Polymarket Taxes (2026): A CPA's Guide to Reporting When There's No 1099

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Polymarket issues no Form 1099-B, 1099-DA, or W-2G. You are still legally required to report every gain and loss to the IRS.

- ✓Polymarket settles in USDC on Polygon, so each trade creates two tax layers: the event contract and the stablecoin used to buy and receive it.

- ✓The IRS has issued no guidance on prediction markets. Filers choose between capital asset, ordinary income, gambling, and Section 1256 treatment, and the choice can move the bill by thousands.

- ✓From 2026, the One Big Beautiful Bill Act caps gambling loss deductions at 90%, creating phantom income under gambling treatment.

- ✓USDC withdrawals surface on exchange 1099-DA forms with missing cost basis. Unreconciled proceeds are what trigger IRS mismatch notices.

Pro Tip

Written by Garrett Taylor, CPA (License #133092). Reviewed by Leanne Grant, EA (#00167954-EA). Last updated: July 2, 2026.

Quick answer: Yes, Polymarket winnings are taxable, even though Polymarket sends you no 1099. Every settlement and every early sale is a taxable event, and because payouts arrive in USDC, you also have a crypto tax layer on top. The IRS has not said which framework applies, so most filers choose between capital gains (Form 8949) and ordinary income (Schedule 1). This guide walks through both, with real numbers.

You made money on Polymarket. Maybe you called the election, the Fed meeting, or the Oscars.

Then January came and went, and no tax form showed up.

Here's the deal: that missing 1099 does not make your winnings tax-free. It makes them your problem. We prepare returns for prediction market traders every season, and Polymarket taxes are some of the most misunderstood filings we see. The platform sends nothing, the IRS has published nothing specific, and the internet is full of confident answers that contradict each other.

In this guide, we'll show you exactly how to report Polymarket activity: which forms to use, how the USDC layer works, what the four possible tax treatments are, and what one real-looking trading year actually looks like on a return. All with worked numbers you can check.

Let's dig in.

Do You Pay Taxes on Polymarket? (Short Answer: Yes)

Under US law, all income is taxable unless Congress specifically exempts it. That rule comes from Section 61 of the Internal Revenue Code, and there is no exemption for prediction markets.

So when you buy a Yes share for $0.62 and it settles at $1.00, you have income. When you sell a position early for more than you paid, you have income. When a position settles at zero, you have a loss (and yes, losses matter, more on that below).

In other words, taxes on Polymarket work like taxes on any other trading activity: profit is income. It does not matter that:

- Polymarket never sent you a form

- You never converted your USDC back to dollars

- Your winnings stayed inside the platform all year

- You live in a state with no income tax (that only helps at the state level)

The taxable event happens when the position is disposed of, not when you cash out to your bank. That single misunderstanding causes more Polymarket tax problems than anything else.

Now let me show you why Polymarket taxes are trickier than a normal brokerage account's.

How Polymarket Positions Actually Work (the 60-Second Version)

You need this background because the mechanics drive the taxes.

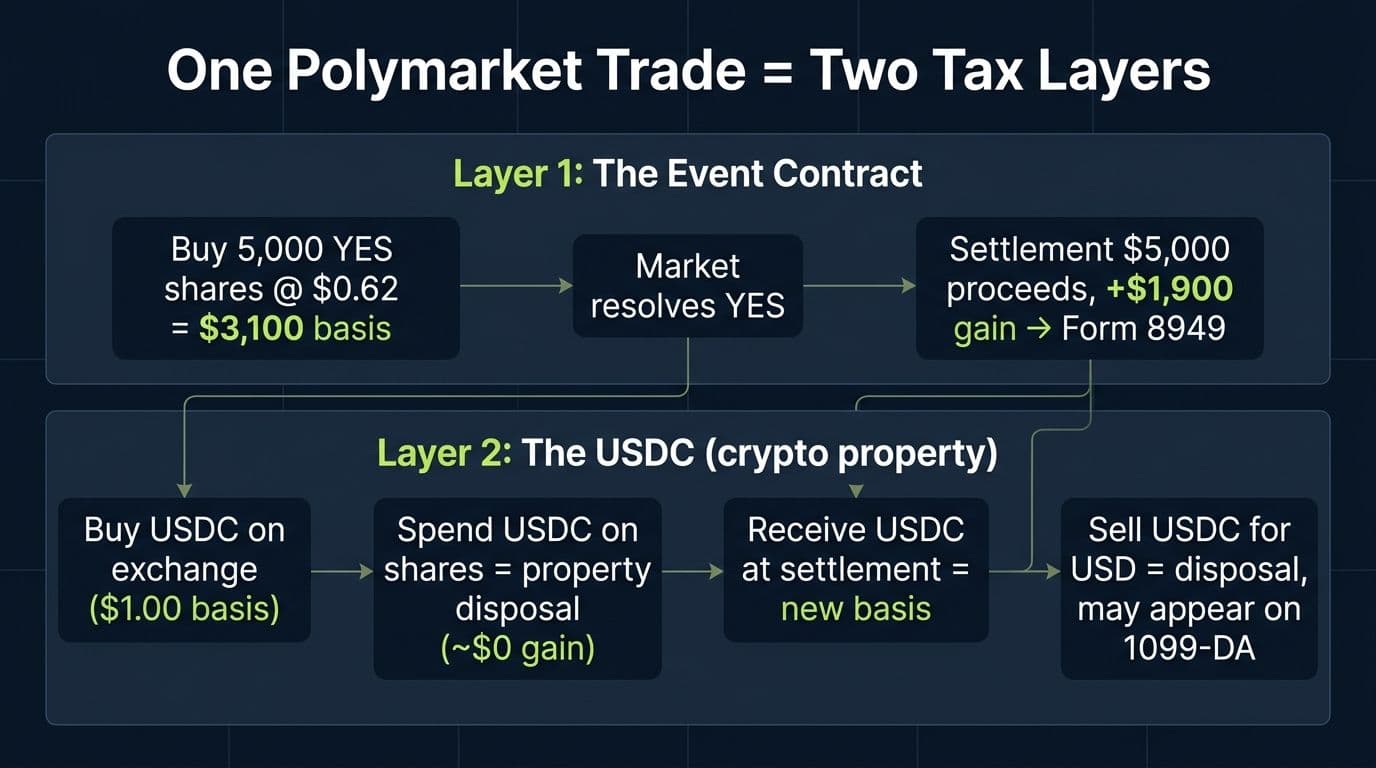

Polymarket runs on the Polygon blockchain. Every market is a binary question: will this event happen, yes or no? You buy outcome shares (technically ERC-1155 tokens) priced between $0.01 and $0.99. If your side wins, each share redeems for exactly $1.00. If it loses, it redeems for $0.

Everything is denominated in USDC, a dollar-pegged stablecoin. You fund your account with USDC, you buy shares with USDC, and winning positions pay out in USDC.

Here's the kicker: the IRS treats USDC as property, not cash. The IRS says so plainly on its digital assets page: digital assets are treated as property, and general property tax principles apply. A dollar-pegged token is still a digital asset.

That means every Polymarket trade touches two separate tax layers:

- The event contract layer. You bought a contractual right for consideration and disposed of it through sale or settlement. Gain or loss equals proceeds minus cost basis.

- The USDC layer. Spending USDC to buy shares is a disposal of property. Receiving USDC at settlement is an acquisition of property with a new cost basis. Selling USDC for dollars later is another disposal.

The USDC layer usually produces gains and losses of nearly zero (the peg holds at $1.00), but the transactions still exist, they still belong in your records, and they still connect to the Form 1040 digital asset question. Every US filer now answers, under penalty of perjury, whether they received, sold, or disposed of digital assets during the year.

If you traded on Polymarket, your answer is yes. Check the box.

Pro Tip

Since January 1, 2025, the IRS also requires per-wallet cost basis tracking for digital assets under Rev. Proc. 2024-28. Your Polymarket wallet's USDC needs its own basis records, separate from your Coinbase or MetaMask balances. See our full guide to [crypto cost basis methods](/blog/crypto-cost-basis-methods).

Why Polymarket Doesn't Send a 1099 (and Why the IRS Doesn't Care)

Polymarket issues no Form 1099-B, no Form 1099-DA, and no Form W-2G. Nothing arrives in January. Nothing gets filed with the IRS on your behalf.

Why not? A little history helps, because Polymarket's regulatory status changed dramatically while most guides weren't looking.

- January 2022: Polymarket paid a $1.4 million civil penalty to settle CFTC charges that it operated an unregistered market for event-based binary options. It agreed to block US users.

- 2022 to 2025: Polymarket operated offshore. US users who accessed it anyway traded on a platform with no US reporting obligations at all.

- July 2025: Polymarket acquired QCEX, a CFTC-licensed exchange and clearinghouse, for $112 million.

- November 25, 2025: The CFTC issued an amended Order of Designation. Polymarket US became a regulated Designated Contract Market (DCM).

- January 2026: Polymarket relaunched to US users under the new structure.

So Polymarket is now regulated. But as of mid-2026, it still has not committed to issuing 1099s for event contract trades, and the IRS broker reporting rules for Form 1099-DA were written around custodial intermediaries, which doesn't map cleanly onto a platform where positions live in smart contracts.

The practical upshot never changes: the entire reporting burden sits with you. No form to reconcile against. No basis number from a broker. No pre-made characterization of the income.

But here's what traders get wrong. No 1099 does not mean no visibility.

Every Polymarket transaction is permanently recorded on the Polygon blockchain, in public. The IRS uses blockchain analytics tools, and your wallet connects to your identity the moment you move USDC through a KYC exchange like Coinbase or Kraken. We'll show you exactly how that surfaces on a 1099-DA later in this guide, because it's the mechanism most likely to generate IRS letters for Polymarket traders in 2026 and beyond.

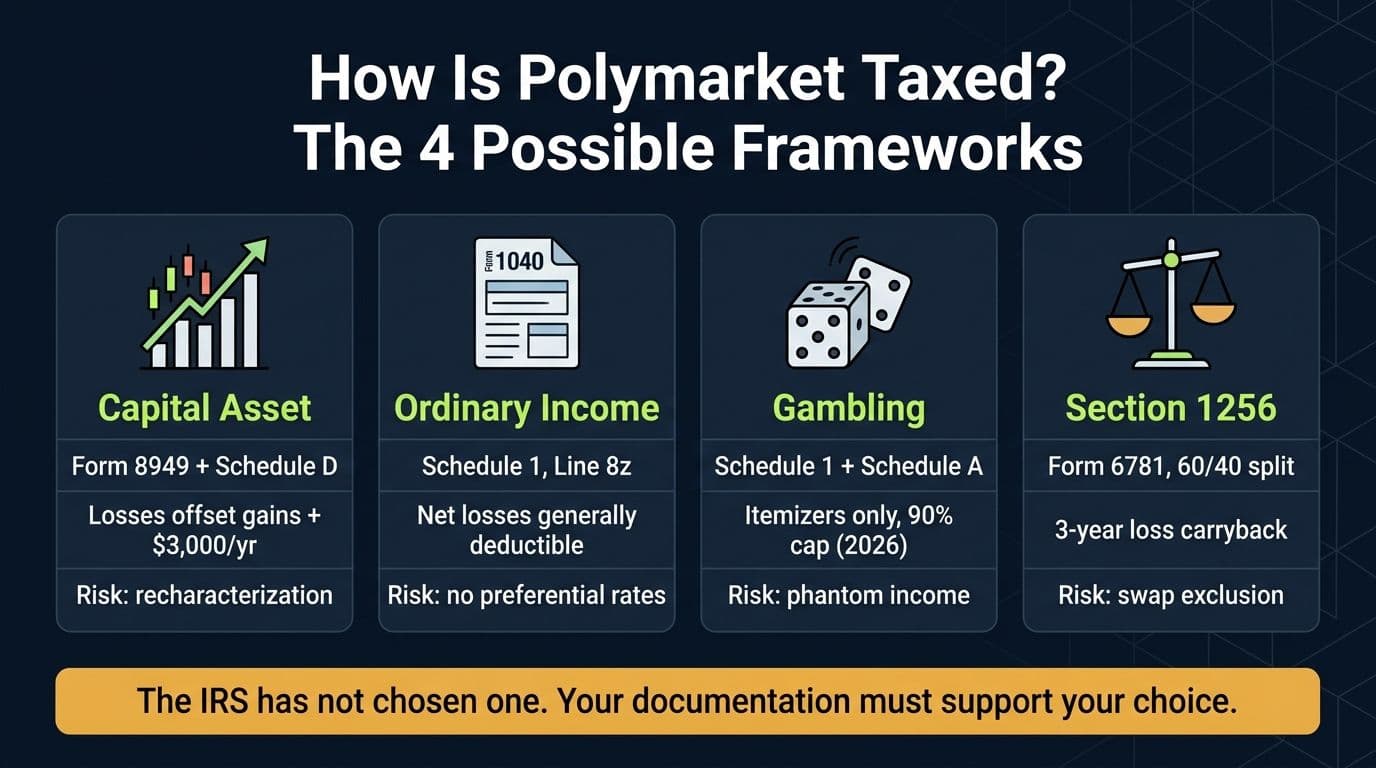

How Are Polymarket Taxes Calculated? The Four Frameworks

Now for the question everyone actually asks: what rate do you pay?

Honest answer from a working CPA: the IRS has never issued guidance on prediction market contracts. No revenue ruling, no notice, no FAQ. Thomson Reuters put it bluntly in a June 2026 report on IRS silence around prediction market winnings, where Baker Tilly's James Creech predicted the classification fight is "probably headed to the Supreme Court."

Until that's resolved, practitioners analyze Polymarket activity under four existing frameworks. Each one is a defensible reading of current law. Each one produces a different form and, sometimes, a very different bill.

The Four Possible Tax Treatments of Polymarket Activity

| Framework | Where It's Reported | Loss Treatment | Biggest Risk |

|---|---|---|---|

| Capital asset | Form 8949 + Schedule D | Offset gains fully; $3,000/yr against ordinary income; carry forward | IRS recharacterization as ordinary income |

| Ordinary income | Schedule 1, Line 8z | Net losses generally deductible without gambling limits | No preferential rates, weaker loss guidance |

| Gambling | Schedule 1 (winnings) + Schedule A (losses) | Itemizers only; capped at 90% of losses from 2026 | Phantom income, session-rule complexity |

| Section 1256 | Form 6781 | 60/40 split; 3-year carryback of net losses | Swap exclusion may disqualify event contracts |

Framework 1: Capital Asset (the Most Common Choice)

Under this view, a Polymarket share is a transferable contractual right, which is property. You bought it for consideration, you disposed of it by sale or settlement, and Section 1001 says you recognize gain or loss equal to proceeds minus basis. Character flows from Section 1221's capital asset definition.

Each position goes on Form 8949 and flows to Schedule D. Positions held a year or less (nearly all of them, since markets resolve fast) are short-term and taxed at your ordinary rate. Positions held longer than a year get long-term rates of 0%, 15%, or 20%.

The real advantage isn't the rate. It's the losses. Capital losses offset capital gains dollar for dollar, including gains from your stock portfolio or crypto. Excess losses deduct up to $3,000 per year against ordinary income and carry forward indefinitely.

The risk: the IRS could argue these contracts aren't capital assets in your hands, especially if your activity pattern looks like wagering rather than investing.

Framework 2: Ordinary Income (the Conservative Default)

Under this view, prediction market contracts are contingent-payoff instruments that don't fit the capital asset box. You report your net profit as Other Income on Schedule 1, Line 8z, with a label like "Polymarket prediction market income."

Important distinction that trips up even preparers: ordinary income treatment is not gambling treatment. Under this framework, gains and losses net fully, and losses aren't trapped behind itemized deduction limits. It's the simplest defensible position, and for short-term traders the rate is often identical to capital treatment anyway, since short-term capital gains are taxed at ordinary rates.

Framework 3: Gambling (the One That Just Got Expensive)

If Polymarket activity is wagering, Section 165(d) controls. Winnings are ordinary income. Losses are deductible only if you itemize, and only against winnings. For context, a March 2026 Ipsos poll found 61% of Americans consider prediction market trading closer to gambling than investing, so don't dismiss this framework as far-fetched.

And here's where 2026 changed the math. The One Big Beautiful Bill Act, signed July 4, 2025, caps the gambling loss deduction at 90% of losses for tax years starting in 2026.

Watch what that does:

A high-volume trader wins $500,000 and loses $500,000 in the same year. Economically: dead flat, zero profit.

Under gambling treatment for 2026:

- Winnings reported: $500,000

- Losses deductible: $450,000 (90% cap)

- Taxable phantom income: $50,000

- Federal tax at a 37% marginal rate: roughly $18,500 on money that was never earned

Add the unresolved "session" problem (the IRS has never defined what a gambling session means for a 24/7 on-chain market) and you can see why most practitioners reserve gambling treatment for fact patterns that genuinely look like betting sprees.

Pro Tip

Several states are worse. Some tax gambling winnings gross while allowing no loss deduction at all. A trader with $60,000 of wins and $55,000 of losses could owe state tax on the full $60,000. If gambling characterization applies to you, check your state's rules before you file, not after.

Framework 4: Section 1256 (Tempting, Unproven)

Section 1256 gives regulated futures contracts a gift: 60% of gains taxed as long-term and 40% as short-term regardless of holding period, mark-to-market at year end, reported on Form 6781. Net 1256 losses can even be carried back three years against prior 1256 gains.

The argument for: since November 2025, Polymarket US is a CFTC-regulated Designated Contract Market, and Section 1256 covers regulated futures contracts traded on qualified exchanges.

The argument against: the CFTC has classified event contracts as binary options that are swaps, and Section 1256(b)(2)(B), added by Dodd-Frank, excludes most swaps from 60/40 treatment. KPMG's analysis of CFTC event contracts lands where we do: the classification is genuinely unresolved, and it drives materially different outcomes.

Our position: Section 1256 is an analytical question, not a default. If you take it, take it with professional support and consider filing a disclosure statement (Form 8275). Do not adopt it just because the 60/40 math looks nice. And note it can only plausibly apply to trades on the regulated US platform, not to pre-2026 offshore activity.

“Pick the framework your facts support, document why, and apply it consistently. The traders who get hurt aren't the ones who chose capital treatment over ordinary income. They're the ones who chose nothing and reported nothing.”

, Garrett Taylor, CPA

A Worked Example: One Trader's Full Polymarket Year

Theory is nice. Numbers are better. Let's build a complete, realistic year and put it on a return.

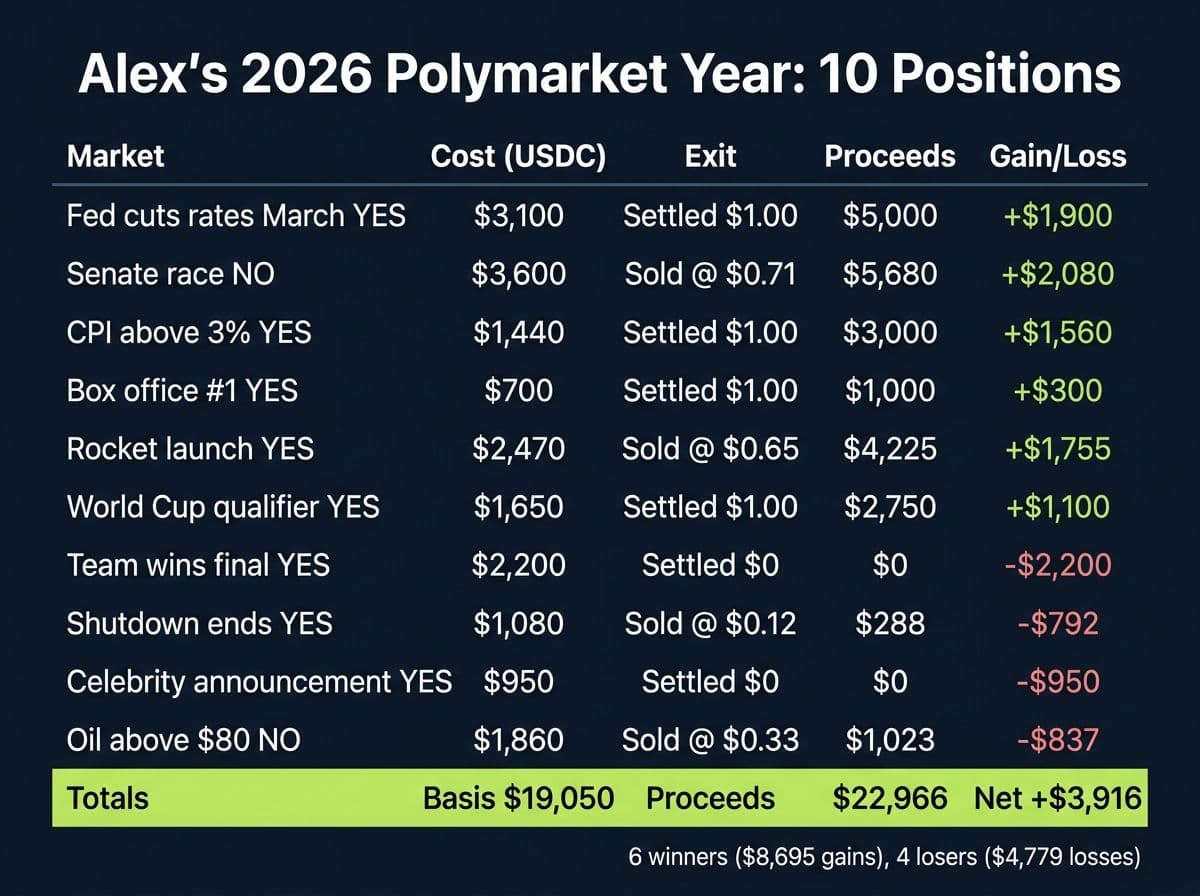

Meet Alex. W-2 income of $120,000 (24% federal bracket, single filer). In 2026, Alex funds Polymarket with $20,000 of USDC bought on Coinbase at $1.00 and bridged to Polygon. Alex trades 10 positions during the year:

Alex's 2026 Polymarket Trade Log

| # | Market | Shares | Cost (USDC) | Exit | Proceeds | Gain/Loss |

|---|---|---|---|---|---|---|

| 1 | Fed cuts rates in March: YES | 5,000 @ $0.62 | $3,100 | Settled $1.00 | $5,000 | +$1,900 |

| 2 | Senate race: NO | 8,000 @ $0.45 | $3,600 | Sold @ $0.71 | $5,680 | +$2,080 |

| 3 | CPI above 3%: YES | 3,000 @ $0.48 | $1,440 | Settled $1.00 | $3,000 | +$1,560 |

| 4 | Box office #1 opening: YES | 1,000 @ $0.70 | $700 | Settled $1.00 | $1,000 | +$300 |

| 5 | Rocket launch by June: YES | 6,500 @ $0.38 | $2,470 | Sold @ $0.65 | $4,225 | +$1,755 |

| 6 | World Cup qualifier: YES | 2,750 @ $0.60 | $1,650 | Settled $1.00 | $2,750 | +$1,100 |

| 7 | Team wins final: YES | 4,000 @ $0.55 | $2,200 | Settled $0 | $0 | -$2,200 |

| 8 | Shutdown ends by Friday: YES | 2,400 @ $0.45 | $1,080 | Sold @ $0.12 | $288 | -$792 |

| 9 | Celebrity announcement: YES | 2,500 @ $0.38 | $950 | Settled $0 | $0 | -$950 |

| 10 | Oil above $80: NO | 3,100 @ $0.60 | $1,860 | Sold @ $0.33 | $1,023 | -$837 |

| **Totals** | **$19,050** | **$22,966** | **+$3,916** |

Six winners produced $8,695 of gains. Four losers produced $4,779 of losses. Net result: a $3,916 profit on $19,050 deployed.

What Goes on the Forms (Capital Asset Treatment)

Alex files under the capital asset framework, the most common choice we see. Here's the paper trail:

- Form 8949, Part I (short-term, Box C since no 1099-B was received). All 10 positions, one row each: description ("Polymarket YES shares, Fed March rate cut market"), date acquired, date sold or settled, proceeds, cost basis, gain or loss.

- Schedule D. Short-term totals flow in: $22,966 proceeds, $19,050 basis, $3,916 net short-term capital gain.

- Form 1040. The $3,916 lands in income. Alex checks Yes on the digital asset question.

- The USDC layer. Alex's USDC disposals (spending it on shares at $1.00 basis, receiving it at settlement) produce roughly zero gain, but they're in the records and support the 8949 numbers.

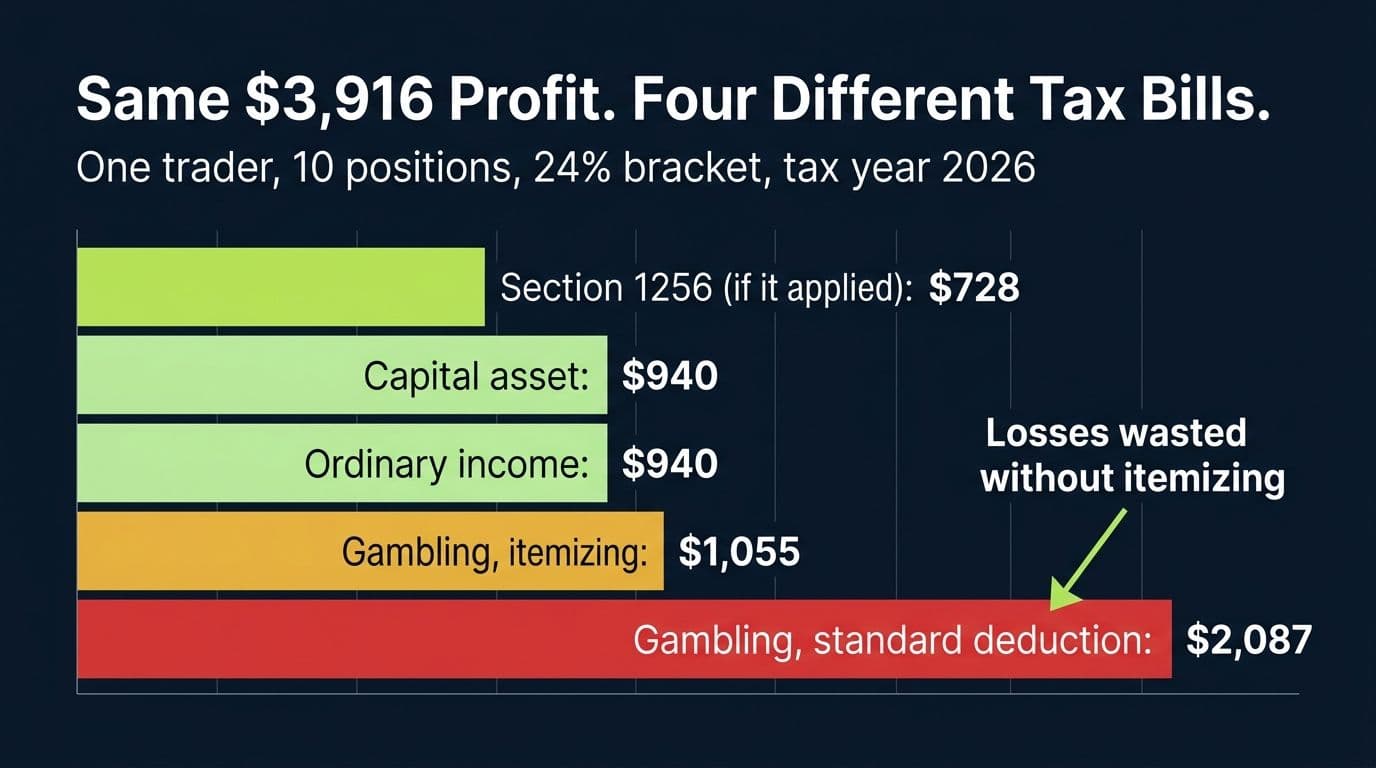

Alex's federal tax on the Polymarket activity: $3,916 x 24% = $940. Every position was held under a year, so short-term rates apply.

The Same Year Under All Four Frameworks

Now the part nobody on page one of Google shows you. Same trades, same $3,916 economic profit, four different tax bills:

Alex's Tax Bill Under Each Framework (2026, 24% Bracket)

| Framework | What's Taxed | Federal Tax | Notes |

|---|---|---|---|

| Capital asset | $3,916 net short-term gain | $940 | Form 8949 + Schedule D |

| Ordinary income | $3,916 net profit | $940 | Schedule 1, Line 8z; simplest paper trail |

| Section 1256 (if it applied) | 60/40 split on $3,916 | $728 | $2,350 at 15% + $1,566 at 24%; unproven position |

| Gambling, itemizing | $8,695 winnings less $4,301 (90% of $4,779 losses) = $4,394 | $1,055 | OBBBA cap costs $115 vs pre-2026 rules |

| Gambling, standard deduction | Full $8,695 winnings, losses wasted | $2,087 | More than double the capital-asset bill |

Look at that spread. The framework question alone moves Alex's bill from $728 to $2,087 on identical trades. That's why "how is Polymarket taxed" has no one-sentence answer, and why the characterization debate is worth real money to active traders.

(One honest caveat: the gambling rows simplify the IRS "session" concept by treating positions individually. Nobody knows how sessions work for on-chain markets, which is itself a reason that framework is operationally painful.)

Not Sure Which Framework Fits Your Facts?

Garrett has filed prediction market returns under every one of these treatments. Get a straight answer about yours before the IRS asks first.

Book a callCan You Write Off Polymarket Losses?

Had a losing year? You have options, and they depend entirely on the framework:

- Capital asset: losses offset any capital gains (stocks, crypto, other Polymarket wins), then up to $3,000 per year against ordinary income, with unlimited carryforward. A $10,000 net Polymarket loss can shelter $10,000 of stock gains this year.

- Ordinary income: net losses from the activity are generally deductible against ordinary income without the gambling limitations, though this corner of the law is the least developed. Document your position.

- Gambling: losses deduct only if you itemize, only against winnings, and only up to 90% of losses starting in 2026. If you take the standard deduction, your losses do nothing.

- Section 1256: net losses can be carried back three years against prior Section 1256 gains, a benefit no other framework offers.

One more thing, since traders always ask: the wash sale rule (Section 1091) applies to securities, and prediction market contracts are not securities. Selling a losing position and immediately re-entering the same market generally doesn't trigger wash sale treatment under current law. The same logic that keeps crypto outside the wash sale rules applies here, and the same warning too: Congress keeps proposing to change it.

Pro Tip

Losses only exist on paper if you can prove basis. A position that settled at zero is a real, documented loss ONLY if you can show what you paid for it. This is where traders who kept no records lose twice.

The 1099-DA Era: Why 2026 Is the Year Polymarket Traders Get Noticed

This section matters more than any other in this guide. Here's why.

Starting with transactions on January 1, 2025, custodial brokers like Coinbase and Kraken must report digital asset gross proceeds to the IRS on Form 1099-DA. The first wave of those forms landed in early 2026. Cost basis reporting phases in for assets acquired in custodial accounts from 2026 onward.

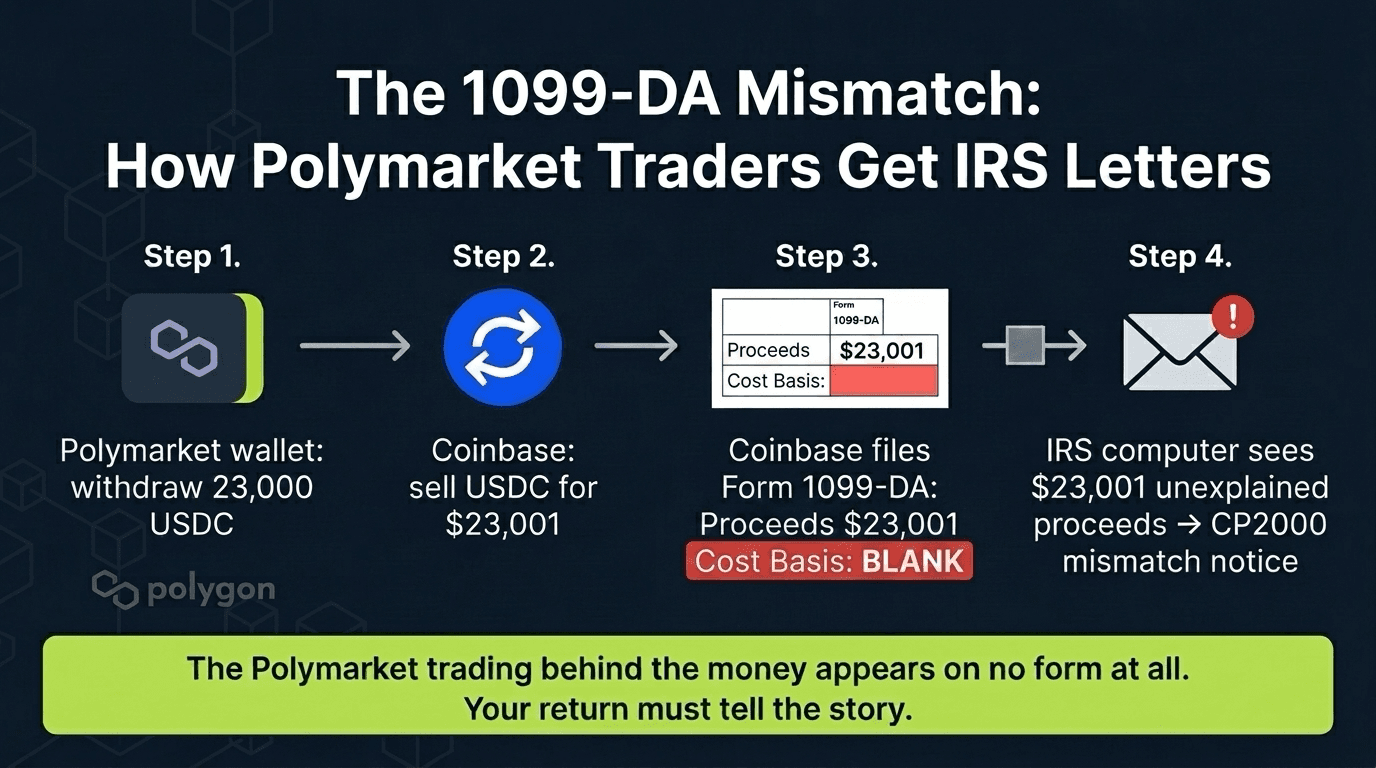

Now trace Alex's money:

- Alex withdraws 23,000 USDC from Polymarket back to Coinbase.

- Alex sells the USDC for $23,001.

- Coinbase files a 1099-DA showing $23,001 of gross proceeds to the IRS.

- Because that USDC was transferred in from an outside wallet, Coinbase doesn't know its basis. The basis field is blank or zero.

From the IRS computer's perspective, Alex has up to $23,001 of unexplained digital asset proceeds. The Polymarket trading that actually produced the money appears on no form anywhere. If Alex's return doesn't report the USDC disposal with correct basis and the underlying trading income, that mismatch is exactly the pattern that generates automated CP2000 notices.

The absence of a Polymarket 1099 doesn't hide you. Combined with exchange 1099-DAs, it exposes you. The IRS sees the cash-out side without the story behind it, and taxpayers with unexplained proceeds get letters.

If you've already received one, don't panic and don't ignore it. We've written a full playbook on responding to IRS crypto tax notices.

Record-Keeping When There's No 1099: The System

Good Polymarket tax reporting starts with data, and since nobody sends you numbers, you build them. For every position, capture:

- Market name and outcome side (which question, Yes or No)

- Acquisition date and time

- USDC cost (your basis)

- Disposal date (sale or market resolution)

- USDC proceeds (sale price or $1.00-per-share settlement, $0 if lost)

- Holding period (drives short vs long term under capital treatment)

Then layer in the USDC side: where the funding USDC came from (exchange purchase, swap, prior winnings), its basis, and where withdrawals went.

Your sources, in order of authority:

- The Polygon blockchain itself. Every acquisition, exit, and redemption is permanently on-chain. This is the audit trail the IRS can see too.

- Your Polymarket account history. Adds market context (which event, when it resolved) to the raw chain data.

- Exchange records for on-ramps and off-ramps.

For a handful of trades, a spreadsheet works. Past a few dozen, use tooling: general crypto tax software can ingest Polygon wallet activity, and Polymarket-specific report generators now exist that read your wallet address and build Form 8949 output directly. Whatever you use, reconcile the output against your account history before filing. Automated classifiers mislabel prediction market redemptions constantly. Our guide to crypto-to-crypto trades explains why every disposal needs its own line.

Action steps:

- Export your full Polymarket trade history today, not in April.

- Pull your Polygon wallet transactions for the same period.

- Match every deposit and withdrawal to an exchange record.

- Pick your framework, write one paragraph explaining why, and keep it with your tax file.

Polymarket Taxes vs Kalshi and Robinhood: One Big Difference

Quick context, because most traders use more than one platform.

Kalshi settles in dollars and provides some tax documentation (a P&L statement, 1099-INT for interest, 1099-MISC for rewards, and crypto-related forms through its custodian). Robinhood's event contracts settle in dollars too, though Robinhood has said it won't issue 1099s for them. Polymarket settles in USDC and issues nothing.

That settlement difference is the whole ballgame: fiat platforms give you a starting point and no crypto layer; Polymarket gives you no forms plus a crypto layer. We break down every major platform, including Kalshi's actual form list and the crypto-settled exchanges like Limitless and Drift BET, in our companion guide to prediction market taxes.

Common Polymarket Tax Mistakes We See (and How to Avoid Them)

After enough prediction market returns, the same five mistakes keep showing up:

- Assuming no 1099 means no Polymarket taxes owed. The most common and the most dangerous. On-chain activity plus exchange 1099-DAs make this visible.

- Ignoring the USDC layer. Reporting the contracts but not the stablecoin disposals leaves a gap that a 1099-DA will eventually expose.

- Grabbing Section 1256 for the 60/40 rate without analysis. The swap exclusion question is real. Aggressive positions need documentation and disclosure, not vibes.

- Treating wins as capital gains and losses as gambling. Pick one framework. Cherry-picking the favorable side of two frameworks is indefensible under exam.

- Waiting until April to reconstruct a year of trades. On-chain forensics under deadline pressure is how errors (and overpayments) happen.

There's a sixth mistake that costs more than the other five combined: overpaying a generalist to guess. A preparer who has never touched a Polygon transaction will either over-report your income or under-document your position. Here's what a crypto-specialized CPA actually costs, and here's how to vet one.

When to Handle It Yourself vs Hire a CPA

Being honest with you:

Handling Polymarket taxes yourself is fine if: you made a handful of trades, your net result is small, you're comfortable choosing ordinary income or capital treatment, and your records are clean.

Get professional help if: you traded five figures or more, you have hundreds of positions, you're considering a Section 1256 position, you have multi-year unreported activity from the offshore era, you received an IRS notice, or your Polymarket activity sits inside a bigger crypto picture (our complete crypto tax guide shows how it all fits together).

93% notice reduction

Across 200+ IRS crypto notices we've handled, the overwhelming majority were resolved with reconstructed records and a documented reporting position.

The pattern we see every season: traders who reconstruct records and file a defensible position sleep fine, even in gray areas. Traders who file nothing hope the gray area protects them. It doesn't. Unreported income plus interest plus accuracy penalties is a much worse outcome than any framework's tax bill.

Get Your Polymarket Year Filed Right

Flat-fee reconstruction and filing for prediction market traders. Garrett reviews your wallet history, picks the defensible framework for your facts, and signs the return.

Book a callFAQ: Polymarket Taxes

Frequently Asked Questions

Do you have to pay taxes on Polymarket gains?

Yes. All Polymarket profits are taxable income under Section 61 of the tax code, whether you receive a tax form or not, and whether or not you convert your USDC winnings back to dollars. The taxable event is the sale or settlement of the position, not the withdrawal to your bank.

Does Polymarket give you a 1099?

No. As of mid-2026, Polymarket issues no Form 1099-B, 1099-DA, or W-2G, even after relaunching as a CFTC-regulated US exchange in January 2026. You must calculate and report your own gains and losses from your trade history and Polygon wallet records.

Can you write off Polymarket losses?

Usually yes, but how depends on your tax treatment. Under capital asset treatment, losses offset capital gains plus up to $3,000 of ordinary income per year, with carryforward. Under ordinary income treatment, net losses are generally deductible. Under gambling treatment, losses only help if you itemize, and from 2026 they're capped at 90% of losses under the One Big Beautiful Bill Act.

Do I have to report Polymarket to the IRS?

Yes. Every disposal of a position (sale or settlement) is a reportable event, and your USDC activity makes you answer yes to the Form 1040 digital asset question. Polymarket transactions are publicly recorded on the Polygon blockchain, and your exchange withdrawals appear on 1099-DA forms the IRS already receives.

Is Polymarket gambling or investing for tax purposes?

The IRS has not said. Practitioners file under four frameworks: capital asset, ordinary income, gambling, or Section 1256. Most filers choose capital asset or ordinary income treatment. Gambling treatment carries the harshest loss rules, especially after the 2026 OBBBA 90% loss cap.

What tax form do I use for Polymarket?

It depends on your framework. Capital asset treatment uses Form 8949 and Schedule D. Ordinary income uses Schedule 1, Line 8z. Gambling uses Schedule 1 for winnings and Schedule A for losses. Section 1256, an aggressive position for Polymarket, uses Form 6781.

Do I get taxed if I made less than $600 on Polymarket?

Yes. The $600 figure is a threshold for platforms issuing certain 1099 forms, not a tax exemption. All income is taxable from the first dollar. Since Polymarket issues no forms at any threshold, the amount is irrelevant: you report whatever you made.

Does Polymarket report to the IRS?

Polymarket itself files no information returns on your trading. But your activity is not invisible: it lives permanently on the Polygon blockchain, and when you move USDC through a US exchange, that exchange reports your proceeds to the IRS on Form 1099-DA.

How much capital gains tax will I pay on $100,000 of Polymarket profit?

Under capital asset treatment, most Polymarket gains are short-term and taxed at ordinary rates. A single filer with $100,000 of short-term gains on top of a $120,000 salary would pay roughly $32,000 in additional federal tax at 2026 rates, plus state tax. Long-term treatment, rare for fast-resolving markets, would cut that dramatically.

Do taxes apply to old offshore Polymarket trades from before the US relaunch?

Yes. US taxpayers owe tax on worldwide income, including trades made on the offshore platform between 2022 and 2025. If you have unreported prior years, fixing them proactively through amended returns is far cheaper than waiting for an IRS letter.

Does the wash sale rule apply to Polymarket trades?

Under current law, no. The wash sale rule in Section 1091 applies to stocks and securities, and prediction market contracts, like crypto generally, fall outside it. You can realize a loss and re-enter the same market, though Congress has repeatedly proposed extending wash sale rules to digital assets.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Prediction Market Taxes (2026): How Kalshi, Polymarket, Robinhood and Every Major Platform Gets Taxed

How prediction market taxes work on Kalshi, Polymarket, Robinhood and more. A CPA splits platforms by settlement type and shows exactly what to report.

The Ultimate Guide to Crypto Tax (2026 Edition)

The most comprehensive crypto tax guide online, written by a CPA who files 500+ crypto returns a year. Every taxable event, form, strategy, and 2026 update.

IRS Crypto Tax Notices: What to Do If You Get One

Got an IRS crypto notice? Learn exactly how to respond to CP2000, Letter 6173, and Letter 6174 notices. Step-by-step response guide from a crypto tax CPA.