Crypto Cost Basis Methods: FIFO vs Specific ID vs HIFO

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Your cost basis method determines which coins you "sell first", and that directly controls your tax bill.

- ✓FIFO is the IRS default. If you don't pick a method, you're using FIFO whether you like it or not.

- ✓HIFO (Highest In, First Out) minimizes taxes but isn't explicitly endorsed by the IRS, it's treated as a subset of Specific Identification.

- ✓Specific Identification gives you maximum control but requires contemporaneous records at the time of each sale.

- ✓Rev. Proc. 2024-28 now requires per-wallet, per-account cost basis tracking, no more pooling across exchanges.

- ✓Starting in 2026, brokers issue 1099-DA forms and may report cost basis differently than your own records.

- ✓Picking the wrong method (or no method) can cost you tens of thousands in unnecessary taxes over a bull market cycle.

- ✓Notice 2026-20 extends specific ID relief through December 31, 2026: you can identify the lots you sold using your own books and records while brokers build lot-level systems.

“The cost basis method you choose can swing your crypto tax bill by thousands of dollars, and starting in 2025, the IRS locked you into per-wallet accounting. Choose wisely.”

, Reviewed by Leanne Grant, EA

Quick answer: Your crypto cost basis is what you originally paid for a coin (including fees). When you sell, you subtract the cost basis from the sale price to calculate your gain or loss. The method you use, FIFO, LIFO, HIFO, or Specific Identification, determines which coins are treated as sold first. FIFO is the default. Specific Identification with HIFO ordering typically produces the lowest tax bill. But after Rev. Proc. 2024-28, you need to track basis per wallet, and you need proper records to back up any method besides FIFO.

Update (July 9, 2026): Notice 2026-20 Extends Specific ID Relief Through the End of 2026

The IRS has extended the transition relief that makes specific identification workable while brokers catch up. Notice 2026-20 extends the temporary relief originally granted in Notice 2025-7 for one more year, so the relief period now runs from January 1, 2025 through December 31, 2026.

Here is what that means in practice. For crypto held in the custody of a broker, you can make an adequate specific identification of the units you sell using your own books and records: either identify the exact lots no later than the date and time of the sale, or record a standing order in your records before the units are sold. You do not have to communicate the identification to your broker during the relief period, because most brokers still cannot accept lot-level instructions.

The fine print that matters:

- The relief covers broker-held units only. Coins in your own self-custody wallets follow the regular per-wallet ordering rules and are not covered.

- If you make no identification at all, the broker-account FIFO default still applies.

- If you are using the Rev. Proc. 2024-28 safe harbor for pre-2025 holdings, you can rely on this relief only after your basis allocation is complete.

- Expect mismatches: the IRS acknowledges that broker-reported basis and acquisition dates may not match your records for 2026 sales, and your documentation is what completes the picture.

The clock matters. After December 31, 2026, specific identification of broker-held units must be communicated to your broker by the time of the sale. Build the books-and-records habit now. And if your 1099-DA forms already disagree with your numbers, our walkthroughs on what to do when a 1099-DA arrives and fixing 1099-DA mismatches cover the reconciliation step by step.

What Is Cost Basis in Crypto?

Cost basis is the original value of a crypto asset for tax purposes. It includes the purchase price plus any transaction fees you paid to acquire it.

When you sell, swap, or spend crypto, the IRS requires you to calculate the difference between your sale proceeds and your cost basis. That difference is your capital gain (or loss).

Here's the problem: most crypto investors don't buy all their coins at once. You might buy Bitcoin at $30,000 in January, $45,000 in June, and $38,000 in November. When you sell some of that Bitcoin, which purchase price counts as your basis?

That's what cost basis methods solve. They're the rules for matching your sales to your purchases.

This isn't optional. Form 8949 requires you to report the cost basis for every single crypto disposal. Get it wrong, and you're looking at penalties, interest, or an audit.

If you're new to crypto taxes generally, start with our complete crypto tax guide for 2026, it covers the fundamentals before you dive into cost basis specifics.

FIFO (First In, First Out), The Default

FIFO means the coins you bought first are treated as the coins you sold first.

How it works: Your purchases are lined up chronologically. When you sell, the IRS assumes you're disposing of your oldest coins.

Why it matters: In a rising market (which crypto has been for most of its history), your oldest coins have the lowest cost basis. That means FIFO typically produces the highest taxable gain.

IRS status: FIFO is the default method under Rev. Proc. 2024-28. If you don't actively choose and document a different method, you're on FIFO automatically.

The upside of FIFO:

- Zero record-keeping burden beyond basic transaction history

- No risk of IRS challenge on method selection

- More of your gains qualify as long-term (held over 1 year) since you're selling oldest lots first

The downside:

- In bull markets, you pay the most tax

- You have no flexibility to optimize

Best for: Investors who want simplicity, those with mostly long-term holdings, or anyone who hasn't kept detailed records.

LIFO (Last In, First Out), Not Recommended for Crypto

LIFO means your most recently purchased coins are treated as sold first.

How it works: The opposite of FIFO. Your newest purchases get matched to your sales.

Why it's problematic for crypto: LIFO is accepted for inventory accounting in certain business contexts, but the IRS has never explicitly approved LIFO for capital asset dispositions like crypto sales. Notice 2014-21 treats crypto as property, not inventory.

The bigger issue: LIFO tends to produce short-term gains (taxed at ordinary income rates up to 37%) because you're always selling your newest coins. That's usually worse than FIFO from a pure tax perspective.

Best for: Almost nobody. If you want to sell recent lots, use Specific Identification instead, you get the same result with actual IRS backing.

HIFO (Highest In, First Out), The Tax Minimizer

HIFO means the coins with the highest cost basis are treated as sold first, regardless of when you bought them.

How it works: Every time you sell, the lot with the highest per-unit cost gets depleted first. This maximizes your cost basis and minimizes your taxable gain.

IRS status, and this is important: The IRS has not explicitly endorsed HIFO as a standalone method. HIFO is widely used and accepted by crypto tax software, but technically it functions as a subset of Specific Identification. You're specifically identifying the highest-cost lots for each sale.

This means HIFO carries the same record-keeping requirements as Specific ID (more on that below). You can't just claim HIFO retroactively without documentation.

The upside:

- Produces the lowest possible taxable gain (or largest loss)

- Widely supported by crypto tax platforms

- Defensible as Specific ID if you have records

The downside:

- Requires lot-level tracking and contemporaneous documentation

- May produce more short-term gains (highest-cost lots are often recent purchases)

- No explicit IRS guidance endorsing the label "HIFO"

Best for: Active traders and high-net-worth investors who maintain detailed records and want to minimize current-year taxes. This is what many crypto tax CPAs, including our team, implement for clients.

Specific Identification, Maximum Control

Specific Identification means you choose exactly which lot to sell for each transaction.

How it works: At the time of each sale, you designate which specific coins you're disposing of. You might sell Lot 3 from August because it gives you a long-term loss, even though Lots 1 and 2 are older.

IRS requirements for Specific ID in crypto: Under Rev. Proc. 2024-28 and general IRS guidance, you need:

- Contemporaneous identification, You must identify the specific lot at the time of the sale (or within a reasonable time), not retroactively at tax time Through December 31, 2026, Notice 2026-20 lets you make this identification in your own books and records for broker-held units, without notifying the broker.

- Adequate records, Transaction IDs, timestamps, wallet addresses, and lot details

- Per-wallet/per-account tracking, As of January 1, 2025, you must track lots separately for each wallet and exchange account

Why this is the gold standard: Specific ID gives you complete flexibility. You can pick the lot that produces the best tax outcome for each individual transaction:

- Sell high-basis lots to minimize gains

- Sell lots held over 12 months to get long-term capital gains rates

- Harvest losses strategically (though keep an eye on crypto wash sale rules)

Best for: Investors who work with a crypto tax CPA or use professional-grade tracking. This is what we recommend to most COS Elite clients, it gives you the most options at tax time.

Rev. Proc. 2024-28: The Per-Wallet/Per-Account Rule

This is the rule that changed everything for crypto cost basis tracking, and most investors still don't know about it.

What it says: Starting January 1, 2025, you must track cost basis separately for each wallet and each exchange account. You cannot pool your cost basis across platforms.

What this means in practice:

Say you hold ETH on Coinbase, Kraken, and a Ledger hardware wallet. Before 2025, many investors (and tax software tools) would pool all their ETH into a single "universal" ledger and apply FIFO or HIFO across the entire pool.

That's no longer allowed.

Now, if you sell 3 ETH on Coinbase, only your Coinbase ETH lots can supply the cost basis. Your Kraken lots and Ledger lots are irrelevant to that sale.

Why this matters for cost basis methods:

- FIFO now applies per wallet, the oldest lot in that specific wallet gets sold first

- Specific ID can only reference lots in the wallet where the sale occurs

- Transfers between wallets get complicated, you need to document which specific lots you moved

This is one of the biggest reasons crypto investors need professional digital asset reconciliation. The per-wallet rule makes DIY tracking exponentially harder, especially if you use DeFi protocols or multiple exchange accounts.

For a deeper look at how trades between different crypto assets trigger taxes, see our breakdown on crypto-to-crypto trade taxation.

How 1099-DA Changes Cost Basis Reporting (2026+)

Starting in tax year 2025 (forms issued in early 2026), crypto brokers are required to issue Form 1099-DA, the Digital Asset equivalent of a 1099-B for stocks.

What 1099-DA reports:

- Gross proceeds from crypto sales

- Cost basis (if the broker has it)

- Whether gains are short-term or long-term

- Transaction dates and asset descriptions

The cost basis problem: Brokers will report cost basis only for assets purchased on their platform. If you transferred crypto in from another exchange or wallet, the broker likely has zero cost basis data for those coins.

When that happens, the 1099-DA will show your cost basis as "unknown" or zero. And the IRS gets a copy.

What this means for you:

If the IRS sees a 1099-DA showing $50,000 in proceeds and $0 in cost basis, their computer flags the entire $50,000 as a gain. You'll need to prove your actual basis with your own records.

This is where your cost basis method and documentation become critical. If you've been using Specific ID with proper records, you can substantiate your basis. If you've been winging it, 2026 is going to be a rough tax year.

Broker vs. taxpayer basis methods: Your broker will likely default to FIFO for the assets it tracks. If you use a different method (like Specific ID or HIFO), your tax return will differ from the 1099-DA. That's allowed, but you need records to back it up. Under Notice 2026-20, your own books and records control which lots you sold through the end of 2026, even when the broker's form shows different basis or dates.

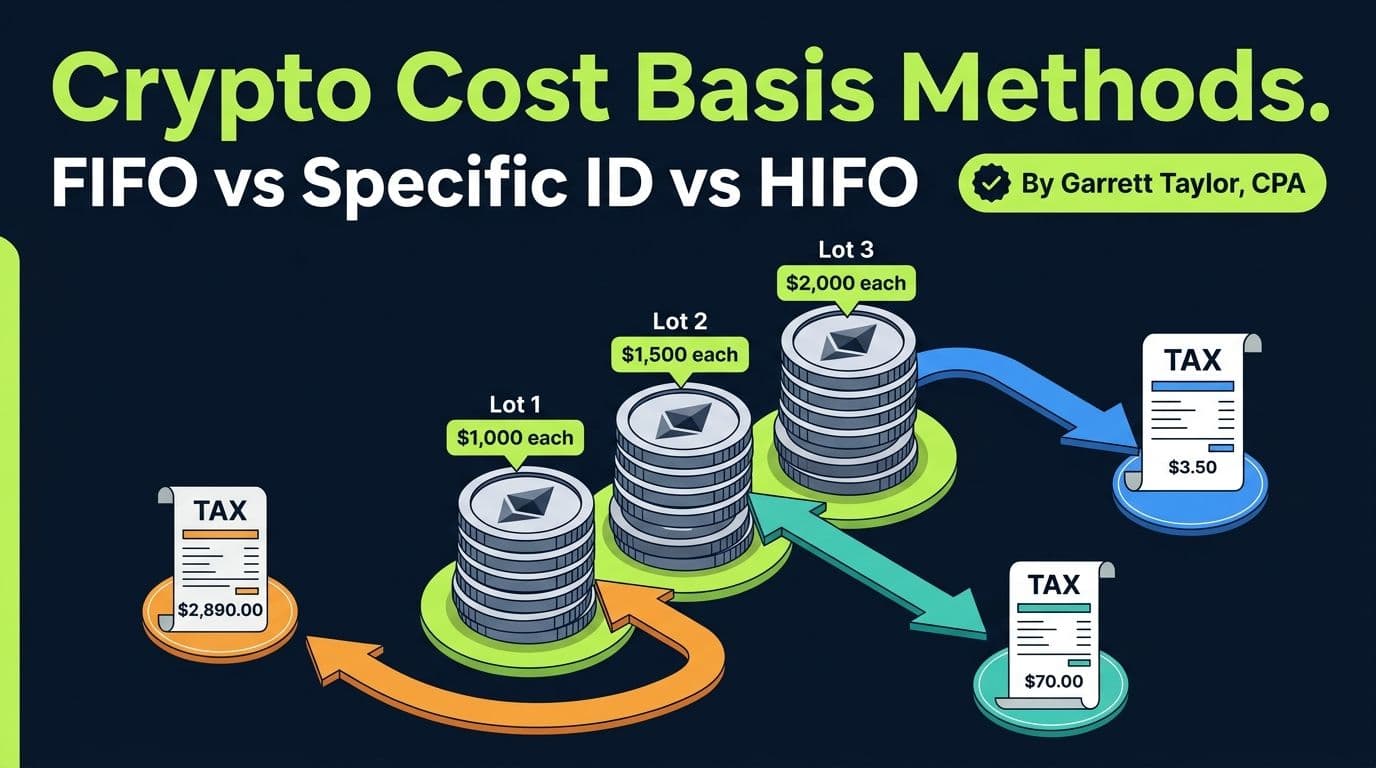

Worked Example: Same 5 Trades, 4 Different Methods, 4 Different Tax Bills

This is where cost basis methods go from abstract to concrete. Let's walk through a real scenario.

Your ETH purchases (5 lots):

| Lot | Date | Quantity | Price per ETH | Total Cost (incl. fees) | Holding Period at Sale |

|---|---|---|---|---|---|

| Lot 1 | Jan 15, 2024 | 2 ETH | $1,500 | $3,000 | Long-term (>1 yr) |

| Lot 2 | Apr 10, 2024 | 1 ETH | $2,800 | $2,800 | Long-term (>1 yr) |

| Lot 3 | Aug 22, 2024 | 3 ETH | $3,100 | $9,300 | Short-term (<1 yr) |

| Lot 4 | Nov 5, 2024 | 1 ETH | $1,900 | $1,900 | Short-term (<1 yr) |

| Lot 5 | Feb 18, 2025 | 2 ETH | $3,400 | $6,800 | Short-term (<1 yr) |

Total holdings: 9 ETH | Total cost: $23,800

The sale: On May 1, 2025, you sell 3 ETH at $3,800 each. Total proceeds: $11,400.

Now let's see how each method handles this sale.

Under FIFO (First In, First Out)

Sells the oldest lots first:

- Lot 1: 2 ETH at $1,500 basis = $3,000 basis (long-term)

- Lot 2: 1 ETH at $2,800 basis = $2,800 basis (long-term)

- Total basis: $5,800

- Total gain: $11,400 - $5,800 = $5,600

- Character: 100% long-term capital gain

- Tax (at 15% LTCG rate): $840

Under LIFO (Last In, First Out)

Sells the newest lots first:

- Lot 5: 2 ETH at $3,400 basis = $6,800 basis (short-term)

- Lot 4: 1 ETH at $1,900 basis = $1,900 basis (short-term)

- Total basis: $8,700

- Total gain: $11,400 - $8,700 = $2,700

- Character: 100% short-term capital gain

- Tax (at 32% ordinary rate): $864

Under HIFO (Highest In, First Out)

Sells the highest-cost lots first:

- Lot 5: 2 ETH at $3,400 basis = $6,800 basis (short-term)

- Lot 3: 1 ETH at $3,100 basis = $3,100 basis (short-term)

- Total basis: $9,900

- Total gain: $11,400 - $9,900 = $1,500

- Character: 100% short-term capital gain

- Tax (at 32% ordinary rate): $480

Under Specific Identification (Optimized)

A crypto tax CPA would cherry-pick the best combination. Here, we select lots that balance high basis with favorable long-term treatment:

- Lot 2: 1 ETH at $2,800 basis = $2,800 basis (long-term)

- Lot 5: 2 ETH at $3,400 basis = $6,800 basis (short-term)

- Total basis: $9,600

- Total gain: $11,400 - $9,600 = $1,800

- Character: $1,000 long-term + $800 short-term

- Tax: ($1,000 x 15%) + ($800 x 32%) = $150 + $256 = $406

| Method | Lots Sold | Total Basis | Taxable Gain | Gain Character | Estimated Tax |

|---|---|---|---|---|---|

| FIFO | Lot 1 + Lot 2 | $5,800 | $5,600 | 100% long-term | $840 |

| LIFO | Lot 5 + Lot 4 | $8,700 | $2,700 | 100% short-term | $864 |

| HIFO | Lot 5 + Lot 3 (partial) | $9,900 | $1,500 | 100% short-term | $480 |

| Specific ID (optimized) | Lot 2 + Lot 5 | $9,600 | $1,800 | Mixed | $406 |

Look at that spread. The difference between the worst method (LIFO at $864) and the best (Specific ID at $406) is $458 on a single 3 ETH sale. Scale that across a year of active trading and the difference can be five figures.

Pro Tip

The "best" method isn't always HIFO. In this example, Specific ID beat HIFO by $74 because it captured a long-term gain on Lot 2 at the favorable 15% rate. A good crypto CPA runs the numbers both ways for every disposal.

| Feature | FIFO | LIFO | HIFO | Specific ID |

|---|---|---|---|---|

| How it works | Sell oldest lots first | Sell newest lots first | Sell highest-cost lots first | Choose any lot per sale |

| IRS status | Default method | Not endorsed for crypto | Treated as subset of Spec ID | Explicitly allowed |

| Tax impact (bull market) | Highest gains | Mixed | Lowest gains | Optimized per sale |

| Long-term gain potential | High | Low | Low | Maximum flexibility |

| Record-keeping burden | Minimal | Minimal | Moderate | High |

| Per-wallet tracking | Required (2025+) | Required (2025+) | Required (2025+) | Required (2025+) |

| Best for | Simple portfolios | Almost nobody | Active minimizers | CPA-managed portfolios |

| Risk level | None | High (unsupported) | Low-moderate | Low (with records) |

Which Method Should You Use?

There's no single answer, but here's the decision framework we use with clients:

Use FIFO if:

- You buy and hold with minimal trading

- You don't have detailed lot-level records

- Most of your holdings are long-term anyway

- You want zero complexity

Use Specific ID (with HIFO ordering) if:

- You actively trade or have significant unrealized gains

- You work with a crypto tax CPA or use professional tracking software

- You can maintain contemporaneous records for every sale

- You want to minimize taxes legally

Avoid LIFO. There's no scenario where LIFO is better than Specific ID for crypto.

Important note on switching methods: You can change your cost basis method, but you cannot retroactively change past disposals. If you've been using FIFO and want to switch to Specific ID, the switch applies going forward. Lots already "used" under FIFO stay as reported.

If you earn crypto through staking or mining, your cost basis is the fair market value at the time you receive the coins. The method you choose then determines the order those lots get sold.

Common Cost Basis Mistakes

1. Pooling basis across exchanges. After Rev. Proc. 2024-28, this is flat-out wrong. Each wallet and exchange account is its own silo.

2. Forgetting transfer basis. When you move crypto from Coinbase to your Ledger, the cost basis travels with it. But you need to document which lots transferred.

3. Using $0 basis for airdrops, forks, or staking rewards. Many of these events have a cost basis equal to the fair market value at the time of receipt (which is also taxable income).

4. Retroactively "choosing" HIFO at tax time. Specific ID requires you to identify lots at the time of sale, not in April when you're filing. If you didn't designate at the time, you're stuck with FIFO. Notice 2026-20 lets the designation live in your own books and records through the end of 2026, but it still has to exist by the time of the sale.

5. Ignoring fees. Transaction fees, gas fees, and exchange commissions are all part of your cost basis. They reduce your gain.

6. Not reconciling with 1099-DA. Starting in 2026, if your reported basis doesn't match the 1099-DA, you need Form 8949 adjustments. Don't ignore mismatches, the IRS won't.

When You Need a Crypto Tax CPA

DIY cost basis tracking works if you have a simple portfolio: one exchange, buy-and-hold, minimal transactions.

But if any of these apply, you likely need professional help:

- You trade on multiple exchanges or use DeFi protocols

- You've transferred crypto between wallets without tracking lot movements

- You've received 1099-DA forms with missing or incorrect cost basis

- You want to use Specific Identification but haven't kept contemporaneous records

- You have unrealized gains over $50,000 and want to plan disposals strategically

- You've been using the wrong method and need to correct prior filings

At COS Elite, crypto cost basis optimization is a core part of our tax return preparation service. We reconstruct transaction histories, reconcile across wallets, and apply the method that legally minimizes your tax, all documented to withstand IRS scrutiny.

For investors with complex transaction histories across multiple wallets and protocols, our digital asset reconciliation service traces every lot from acquisition to disposal.

Find Your Optimal Cost Basis Method

Stop overpaying on crypto taxes. The difference between FIFO and optimized Specific ID can be thousands of dollars per year. Book a free consultation with COS Elite to find out which cost basis method saves you the most, and make sure your records back it up.

Schedule Your Free Crypto Tax ReviewFree 15 minute call. No commitment.

Frequently Asked Questions

What is the default cost basis method for crypto?

FIFO (First In, First Out) is the default. Under Rev. Proc. 2024-28, if you don't specifically identify which lots you're selling at the time of each transaction, FIFO applies automatically.

Is HIFO legal for crypto taxes?

HIFO is not explicitly named in IRS guidance, but it's treated as a form of Specific Identification, which is explicitly allowed. As long as you meet the Specific ID documentation requirements (contemporaneous identification, adequate records), HIFO ordering is defensible.

Can I switch from FIFO to Specific Identification?

Yes, you can switch going forward. However, you cannot retroactively change the method used for past sales. Any lots already disposed of under FIFO remain as reported.

What does Rev. Proc. 2024-28 require for cost basis?

Starting January 1, 2025, you must track cost basis separately for each wallet and exchange account. You can no longer pool basis across platforms. You must also select your accounting method at the account level.

How does 1099-DA affect my cost basis reporting?

Brokers issue 1099-DA starting in 2026 (for tax year 2025). They report cost basis only for assets purchased on their platform. If you transferred crypto in, the broker may report zero basis, and you'll need your own records to prove the correct amount.

What records do I need for Specific Identification?

You need the date and time of each purchase, the quantity and price per unit, transaction IDs or hashes, the wallet or exchange where the purchase occurred, and documentation showing which specific lot you designated at the time of each sale.

Does cost basis include transaction fees?

Yes. Gas fees, exchange commissions, and network fees paid to acquire crypto are all added to your cost basis. Fees paid on the sale side reduce your net proceeds.

What happens if I don't know my cost basis?

If you cannot determine your cost basis, the IRS may treat it as $0, meaning your entire sale proceeds are taxable. This is exactly what happens when a 1099-DA shows unknown basis. Reconstructing your transaction history with a crypto CPA can often recover your actual basis.

Can I use different methods for different coins?

Yes, you can use FIFO for one asset and Specific ID for another. However, under Rev. Proc. 2024-28, the method is applied at the wallet/account level, so consistency within each account is required.

Is LIFO allowed for crypto?

The IRS has not endorsed LIFO for crypto (which is treated as property, not inventory). While some taxpayers have used it, LIFO is risky and rarely produces better results than Specific Identification anyway.

How do I track cost basis for crypto-to-crypto trades?

Each crypto-to-crypto trade is a taxable event. You recognize gain or loss on the coin you're disposing of (using your chosen cost basis method), and the coin you receive gets a new cost basis equal to its fair market value at the time of the trade. See our guide on [how crypto-to-crypto trades are taxed](/blog/crypto-to-crypto-trades-taxes).

What if my exchange was hacked or shut down and I lost records?

Blockchain records are permanent, so a crypto tax professional can often reconstruct your transaction history from on-chain data. This is part of what COS Elite's [digital asset reconciliation](/services/digital-asset-reconciliation) service covers.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

The Ultimate Guide to Crypto Tax (2026 Edition)

The most comprehensive crypto tax guide online, written by a CPA who files 500+ crypto returns a year. Every taxable event, form, strategy, and 2026 update.

Crypto-to-Crypto Trades: Tax Treatment Explained

Every crypto-to-crypto swap is taxable. Learn how to calculate gain/loss, why Section 1031 doesn't apply, and how to handle stablecoin swaps, wrapped tokens, and DEX trades.

Wash Sale Rules and Crypto: The Loophole That Won't Last

The wash sale rule doesn't apply to crypto, yet. Learn how to tax-loss harvest crypto in 2026, what legislation could change, and how to maximize savings before the loophole closes.

I Got a 1099-DA, Now What? A CPA Walks Through Every Box (2026)

Form 1099-DA reports your crypto proceeds to the IRS, usually with no cost basis. A CPA explains every box, what to do before filing, and when to amend.

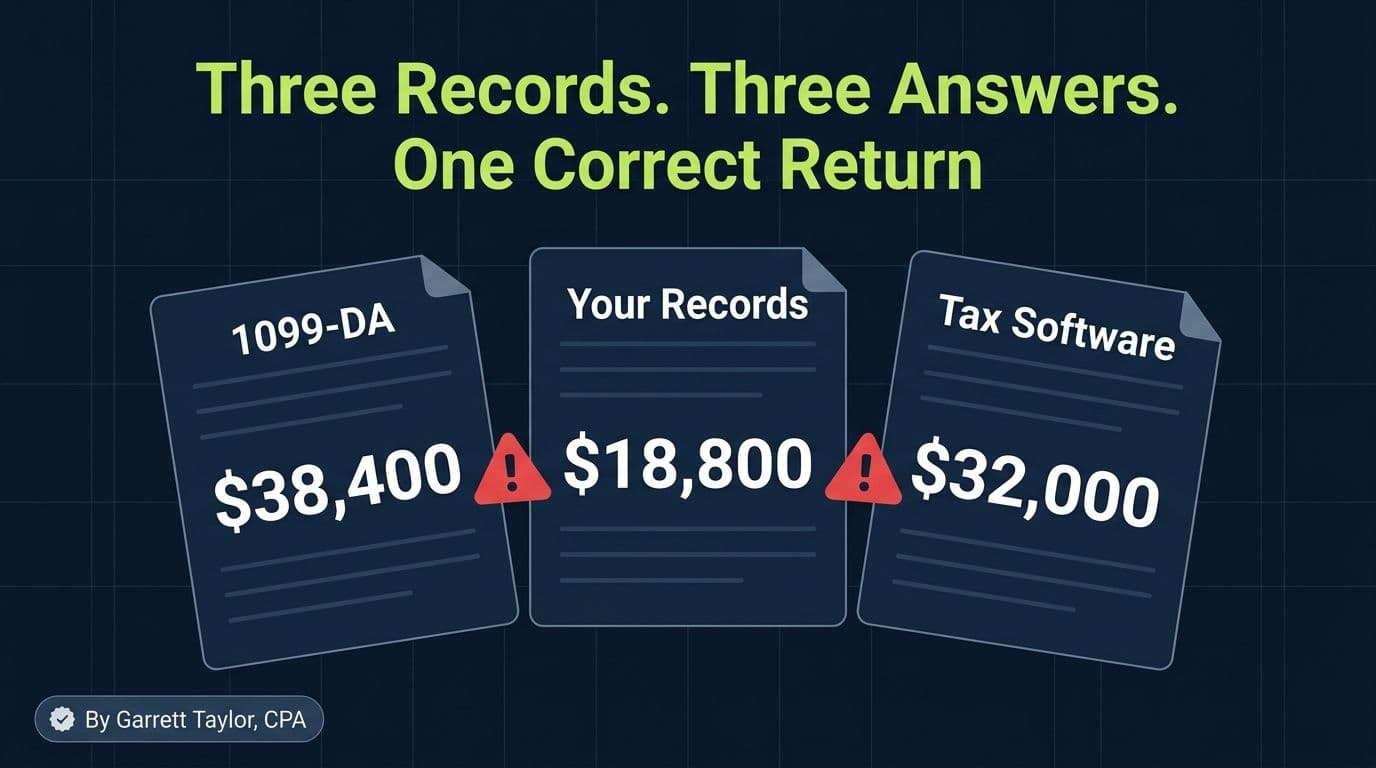

Your 1099-DA Doesn't Match Your Records: The Three-Record Problem, Fixed (2026)

Your 1099-DA, your wallet history, and your tax software all disagree. A CPA explains the five common mismatches and the exact reconciliation workflow.