Your 1099-DA Doesn't Match Your Records: The Three-Record Problem, Fixed (2026)

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Every crypto filer now juggles three records: the broker's 1099-DA, their own wallet and exchange history, and their tax software's output. The three were never designed to agree, and in 2026 they usually don't.

- ✓The 1099-DA systematically overstates gains because brokers can't see the basis of coins acquired before 2026 or transferred in from elsewhere. Blank basis is a data gap, not a tax bill.

- ✓The IRS matches only the proceeds side. Your Form 8949 must account for every dollar of Box 1f, but your documented basis overrides anything the form left blank or got wrong.

- ✓Unmatched transfers are the number one source of phantom gains: one wallet-to-exchange move misread as a sale can fabricate tens of thousands in taxable income.

- ✓Reconcile before you file, not after the CP2000 arrives. The automated notice proposes tax on full proceeds with zero basis credit, plus a 20% accuracy penalty and interest.

Pro Tip

Written by Garrett Taylor, CPA (License #133092). Reviewed by Leanne Grant, EA (#00167954-EA). Last updated: July 9, 2026.

Quick answer: When your 1099-DA disagrees with your own transaction history and your crypto tax software, you file the numbers you can prove, not the broker's incomplete version and not the software's guess. The 1099-DA's proceeds must be accounted for on your Form 8949 because the IRS matches that number by computer, but the basis, the gain, and the holding period come from your substantiated records. This guide explains why the three records disagree, the five most common mismatches, and the exact reconciliation workflow we use, with a full worked example.

You've got three numbers in front of you.

The 1099-DA from your exchange says one thing. Your own spreadsheet of what you bought and sold says another. And your crypto tax software, the tool that was supposed to settle this, says a third thing entirely.

None of them agree. The gaps aren't small. And the filing deadline doesn't care.

Here's what nobody tells you up front: this is normal. Not fine, not safe to ignore, but normal. The 2026 filing season is the first in which broker reporting, personal records, and software output all collide on the same return, and the collision has a name in our office: the three-record problem. We reconcile these mismatches professionally, and every one we've seen traces back to a handful of causes with known fixes.

This is the complete repair manual.

The Three-Record Problem: Why Your 1099-DA, Your History, and Your Software All Disagree

Each of the three records was built by a different party, with different visibility, for a different purpose. Disagreement isn't a malfunction; it's the architecture.

What Each Record Knows (and Systematically Gets Wrong)

| Record | What It Knows | Where It Fails |

|---|---|---|

| Broker's 1099-DA | Exact proceeds and dates for disposals on that one platform | No basis for transferred-in or pre-2026 coins; sees only its own walls |

| Your wallet and exchange history | Everything you did, everywhere | Scattered across platforms, formats, and dead exchanges; rarely assembled in one place |

| Tax software output | Whatever you imported, processed by its matching rules | Garbage in, garbage out: missing imports become fake zero-basis lots and phantom gains |

The broker's record is narrow but loud. The 1099-DA reports gross proceeds from disposals on that platform, and the IRS gets a copy. For 2025 transactions, proceeds were mandatory to report and basis was voluntary, so most brokers reported proceeds only. Even under the full rules that started with 2026 acquisitions, a broker reports basis only for coins bought and kept at that broker. Anything that crossed a wallet boundary arrives with no price history attached.

Your record is complete but chaotic. Somewhere across your exchange accounts, wallets, emails, and bank statements exists the true story of every acquisition and disposal. In practice it's fragmented, partially exported, and in at least one place (a shut-down exchange, a lost login) missing entirely.

The software's record is a model, not the truth. Crypto tax software is a calculation engine running on the data you connected. Miss one exchange, one wallet, or one year, and the engine doesn't leave a polite gap. It fills the hole with assumptions: transfers become deposits from nowhere, deposits from nowhere become zero-basis acquisitions, and zero-basis acquisitions become gains you never earned.

Understanding which record is authoritative for which number is the whole game, so let's make it explicit.

Which Record Wins? What the IRS Actually Matches

The IRS's automated underreporter system does one comparison well: Box 1f proceeds on every 1099-DA filed under your Social Security number, against the proceeds you report on Form 8949. That's the tripwire. If the forms say $38,400 and your return accounts for $21,000, the computer flags you, no human required.

What the computer does not independently know is your cost basis for noncovered assets. That side of the ledger belongs to you, and the rules currently in force lean surprisingly hard in your favor:

- The 2025 form instructions themselves say that when basis is blank, you determine it from your own records.

- Under Notice 2026-20, through the end of 2026 you can make adequate specific identification of which units you sold using your own books and records, because most brokers still can't accept lot-level instructions. The IRS even acknowledges that broker-reported basis and acquisition dates may not match your records during this period, and anticipates the mismatch.

- Since January 1, 2025, basis must be tracked wallet by wallet. If you held crypto from before then, Revenue Procedure 2024-28 governed the one-time allocation of your old universal-pool basis to specific wallets and accounts. Your allocation records are part of your proof.

So the operating rule is: the form controls the proceeds conversation, your documentation controls the gain conversation. File a return where every 1099-DA dollar of proceeds is visible, attached to the basis you can substantiate, and a mismatch between the form and your software's first draft becomes a non-event.

“People assume the broker's form outranks their own records. It's the reverse. The broker is testifying about one account it can see. You're the only party in the room who knows the whole history, and the IRS's own transition guidance expects you to be the one who completes the picture.”

, Leanne Grant, EA

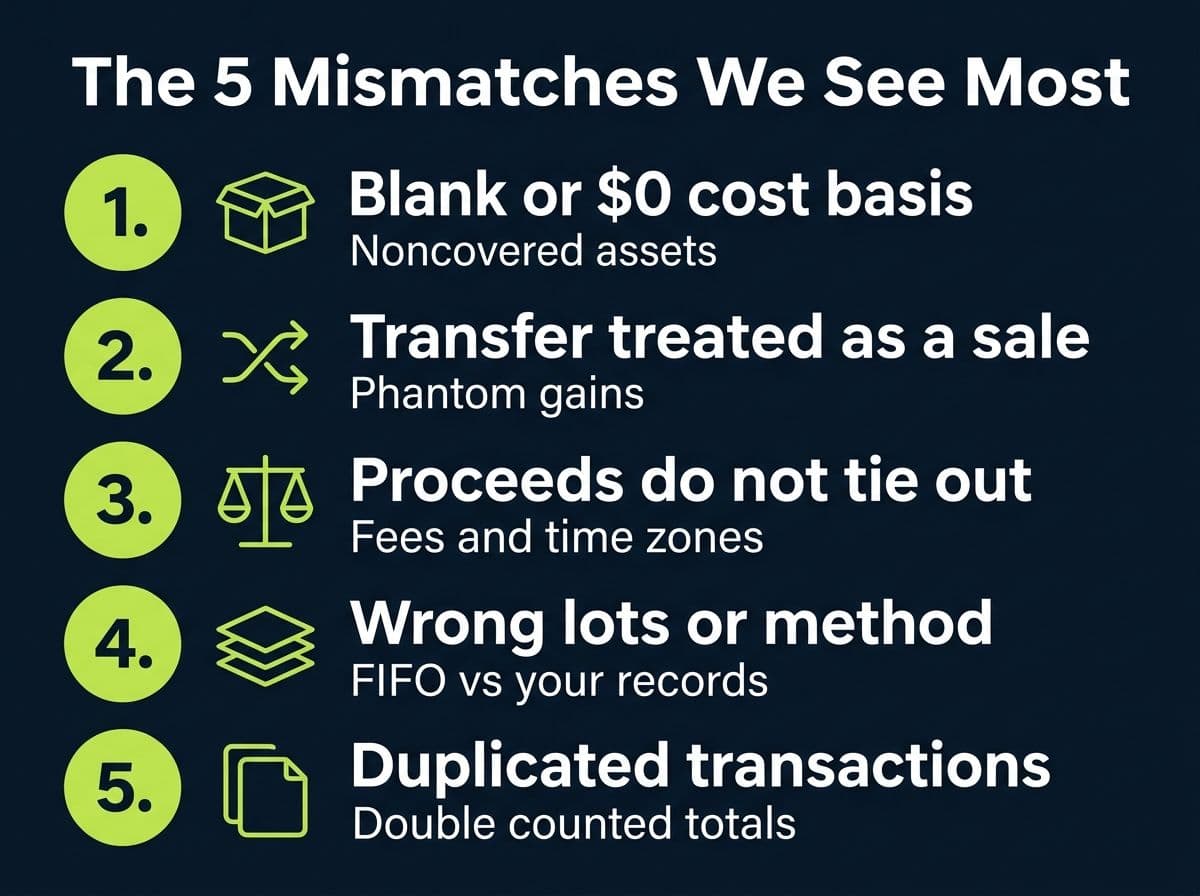

The Five Mismatches We See Most (and What Each One Means)

Nearly every "my 1099-DA is wrong" case lands in one of five buckets. Diagnose yours before touching anything.

Mismatch 1: Basis is blank or $0 on the 1099-DA. The classic. Box 1g empty, Box 9 (noncovered) checked, often with blank acquisition date and holding period too. Cause: you bought the coins before 2026 or transferred them in, so the broker never knew your cost. This isn't an error and no corrected form is coming; brokers can't report data they don't have. The fix is supplying basis yourself, documented, on Form 8949. One nuance from the instructions worth repeating: an actual $0 entry in Box 1g means the broker affirmatively reported zero basis to the IRS, which you should challenge with the broker if it's wrong, while a blank means nothing was reported at all.

Mismatch 2: A transfer is being treated as a taxable sale. Moving your own crypto between your own wallets and accounts is not a disposal. But your software sees coins leave one place and arrive in another, and if it can't link the two legs, it may book a sale on the way out and a zero-basis acquisition on the way in: two fake taxable events from one harmless move. On the broker side, Boxes 12a and 12b of the 1099-DA record units transferred in and the date, which is corroborating evidence, not income. Unmatched transfers are the single largest source of phantom gains we correct.

Mismatch 3: Proceeds don't tie out. The form says $38,400, your records say $38,150. Usual suspects: trading fees (gross versus net treatment), a disposal you booked in a different tax year because the broker reports in UTC time and your records use local time (a December 31 evening sale can land in different years), or an aggregated stablecoin line under Box 11a representing hundreds of small conversions as one total. Small, explainable proceeds differences need documentation, not panic.

Mismatch 4: The lots don't match. The broker's report (or your software's default) assumed FIFO, but you intended to sell specific higher-basis lots. Since the 2025 rules, lot identification happens per wallet, and through 2026 your own contemporaneous books and records are an acceptable way to identify lots under Notice 2026-20. Method differences quietly reshuffle gains between years and between short-term and long-term, which is why our guide to crypto cost basis methods is required reading before you recalculate anything.

Mismatch 5: Duplicates. The same disposal appears on the broker's form and again in your software from an imported wallet or API feed, or a platform issued multiple 1099-DA forms per asset and the totals got double-counted. Symptom: your software's proceeds exceed the sum of your forms plus your off-exchange sales. Deduplicate before you believe any total.

Pro Tip

Notice what's not on this list: the broker maliciously inflating your income. In our experience actual proceeds errors on 1099-DA forms are rare. The forms are incomplete far more often than they're wrong, and incomplete has a filing remedy that wrong doesn't need.

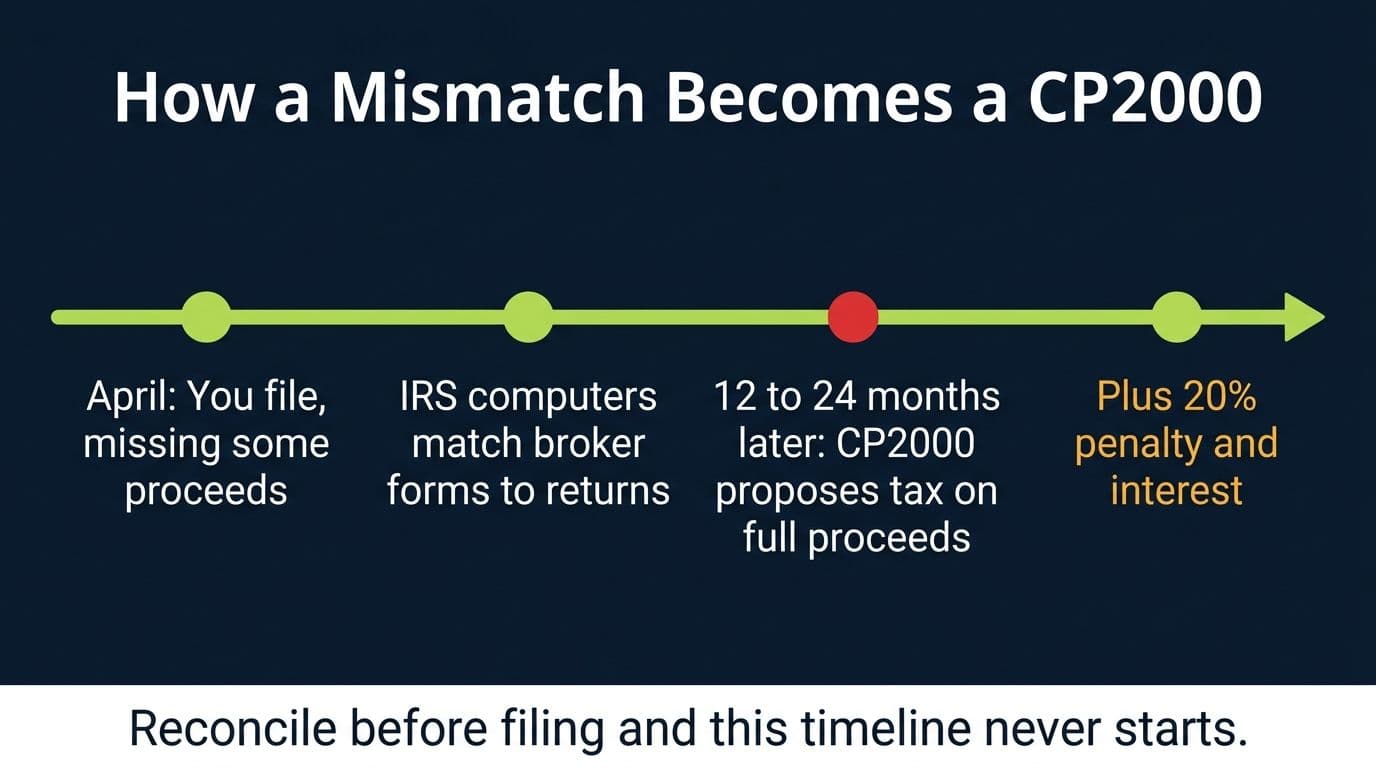

The Real Risk: How a Mismatch Becomes a CP2000 Notice

Here's what happens if you file without reconciling, in either direction.

Underreport the proceeds (skip the form, forget an account) and the automated underreporter system catches the gap when it matches broker filings to your return, typically 12 to 24 months after you file. Out comes a CP2000 notice: proposed additional tax, calculated the worst possible way. The computer knows your proceeds and not your basis, so it taxes the entire proceeds figure as gain, then adds a 20% accuracy-related penalty and interest backdated to the original due date.

A CP2000 is not a bill and not an audit; it's a proposal you must answer by the deadline printed on it, with documentation. Most crypto CP2000s shrink dramatically once real basis enters the conversation. But responding costs months, professional fees, and stress that a pre-filing reconciliation would have avoided entirely. If one has already landed, our guide to handling IRS crypto notices covers the response playbook, and if you need to know what the IRS already has on file, your Wage and Income transcript lists every form filed under your SSN.

Overreport (accept the blank basis as zero, let the software's phantom gains stand) and no notice ever comes. The IRS does not mail letters about overpayment. The money is simply gone unless you catch it and amend within the refund window, generally three years. One direction of sloppiness costs you a notice; the other costs you cash, silently.

12 to 24 months

Typical lag between filing a return that misses 1099-DA proceeds and receiving the CP2000 that proposes tax, penalty, and interest on the gap. The system is slow, automated, and extremely patient.

The 7-Step Reconciliation Workflow

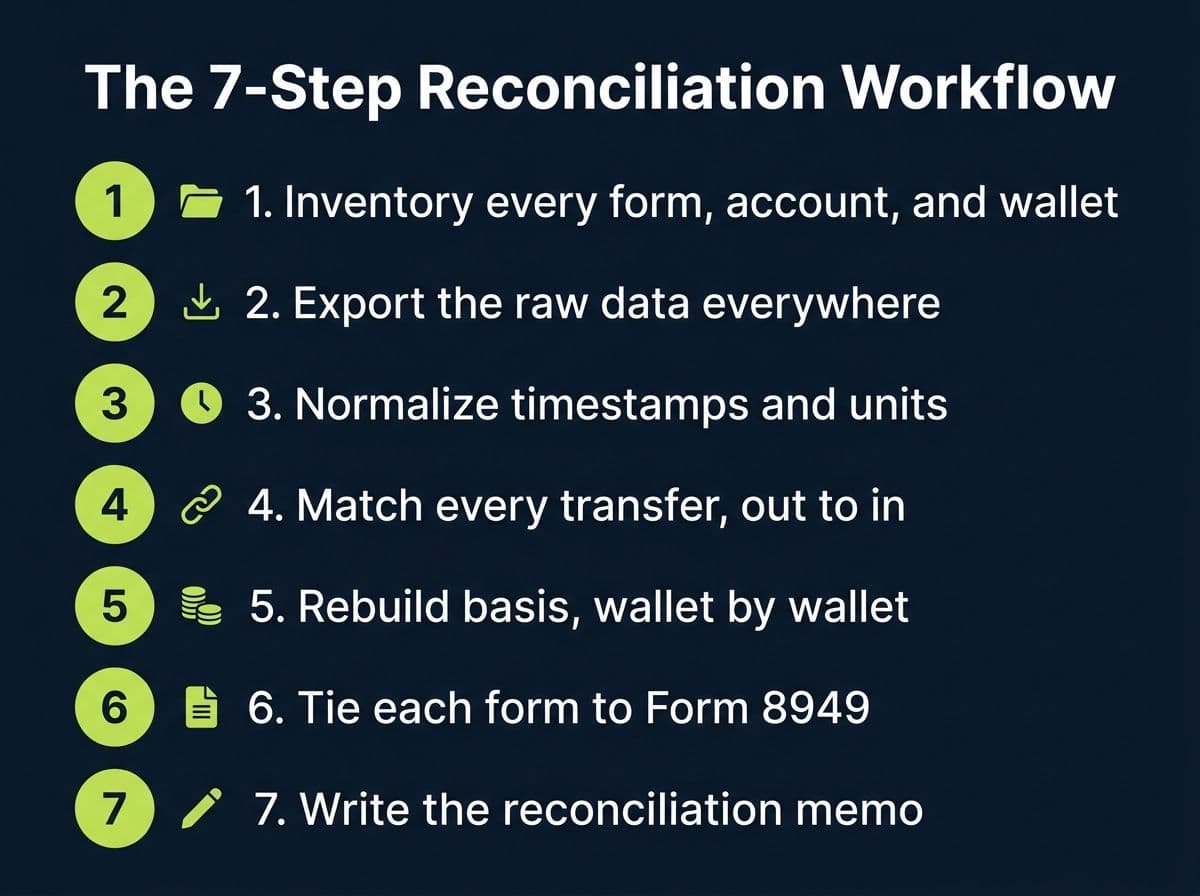

This is the process we run on every mismatched 1099-DA engagement. Run it in order; each step feeds the next.

Step 1: Inventory everything. Every 1099-DA received, every exchange account (active or dead), every wallet address you controlled during the year. Pull your IRS Wage and Income transcript to confirm you've seen every form the IRS has; forms mailed to old addresses count against you just the same.

Step 2: Export the raw data. Complete transaction histories from every platform, full activity for every wallet address from a block explorer. Raw exports, not the software's processed view. If a platform is gone, gather secondary evidence now: confirmation emails, bank and card statements showing fiat in and out, and on-chain records.

Step 3: Normalize timestamps and units. Convert everything to one time zone (the 1099-DA uses UTC-based reporting; your memories use local time), confirm year boundaries, and check unit quantities against Box 1c on each form. A sale recorded at 11:40 pm December 31 local time may be a January 1 transaction on the form, or vice versa.

Step 4: Match every transfer, out to in. For each withdrawal from any platform, find the matching deposit elsewhere, by transaction hash where possible, and link them in your software so it knows they're the same coins moving. Box 12 of your 1099-DA gives you the broker's view of what transferred in and when. When this step is done, there should be zero "deposits from nowhere" left in your data. Every unmatched arrival is a future phantom gain.

Step 5: Rebuild basis, wallet by wallet. With transfers linked, basis can finally travel with the coins. Apply your Revenue Procedure 2024-28 allocation for pre-2025 holdings, then confirm lot identification for each disposal under your chosen method, using your own records as Notice 2026-20 permits through 2026. This step turns a pile of matched transactions into defensible gain and loss numbers.

Step 6: Tie each form to the return. For every 1099-DA, trace Box 1f into your Form 8949 rows until the full proceeds amount is accounted for. Where the form's basis is blank or wrong, report your substantiated basis; when you're adjusting a reported figure, use the Form 8949 adjustment columns and codes (code B is the one for incorrect basis) so the IRS's computer can reconcile your return against the form without human intervention.

Step 7: Write the memo. One page: which records were used, how transfers were matched, how basis was established, why any proceeds differences exist, method and lot identification choices. Attach the workpapers and keep it seven years. If a notice ever arrives, this memo converts a months-long fight into a single documented response.

Pro Tip

Do steps 1 and 2 even for years you've already filed. Data disappears on the platforms' schedule, not yours, and the export you pull today is the evidence for the amendment or the notice response you might need in 2027.

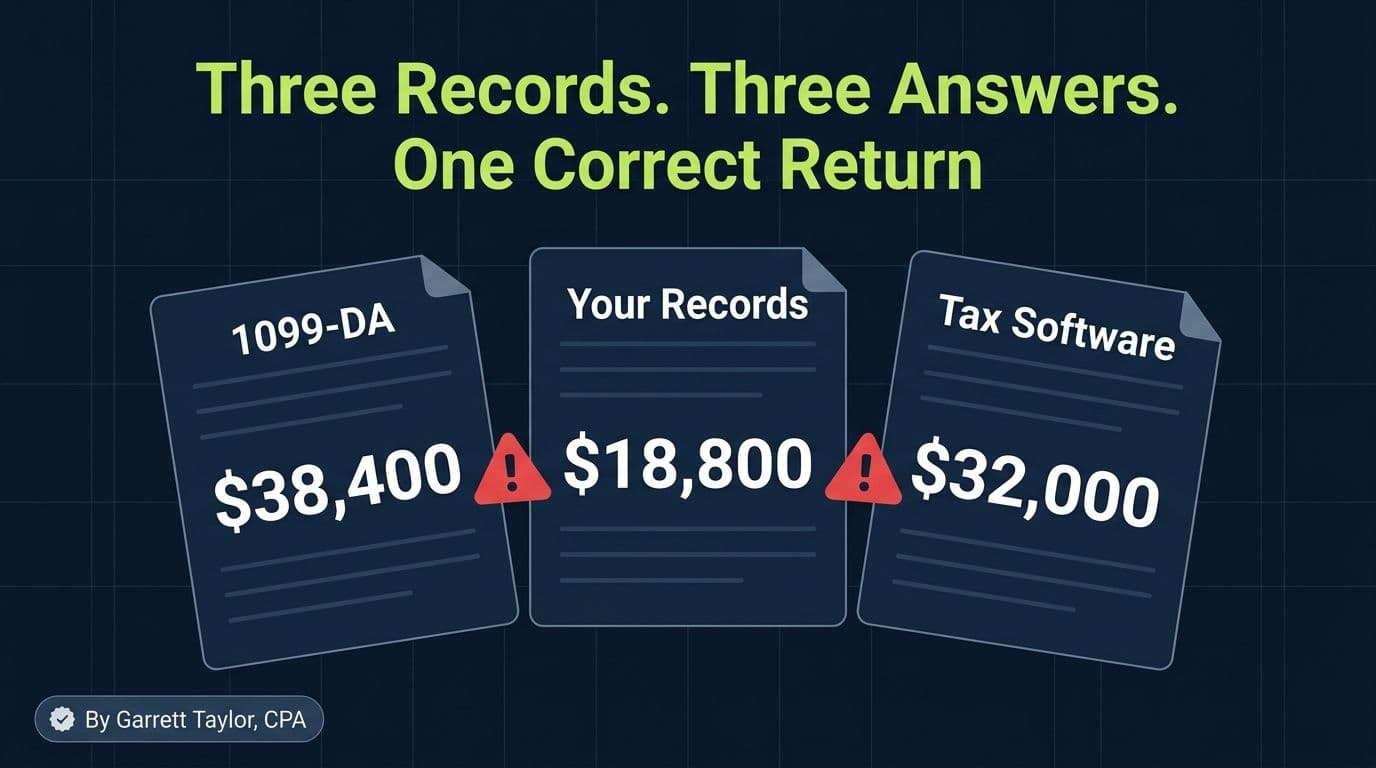

A Worked Example: Dev's Three Records, Reconciled

Abstract workflows hide the actual moves, so here's a complete reconciliation with real math.

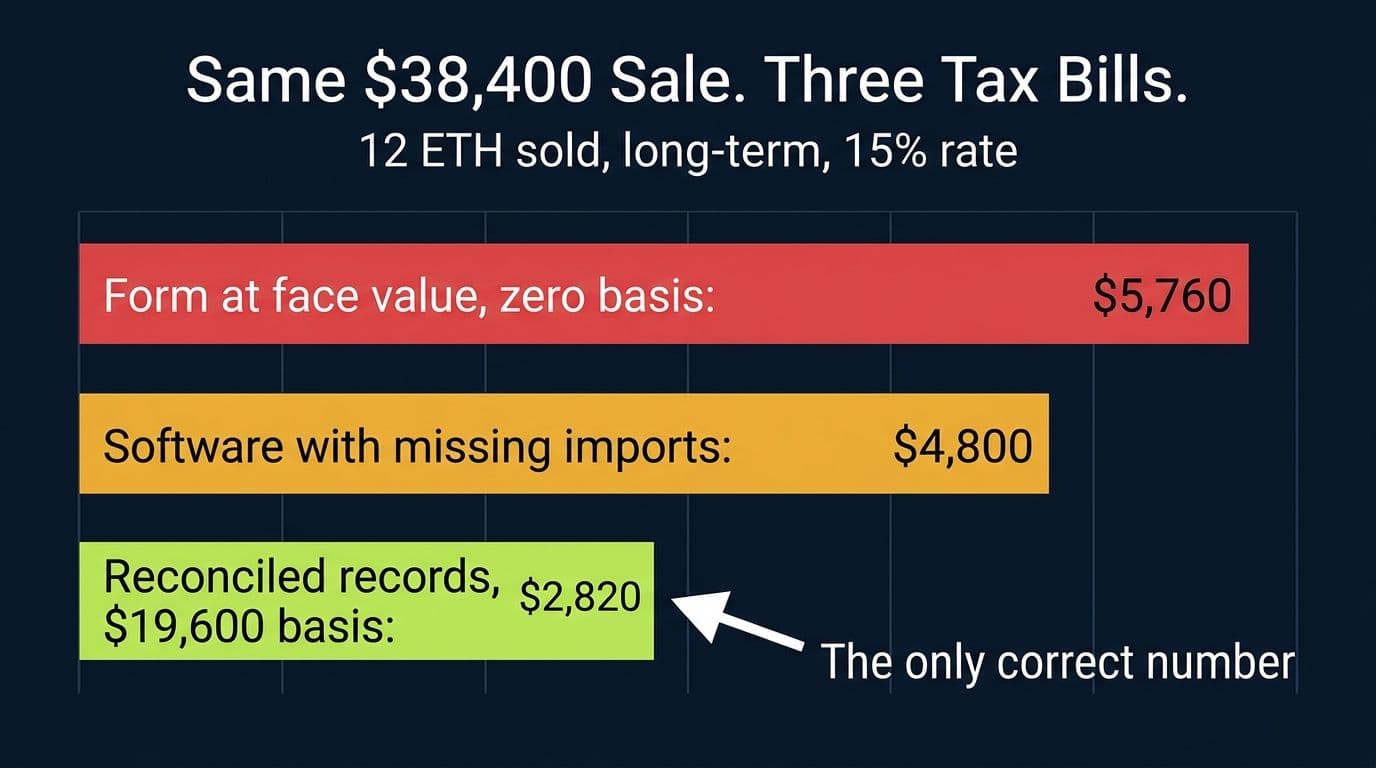

Dev's true history: Dev bought 12 ETH on Exchange A across three lots: 4 ETH at $1,200 each ($4,800) in 2022, 4 ETH at $1,600 each ($6,400) in early 2023, and 4 ETH at $2,100 each ($8,400) in late 2023. Total cost basis: $19,600. In 2024, Exchange A announced it was shutting down, so Dev withdrew all 12 ETH to a hardware wallet. In March 2025 he transferred the 12 ETH to Exchange B, and in November 2025 he sold all of it for $3,200 per ETH: $38,400 in proceeds, net of fees.

Record one, the 1099-DA from Exchange B: proceeds of $38,400 in Box 1f, 12 units in Box 1c, blank Box 1g, blank acquisition date, Box 9 checked (noncovered), and Boxes 12a and 12b showing 12 units transferred in on the March date. Face value of this record: $38,400 of gain.

Record two, the software: Dev connected Exchange B's API and his wallet address, but Exchange A no longer exists to connect, and he only ever manually entered one old lot (the 4 ETH at $1,600). The software sees 12 ETH arrive in the wallet from an address it doesn't recognize, matches basis for the 4 ETH it knows about, and assigns zero basis to the other 8. Software's output: proceeds $38,400, basis $6,400, gain $32,000, with a couple of yellow "missing purchase history" warnings Dev scrolled past.

Record three, Dev's documentation: the true numbers. Basis $19,600, all lots held over a year. Gain $18,800, long-term.

Three records, three answers. At Dev's income, long-term gains are taxed at 15%:

Same Sale, Three Records, Three Tax Bills

| Record | Basis Used | Reported Gain | Tax at 15% | Error vs Truth |

|---|---|---|---|---|

| 1099-DA at face value | $0 | $38,400 | $5,760 | Overpays $2,940 |

| Software output, as imported | $6,400 | $32,000 | $4,800 | Overpays $1,980 |

| Reconciled records | $19,600 | $18,800 | $2,820 | Correct |

The reconciliation, step by step. Dev inventories his accounts and realizes Exchange A's records are the missing link (Step 1). He digs up his old trade confirmation emails and his bank statements showing the three purchases totaling $19,600 (Step 2). Timestamps check out; unit counts match Box 1c (Step 3). He matches the chain: Exchange A withdrawal hash to hardware wallet deposit, wallet withdrawal hash to Exchange B deposit, which is the same transfer Exchange B's own form documents in Box 12 (Step 4). He enters the two missing lots into the software and links the transfers, which kills the zero-basis phantoms; all 12 ETH now carry basis from 2022 and 2023 (Step 5). Form 8949 shows the sale in the long-term, basis-not-reported section: proceeds $38,400, basis $19,600, gain $18,800, and every dollar of the 1099-DA's Box 1f is accounted for (Step 6). One page memo, workpapers attached, done (Step 7).

The IRS matching computer sees $38,400 of proceeds on the form and $38,400 on the return. Match. No notice, no letter, and $2,940 stays in Dev's pocket instead of subsidizing a data gap.

Three Records That Won't Agree?

Garrett reconciles 1099-DA forms against wallets, exchanges, and software output for a living, including platforms that no longer exist. Get the correct number, documented, filed.

Book a callWhat If You Genuinely Can't Reconstruct the Basis?

Sometimes the trail is truly cold: the exchange is gone, the emails are purged, the wallet was managed by an app that folded. You still have options, in descending order of strength.

Bank and card records. Fiat purchases leave marks. A $5,000 ACH to a crypto exchange in 2021 is powerful evidence of a $5,000 acquisition even when the exchange's own records are unreachable.

On-chain data plus historical prices. Public blockchains are permanent. If you can identify the deposit transaction that brought coins into your wallet, the date is provable, and a documented fair market value on that date supports a reasonable basis estimate. Courts and the IRS have long accepted reasonable reconstructions when records are unavailable through no fault of the taxpayer (the principle behind the Cohan rule), though estimates must be defensible and honest.

Partial documentation. Prove what you can lot by lot. Real basis on eight of twelve units beats surrendering to zero on all twelve.

Zero basis, as a last resort, on the units you truly cannot support. Painful but bulletproof: report the full proceeds as gain on those units. We use it as a scalpel on small unproveable slivers, never as a default for entire portfolios, because as Dev's table shows, defaulting to zero is the single most expensive filing decision in crypto.

What you should not do is invent a basis you can't support. An estimated basis with a documented method survives scrutiny; a number pulled from vibes does not, and the difference is obvious in an exam.

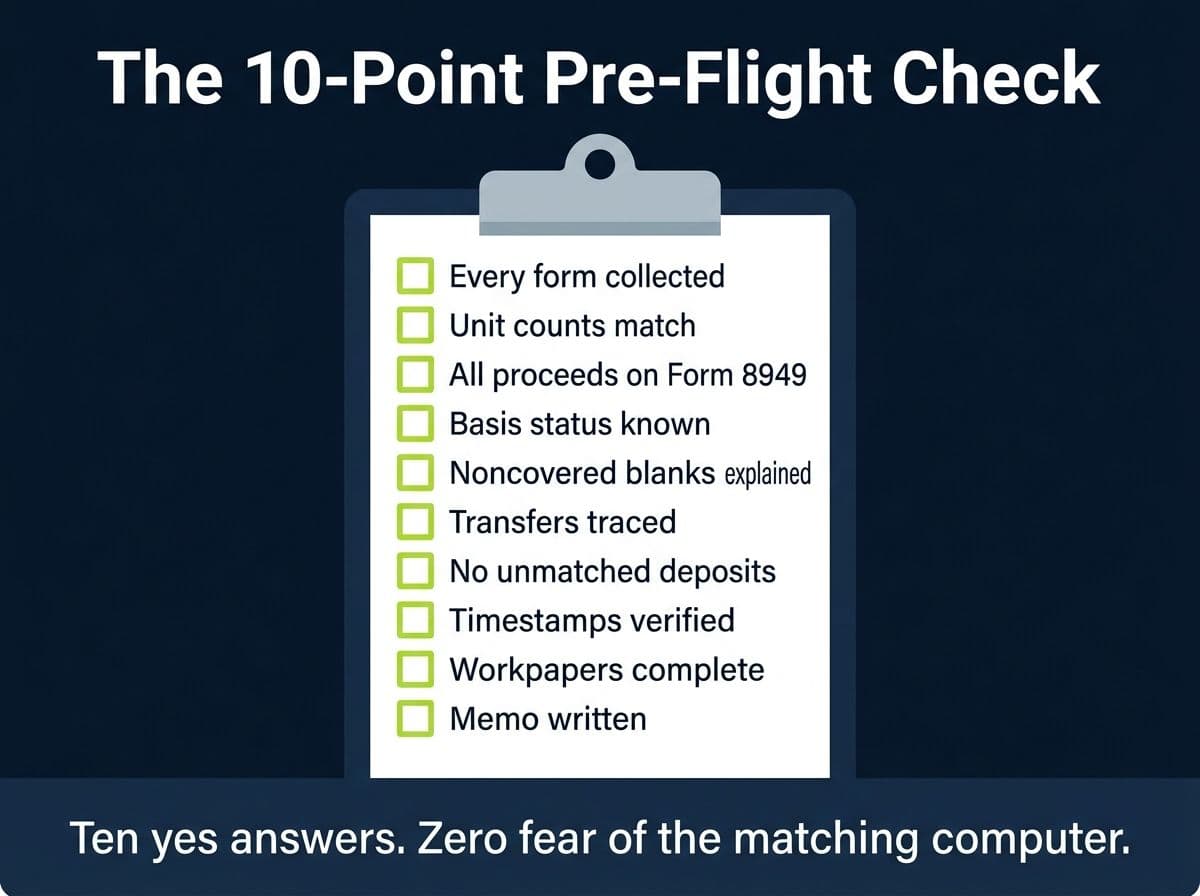

The 10-Point 1099-DA Pre-Flight Checklist

Before any return with a 1099-DA on it goes out the door, we run this list. Ten yes-or-no questions, two minutes each, and every "no" is a specific repair job from the sections above.

- Do I have every 1099-DA the IRS has? Check your Wage and Income transcript, not just your inbox. A 1099-DA mailed to an old address still counts against your return.

- Does Box 1c match my records? Unit counts are the fastest error detector on the whole form. If the 1099-DA says you sold 12 ETH and your history says 11.6, something (usually a fee or a missed transaction) needs explaining before anything else.

- Is every dollar of Box 1f visible on my Form 8949? Sum the proceeds across every 1099-DA and compare against the return. This is the exact comparison the IRS computer will run.

- Is Box 1g blank, zero, or populated, and do I know which? Blank means unreported (you supply basis). An actual zero means the broker reported zero basis to the IRS (dispute it if wrong). Populated means check the broker's FIFO math against your intended lots.

- Is Box 9 checked, and does that explain the other blanks? Noncovered status accounts for the missing acquisition date and holding period. It also means no corrected 1099-DA is coming, ever, so stop waiting for one.

- Do Boxes 12a and 12b line up with transfers I can trace? Every transfer-in the broker reported should match a withdrawal you can point to, with the basis story attached.

- Are there zero unmatched deposits left in my software? Any coins that still appear from nowhere are phantom gains waiting to be taxed.

- Do my short-term and long-term buckets survive a timestamp check? UTC reporting shifts year boundaries and holding periods. Verify the disposals within thirty days of January 1 and any lot near the one-year line.

- Can I hand a stranger my basis workpapers and have them re-derive my gain? If the answer is no, the documentation isn't done.

- Does the reconciliation memo exist? One page, written while you still remember why the numbers are what they are.

Ten yes answers means the three records agree, or disagree for reasons you can prove. That return doesn't fear the matching computer.

When Software Is Enough, and When You Need a CPA

The honest split, since we sell one side of it:

Software plus patience gets you there if: your platforms are all alive and importable, transfers match cleanly once linked, the 1099-DA differences trace to obvious causes like fees or FIFO defaults, and the dollars at stake are modest. The right software handles the mechanical 90% of reconciliation well when it's fed complete data.

Bring in a professional if: basis is missing on large disposals and the source platform is dead; software warnings ("missing purchase history," "zero-basis asset") cover material amounts; multiple forms overlap or contradict; DeFi, staking, or cross-chain activity muddies the transfer matching; you already filed on bad numbers and need an amendment or a notice response; or the gap between your three records is bigger than the cost of professional help. For scale: reconciliation engagements are exactly the work a crypto-specialized CPA exists for, and the fee is usually a fraction of a single phantom-gain overpayment.

The one thing not to do is file the mismatch and hope. The proceeds side is machine-checked, the basis side is yours to lose, and both failure modes have a price tag.

Get the Mismatch Fixed Before the IRS Notices

Flat-fee 1099-DA reconciliation: transfers matched, basis rebuilt and documented, Form 8949 tied to every form, return signed by a CPA.

Book a callFAQ: 1099-DA Mismatches and Reconciliation

Frequently Asked Questions

Why doesn't my 1099-DA match my crypto tax software?

Usually because the two see different data. The broker reports only activity on its own platform and rarely knows your cost basis, while the software knows only the accounts and wallets you imported. Missing imports, unmatched transfers, fee treatment, and FIFO defaults account for nearly all disagreements.

Which number do I use if my 1099-DA and my records disagree?

Account for the form's full proceeds on Form 8949, because the IRS matches that figure by computer, but use your documented basis, dates, and lot identification for the gain calculation. Your substantiated records override blanks or errors on the form, with adjustments shown through the Form 8949 codes.

Why is the cost basis blank or $0 on my 1099-DA?

Brokers weren't required to report basis for 2025 sales, and they can't report basis for noncovered assets: anything acquired before 2026 or transferred in from a wallet or another platform. Blank means unreported; an actual $0 entry means the broker told the IRS your basis was zero, which is worth disputing with the broker if wrong.

What is the three-record problem in crypto taxes?

It's the collision between the broker's 1099-DA, your own wallet and exchange history, and your tax software's output, three records built by different parties with different visibility. They routinely disagree on gains, and a correct return reconciles all three rather than copying any single one.

Will a 1099-DA mismatch trigger an audit?

Usually not an audit, but underreported proceeds reliably trigger a CP2000 notice from the IRS's automated matching system, typically 12 to 24 months after filing. The notice proposes tax on the full unmatched proceeds with no basis credit, plus a 20% accuracy penalty and interest, until you respond with documentation.

My software counted a wallet transfer as a sale. How do I fix it?

Link the withdrawal and deposit legs as a single transfer in the software, by transaction hash where possible, so the coins keep their original basis and holding period. Transfers between your own wallets and accounts are not taxable events, and Box 12 on the 1099-DA corroborates transfer-in activity.

Can I request a corrected 1099-DA?

Yes, for genuine errors like wrong proceeds, wrong units, or an incorrect $0 basis entry: contact the issuer listed in the form's filer box. But a blank basis on a noncovered asset isn't an error and won't be corrected; the broker doesn't have the data. Don't delay filing while you wait.

What if my exchange shut down and I can't get my purchase records?

Reconstruct from secondary evidence: bank and card statements showing purchases, confirmation emails, and on-chain data paired with historical prices. Documented, reasonable reconstructions are accepted practice. Report zero basis only for units you genuinely cannot support in any way.

Do I attach the 1099-DA to my tax return?

No. You report the transactions on Form 8949 and Schedule D and keep the form with your records. If box-level details need correction, the Form 8949 adjustment codes communicate that to the IRS; code B is the one for basis shown incorrectly on the form.

The proceeds on my 1099-DA are slightly different from my records. Does it matter?

Small differences usually trace to fees, UTC versus local-time year boundaries, or aggregated stablecoin reporting. Identify the cause, document it, and make sure the form's full proceeds are accounted for on your return. Explainable presentational differences with a matching bottom line are not a problem.

I already filed using the wrong numbers. What now?

If you overpaid because of zero-basis phantoms, amend within the refund window, generally three years, and collect your money. If you underreported proceeds, amend promptly before matching generates a CP2000. Our companion guide on what to do when a 1099-DA arrives covers the amend-or-wait decision in detail.

When should I hire a CPA instead of fixing it in software?

When material basis is missing and source platforms are gone, when software warnings cover significant amounts, when forms overlap or contradict, or when notices and amendments are already in play. If the disagreement between your three records exceeds the cost of professional reconciliation, the decision has made itself.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

I Got a 1099-DA, Now What? A CPA Walks Through Every Box (2026)

Form 1099-DA reports your crypto proceeds to the IRS, usually with no cost basis. A CPA explains every box, what to do before filing, and when to amend.

Crypto Cost Basis Methods: FIFO vs Specific ID vs HIFO

Compare FIFO, LIFO, HIFO, and Specific ID for crypto taxes. Worked example shows how the same sale produces 4 different tax bills. Updated for Rev. Proc. 2024-28 and 1099-DA.

IRS Crypto Tax Notices: What to Do If You Get One

Got an IRS crypto notice? Learn exactly how to respond to CP2000, Letter 6173, and Letter 6174 notices. Step-by-step response guide from a crypto tax CPA.