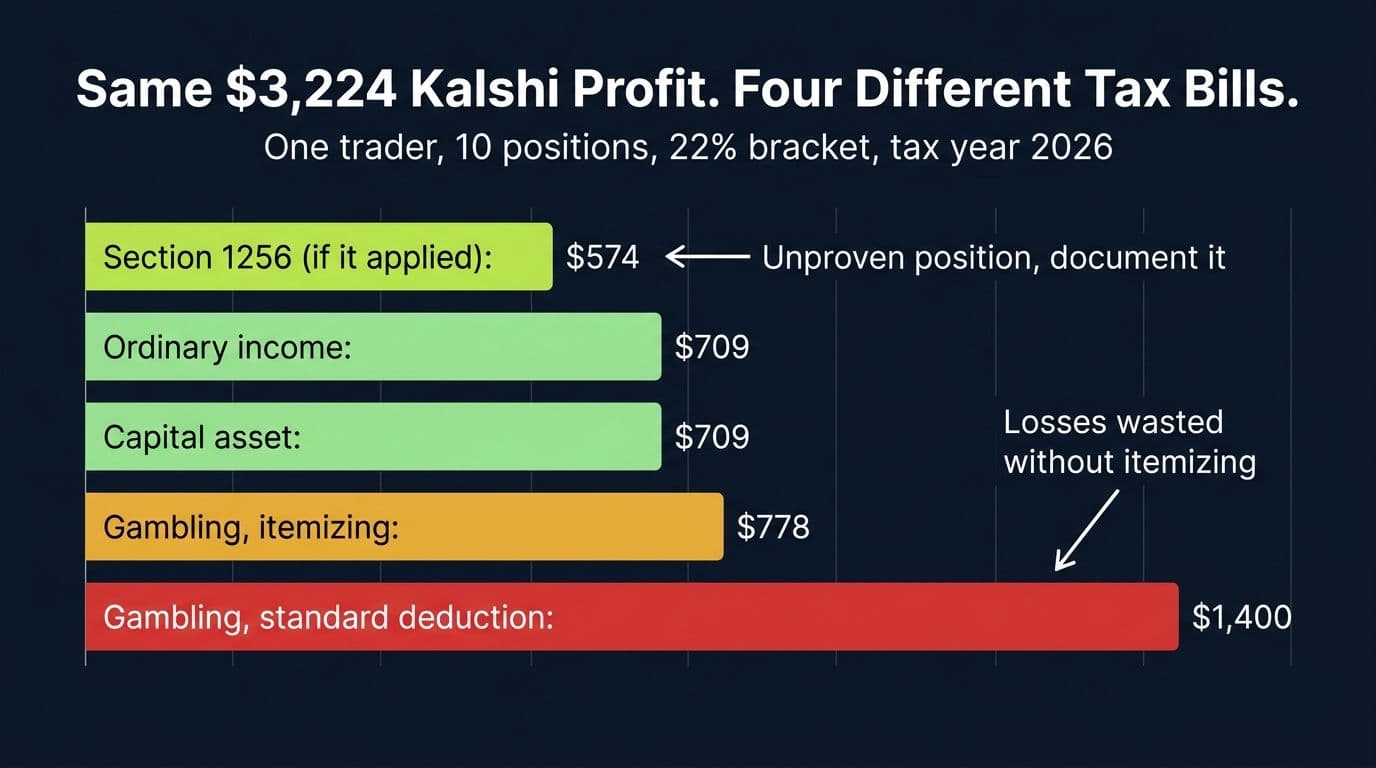

The Same Trading Year Under All Four Treatments

Now the comparison nobody on page one of Google runs. Same 10 trades, same $3,224 economic profit, four different bills on the trading activity alone (interest, bonus, and BTC gain stay constant):

Sam's Trading Tax Bill Under Each Treatment (2026, 22% Bracket)

| Treatment | What's Taxed | Federal Tax | Notes |

|---|---|---|---|

| Section 1256 (if it applied) | 60/40 split on $3,224 | $574 | $1,934 at 15% + $1,290 at 22%; unproven position, document it |

| Ordinary income | $3,224 net profit | $709 | Schedule 1, Line 8z; simplest paper trail |

| Capital asset | $3,224 net short-term gain | $709 | Form 8949 + Schedule D; best loss flexibility |

| Gambling, itemizing | $6,364 winnings less $2,826 (90% of $3,140 losses) | $778 | OBBBA cap adds $69 vs pre-2026 rules |

| Gambling, standard deduction | Full $6,364 winnings, losses wasted | $1,400 | Nearly double the default treatments |

Look at that spread. Identical trades, and the answer to one unresolved legal question moves Sam's bill from $574 to $1,400. Scale Sam's numbers by ten and the characterization question is worth more than most people's entire refund.

(Honest caveats: the gambling rows treat each position as its own wager because the IRS has never defined a "session" for exchange-traded contracts, and the 1256 row assumes the position survives scrutiny, which is genuinely uncertain.)

Want These Numbers Run on Your Actual Kalshi Year?

Garrett has filed prediction market returns under every treatment on this table. Bring your trade history and get a defensible answer, with the math shown.

Book a callThe Crypto Corner: Why Depositing Bitcoin Into Kalshi Is a Taxable Event

This is the least understood corner of Kalshi taxes, and it's going to generate IRS letters for years.

Kalshi lets you fund your account with crypto: BTC, USDC, SOL, and other supported assets. But Kalshi is a dollar-denominated exchange, so its partner ZeroHash converts your crypto to US dollars the moment it arrives. Your account is credited in dollars; the crypto is gone.

From the IRS's perspective, per its digital assets guidance, crypto is property, and converting property to dollars is a disposal. The deposit itself is the taxable event. Sam's 0.02 BTC, bought for $600 and converted at $2,000, produced a $1,400 long-term capital gain before Sam placed a single trade.

Three traps live inside this flow:

- The proceeds get reported; your basis doesn't. The ZeroHash 1099-B or 1099-DA shows what the conversion produced, but the platform has no idea what you originally paid for that bitcoin. If your return doesn't supply the basis, the IRS's default assumption is basis zero, meaning 100% gain. It's the same 1099-DA reconciliation problem hitting the whole crypto world in 2026.

- Stablecoins count too. Depositing USDC is also a disposal. The gain is usually pennies (USDC holds its peg), but the transaction belongs in your records, and it flips your Form 1040 digital asset answer to Yes.

- Withdrawing to crypto starts a new clock. Cash out of Kalshi into crypto and the conversion price becomes your new cost basis with a new holding period. Track it from day one.

If most of your prediction market activity lives on crypto rails instead, the picture inverts entirely: no forms at all, plus a stablecoin layer on every trade. That's a different article, and we wrote it: Polymarket taxes.

Pro Tip

Deposit crypto into Kalshi only after checking what gain you're about to realize. We've seen traders trigger five-figure capital gains funding an account, without realizing a sale happened, because the word "deposit" sounds harmless.

How to Report Kalshi on Your Taxes: Step by Step

Here's the workflow we use when a Kalshi year lands on our desk. Steal it.

Step 1: Export everything. Download your full trade history and PnL statement from the Tax Info page. Now, not in April; you want time to fix anomalies.

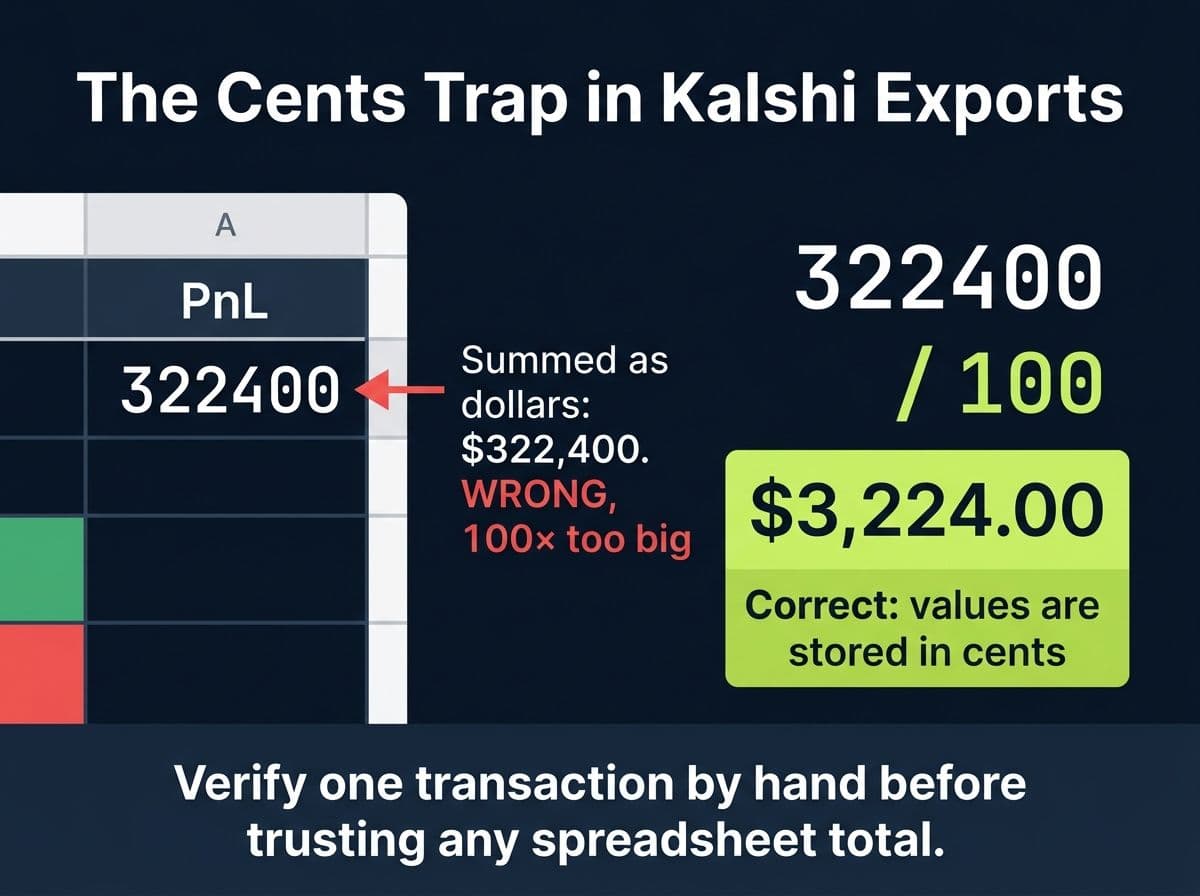

Step 2: Mind the cents. Kalshi's transaction export stores monetary values in cents, not dollars. A PnL entry of 322400 means $3,224.00. Sum the raw column without dividing by 100 and your profit comes out exactly one hundred times too large. Verify one transaction by hand before trusting any spreadsheet total; a surprising number of self-prepared Kalshi tax returns fail this check.

Step 3: Compute net profit independently. Total proceeds minus total cost minus fees, across every position closed during the year. Reconcile against the PnL statement (remember it uses FIFO). If they disagree, find out why before filing.

Step 4: Pick your treatment and place the income. Ordinary income goes on Schedule 1, Line 8z. Capital treatment goes position-by-position on Form 8949, Box C, flowing to Schedule D. A documented 1256 position goes on Form 6781. Whatever you choose, write down why and keep it with your records.

Step 5: Add the side income. Interest from the 1099-INT. Bonuses and credits, form or no form. Any crypto conversion gains, with basis you can prove.

Step 6: Check the estimated tax math. No withholding means a big Kalshi year can trigger underpayment penalties even if you pay in full by April. If you're up meaningfully by mid-year, make quarterly payments.

Step 7: Keep the file. Trade history, PnL statements, bank and crypto records, your treatment memo. Seven years.

Pro Tip

Set a calendar reminder for the first week of January: download your prior-year trade history and PnL statement while the year is fresh. Platform exports change format, support queues get long in March, and the trader with clean records in January files a better return than the one reconstructing in April.

Kalshi vs Polymarket vs Robinhood: The Tax Difference in One Paragraph

Traders increasingly use all three. Kalshi settles in dollars and gives you partial forms plus a PnL statement; you self-report the trading profit. Robinhood's event contracts (which execute on Kalshi's exchange) settle in dollars with no 1099 for the contracts at all; the annual statement explicitly isn't a tax form. Polymarket settles in USDC on the Polygon blockchain, sends nothing, and layers crypto property taxation onto every trade. Same product, three different tax seasons. Our pillar guide linked above compares all eleven major platforms side by side.

State Taxes on Kalshi Winnings

Federal isn't the whole bill. Three state-level points on Kalshi taxes worth knowing:

Your state taxes the income too. If you live in a state with an income tax, your Kalshi profit is taxable there under whatever character it takes federally. California, New York, New Jersey: plan on your marginal state rate on top of the federal numbers above. The no-income-tax states spare you this layer.

Characterization can matter more at the state level. Some states tax gambling winnings gross while limiting or denying loss deductions entirely. If gambling treatment ever sticks to event contracts, a break-even year could produce a real state bill in those states. One more reason most filers document a non-gambling position.

The regulatory fight isn't a tax fight. Kalshi operates nationwide under CFTC jurisdiction and has spent two years litigating with state gaming regulators over its sports contracts. Interesting law, irrelevant to your return: whether a state regulator thinks Kalshi should operate there has no bearing on whether your profits are taxable. They are.

Common Kalshi Tax Mistakes We See

After enough prediction market returns, the same errors repeat:

- Reporting only what came on a form. The 1099-INT gets reported, the $9,000 trading profit doesn't. The signature Kalshi tax mistake.

- The cents-to-dollars error. Raw export values summed without dividing by 100.

- Not realizing a crypto deposit was a sale. Five-figure BTC deposits with unreported gains, discovered when the ZeroHash form surfaces basis questions.

- Claiming 60/40 rates with zero documentation. Section 1256 without a memo, a consistent method, or Form 6781 mechanics done right, including year-end marks.

- Netting the bonus into trading P&L. Rewards income double-counted or vanished, so nothing ties to the 1099-MISC when one exists.

- Ignoring estimated taxes. A $40,000 profit year, zero withholding, and an April surprise with an underpayment penalty attached.

Every one is preventable with the workflow above. If you've already received an IRS notice about a past year, move quickly and deliberately: our guide to responding to IRS crypto tax notices applies to prediction market mismatches too.

When to DIY and When to Bring In a Pro

Straight talk:

Handling Kalshi taxes yourself is fine if: you made a modest profit across a manageable number of trades, you're comfortable with ordinary income or capital treatment, you never deposited crypto, and your records reconcile cleanly.

Get professional help if: you're up five figures or more, you're weighing a Section 1256 position, you funded with crypto and don't know your basis, you trade multiple platforms (especially crypto-settled ones), you have unreported prior years, or a notice already arrived. Here's what a crypto-specialized CPA costs and how to vet one.

The economics are usually simple. On a big year, the characterization question alone (remember Sam's $574 to $1,400 spread, then add zeros) is worth more than the fee, and a documented position beats an improvised one in every audit we've ever handled.

Get Your Kalshi Year Filed Right

Flat-fee preparation for prediction market traders: trade history reconciled, treatment documented, crypto deposits handled, return signed by a CPA who has done this before.

Book a callFAQ: Kalshi Taxes

Frequently Asked Questions

Do you have to pay taxes on Kalshi winnings?

Yes. All Kalshi profits are taxable from the first dollar, whether or not you receive a tax form and whether or not you withdraw to your bank. Kalshi withholds nothing, so the full reporting and payment obligation sits with you.

Does Kalshi send you a 1099?

Only narrow ones. Kalshi issues a 1099-INT for interest of $10 or more, a 1099-MISC for credits and rewards above the threshold ($600 for 2025, $2,000 for 2026), and 1099-B or 1099-DA forms for crypto conversions through ZeroHash. No 1099 covers your event contract trading profits.

Does Kalshi report to the IRS?

Partially. Every 1099 Kalshi issues also goes to the IRS, so interest, larger rewards, and crypto conversion proceeds are visible. Contract-level trading activity is not reported, but you must report it yourself, and Kalshi keeps complete KYC'd records the IRS can request.

What tax form do I use to report Kalshi trading?

It depends on your treatment. Most filers report net profit as Other Income on Schedule 1, Line 8z, or list positions on Form 8949 and Schedule D under capital treatment. A documented Section 1256 position uses Form 6781. Interest goes on your interest line, rewards on Schedule 1.

Do I have to report Kalshi if I made less than $600?

Yes. The $600 figure (now $2,000 for 2026) is a form-issuance threshold for the 1099-MISC, not a tax exemption. All trading profit is taxable from the first dollar regardless of whether any form is generated.

How do I find my Kalshi tax documents?

Open the Account tab and go to the Tax Info page. Any 1099s you qualified for appear there, along with your Profit and Loss statement. Download your full trade history too, and remember the export stores values in cents, not dollars.

Is Kalshi trading treated as gambling for taxes?

Not by default. The IRS has issued no guidance, and most practitioners treat exchange-traded event contracts under ordinary income or capital asset principles rather than gambling rules. The distinction matters more from 2026, when the One Big Beautiful Bill Act caps gambling loss deductions at 90% of losses.

Can you write off Kalshi losses?

Generally yes, depending on treatment. Under ordinary income treatment, losses net against gains from the activity. Under capital treatment, losses offset any capital gains plus up to $3,000 of ordinary income per year with carryforward. Under gambling treatment, losses help only if you itemize and are capped at 90% from 2026.

Do Kalshi contracts qualify for Section 1256 60/40 treatment?

It's unresolved. Kalshi's status as a CFTC-regulated exchange makes the argument stronger than for any other prediction market, but the Dodd-Frank swap exclusion may disqualify event contracts, and the IRS has never ruled. If you take the position, document the analysis, apply mark-to-market correctly, and consider a Form 8275 disclosure.

Is depositing crypto into Kalshi taxable?

Yes. ZeroHash converts your crypto to dollars the moment it arrives, and that conversion is a disposal of property. You recognize gain or loss equal to the conversion value minus your original cost basis, and the proceeds are reported on a 1099-B or 1099-DA. The same logic applies to stablecoins, just with tiny gains.

Do I pay taxes on Kalshi interest?

Yes. Interest from Kalshi's APY program is ordinary interest income, exactly like a savings account. Kalshi issues a 1099-INT at $10 or more and files it with the IRS, so this is the one Kalshi number the IRS always has. Report it separately from your trading profit.

Does Kalshi withhold taxes on winnings?

No. Kalshi withholds nothing from trading profits, interest, or bonuses. In a significantly profitable year, plan on quarterly estimated tax payments to avoid an underpayment penalty.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Prediction Market Taxes (2026): How Kalshi, Polymarket, Robinhood and Every Major Platform Gets Taxed

How prediction market taxes work on Kalshi, Polymarket, Robinhood and more. A CPA splits platforms by settlement type and shows exactly what to report.

Polymarket Taxes (2026): A CPA's Guide to Reporting When There's No 1099

Polymarket sends no 1099, but your winnings are still taxable. A CPA explains the forms, the four tax treatments, and the USDC layer, with worked numbers.

The Ultimate Guide to Crypto Tax (2026 Edition)

The most comprehensive crypto tax guide online, written by a CPA who files 500+ crypto returns a year. Every taxable event, form, strategy, and 2026 update.