I Got a 1099-DA, Now What? A CPA Walks Through Every Box (2026)

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Form 1099-DA is the new broker form for digital assets. The first wave, covering 2025 transactions, landed in early 2026, and the IRS receives a copy of every single one.

- ✓For 2025 sales, brokers were only required to report gross proceeds. Cost basis reporting was voluntary, so most forms show a blank or zero basis box even when you paid real money for the crypto.

- ✓A blank Box 1g does not mean your basis is zero. It means the broker doesn't know it. If you file without supplying basis, you overpay, sometimes dramatically.

- ✓The IRS matches Box 1f proceeds against your Form 8949. Report less than the forms show and the automated CP2000 system flags the gap, usually 12 to 24 months after you file.

- ✓If you already filed and the 1099-DA reveals unreported sales, amend with Form 1040-X before the IRS writes first. If you reported everything accurately, you generally do not need to amend just because a late form arrived.

Pro Tip

Written by Garrett Taylor, CPA (License #133092). Reviewed by Leanne Grant, EA (#00167954-EA). Last updated: July 9, 2026.

Quick answer: Form 1099-DA reports the gross proceeds from your digital asset sales to you and to the IRS. It usually does not report your cost basis, which means the form alone makes every sale look like pure profit. Your job before filing: verify the proceeds, supply the basis from your own records, and report each transaction on Form 8949 and Schedule D. If you already filed without it, you may need to amend with Form 1040-X, but not always. This guide walks through every box on the form, a complete worked example, and the exact already-filed decision tree.

The envelope looks official because it is. Form 1099-DA, Digital Asset Proceeds From Broker Transactions, is the first tax form in history built specifically for crypto, and if one showed up in your mailbox or your exchange's tax center, the IRS has an identical copy sitting in its matching system right now.

Here's the uncomfortable part: the form was mailed to millions of people who have no idea what to do with it. It lists proceeds that look terrifyingly large, a cost basis box that's probably empty, and a checkbox layout that even seasoned tax pros had to learn from scratch this year.

We prepare crypto tax returns all day, every day, and since January the single most common message we get starts the same way: "I got a 1099-DA, now what?"

So let's answer it properly. Box by box, decision by decision, with real math.

What Is Form 1099-DA and Why Did You Get One?

Form 1099-DA is the digital asset equivalent of the 1099-B that stock brokerages have sent for decades. Under final regulations the Treasury issued in 2024, brokers that take custody of digital assets (centralized exchanges, hosted wallet providers, payment processors, some crypto ATMs) must report your disposals to the IRS.

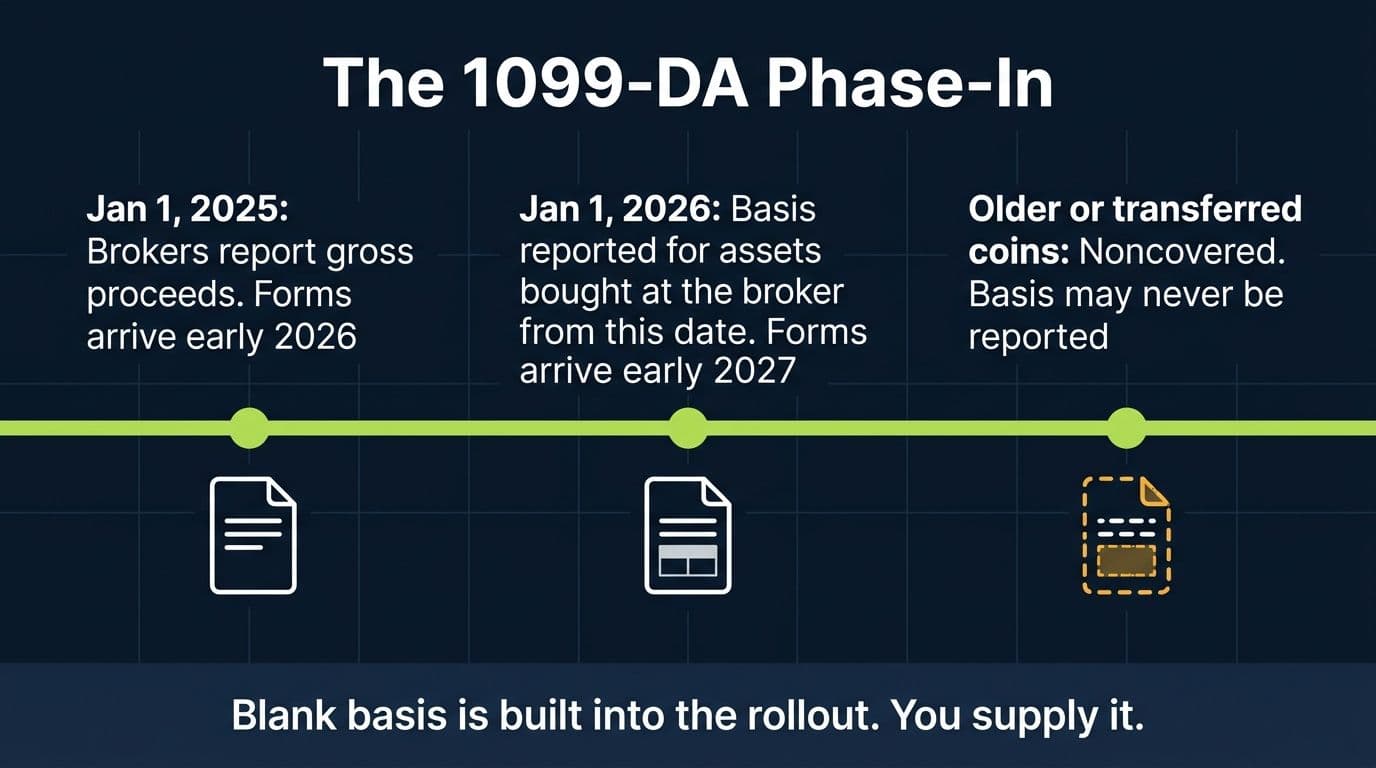

The rollout has a specific timeline, and knowing where you are on it explains most of what's confusing about your form:

- Sales on or after January 1, 2025: brokers report gross proceeds. These forms arrived in early 2026, due to recipients by mid-February. This is the wave you're holding.

- Assets acquired on or after January 1, 2026 (and sold through the same custodial broker): brokers must also report cost basis. Those forms arrive in early 2027.

- Anything acquired before 2026, or transferred into the broker from elsewhere: treated as a "noncovered" asset. The broker reports the sale but is not required to report basis, possibly ever.

You got a 1099-DA because at some point in 2025 you sold, traded, spent, or otherwise disposed of a digital asset through a U.S. custodial broker. That includes some things people don't think of as "selling": swapping ETH for SOL, converting crypto to a stablecoin, spending bitcoin through a payment processor, or paying trading fees in crypto. Per the IRS's own explanation of the form, any disposal for cash, other digital assets, property, goods, or services can trigger reporting.

Two groups notably do not send the form. Foreign exchanges without U.S. reporting obligations generally issue nothing (your tax obligation is unchanged; the paperwork just doesn't exist). And decentralized protocols don't either: Congress repealed the so-called DeFi broker rule in April 2025 under the Congressional Review Act, so self-custody wallets and DEX front-ends stay outside the 1099-DA system entirely.

January 1, 2025

The date the 1099-DA era started. Every disposal through a U.S. custodial broker from that day forward generates a report to the IRS, whether or not you ever see the form.

Will Everyone Get a 1099-DA?

No, and the gaps matter as much as the forms.

You should have received a 1099-DA if you disposed of digital assets in 2025 through a U.S. centralized exchange or another custodial broker. One broker may issue one consolidated form or many separate ones, and if you used four exchanges, you're reconciling four brokers' worth of paper.

You likely received nothing if your 2025 activity was self-custody only, DeFi only, on foreign platforms, or you bought and held without disposing of anything. Buying crypto with dollars and holding it is not a reportable disposal, and neither is moving your own coins between your own wallets (though transfers create their own problems we'll get to).

Two special cases from the form's own rules are worth knowing:

- Stablecoins: brokers can use an optional aggregate method. If your total qualifying stablecoin sales stayed at or under $10,000 for the year, the broker may not report them at all. Above that, they can appear as one aggregated line with a checkbox in Box 11a.

- NFTs: same idea with a $600 aggregate threshold for specified NFTs.

Here's the trap in all of this: no form does not mean no taxes. The IRS has been explicit that all digital asset income is reportable whether or not a 1099-DA exists. The form changes what the IRS can see, not what you owe. If you're reading this because you got one form from Coinbase but traded on three other platforms, your return still needs all four.

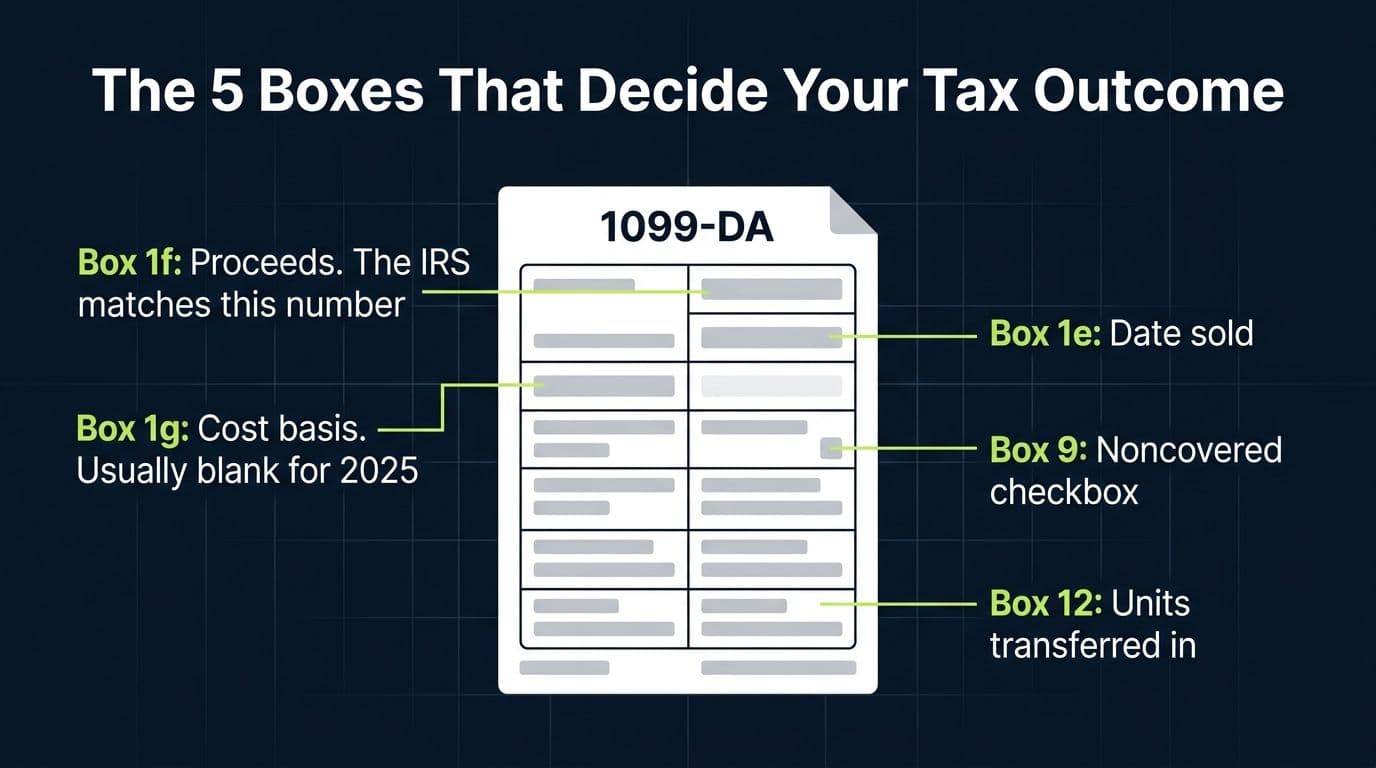

The Box-by-Box Walkthrough: What Every Field on Your 1099-DA Means

Put the form in front of you. Here's what you're looking at, based on the official 2025 form and instructions.

Form 1099-DA, Box by Box (2025 Form)

| Box | What It Shows | What to Watch For |

|---|---|---|

| 1a, 1b | Code and name of the digital asset | One form or section per asset |

| 1c | Number of units disposed | Verify against your own history |

| 1d | Date acquired | Often blank for noncovered assets |

| 1e | Date sold or disposed | Drives short-term vs long-term |

| 1f | Proceeds | The number the IRS matches against your return |

| 1g | Cost or other basis | Usually blank for 2025. Blank means unknown, not zero |

| 1h, 1i | Accrued market discount, wash sale loss | Rarely apply; wash sale box is only for digital assets that are also securities |

| 2 | Basis reported to IRS checkbox | Checked only if 1g actually went to the IRS |

| 4 | Federal tax withheld | Backup withholding; almost always zero for 2025 |

| 6 | Short-term, long-term, or ordinary | Often blank when Box 9 is checked |

| 8 | Broker relied on your acquisition info | Relevant if you gave the broker lot details |

| 9 | Noncovered asset checkbox | The single most important checkbox on the form |

| 11a to 11c | Aggregate stablecoin or NFT reporting | One line may represent hundreds of trades |

| 12a, 12b | Units transferred in, and when | The paper trail of your deposits |

| 14 to 16 | State reporting | A few states get their own copy |

Let's slow down on the boxes that actually decide your tax outcome.

Box 1f, Proceeds, is the number that can hurt you. This is what the broker says you received, and it's the figure the IRS's document-matching system compares against your Form 8949. Your first reconciliation job is simple: does every dollar of Box 1f appear on your return?

Box 1g, Cost or other basis, is the number that can save you. When it's filled in, check it carefully (brokers use FIFO by default, which may not match your intended lots). When it's blank, and for 2025 forms it usually is, the entire burden of proving what you paid shifts to you. One subtle rule from the instructions: any entry in Box 1g, including zero, means basis was actually reported to the IRS. A true zero is different from a blank, and both are different from your real basis.

Box 9, the noncovered checkbox, explains most blank boxes. If it's checked, the asset was acquired before 2026 or arrived at the broker by transfer, and the broker had no obligation to track or report basis, acquisition date, or holding period. Boxes 1d, 1g, and 6 going blank together with Box 9 checked is the signature pattern of the 2026 filing season.

Boxes 12a and 12b quietly document your transfers. Units transferred in and the transfer date. That's the broker telling the IRS "these coins came from somewhere else." It's also your reminder that the basis lives wherever those coins actually originated, which is exactly the reconciliation problem that deserves its own guide.

And one reassuring note: Box 1i, wash sale loss disallowed, almost never applies to crypto. The wash sale statute covers stock and securities, and under current law that doesn't include ordinary digital assets. The box exists for edge cases like tokenized securities. If you sold at a loss and rebought, that loss generally still counts (see our full breakdown of crypto wash sale rules).

Why Is the Cost Basis Blank on My 1099-DA?

Because for the 2025 tax year, the rules practically guaranteed it. Three reasons stack on top of each other:

Reason one: basis reporting wasn't required yet. For 2025 sales, brokers had to report gross proceeds; basis was voluntary. Most brokers reported the minimum.

Reason two: your coins are noncovered. Basis reporting, even when it becomes mandatory in 2026, only covers assets you acquired at that broker on or after January 1, 2026 and kept there. Every coin you bought before 2026 is noncovered indefinitely. The first fully-populated 1099-DA forms won't be common for years.

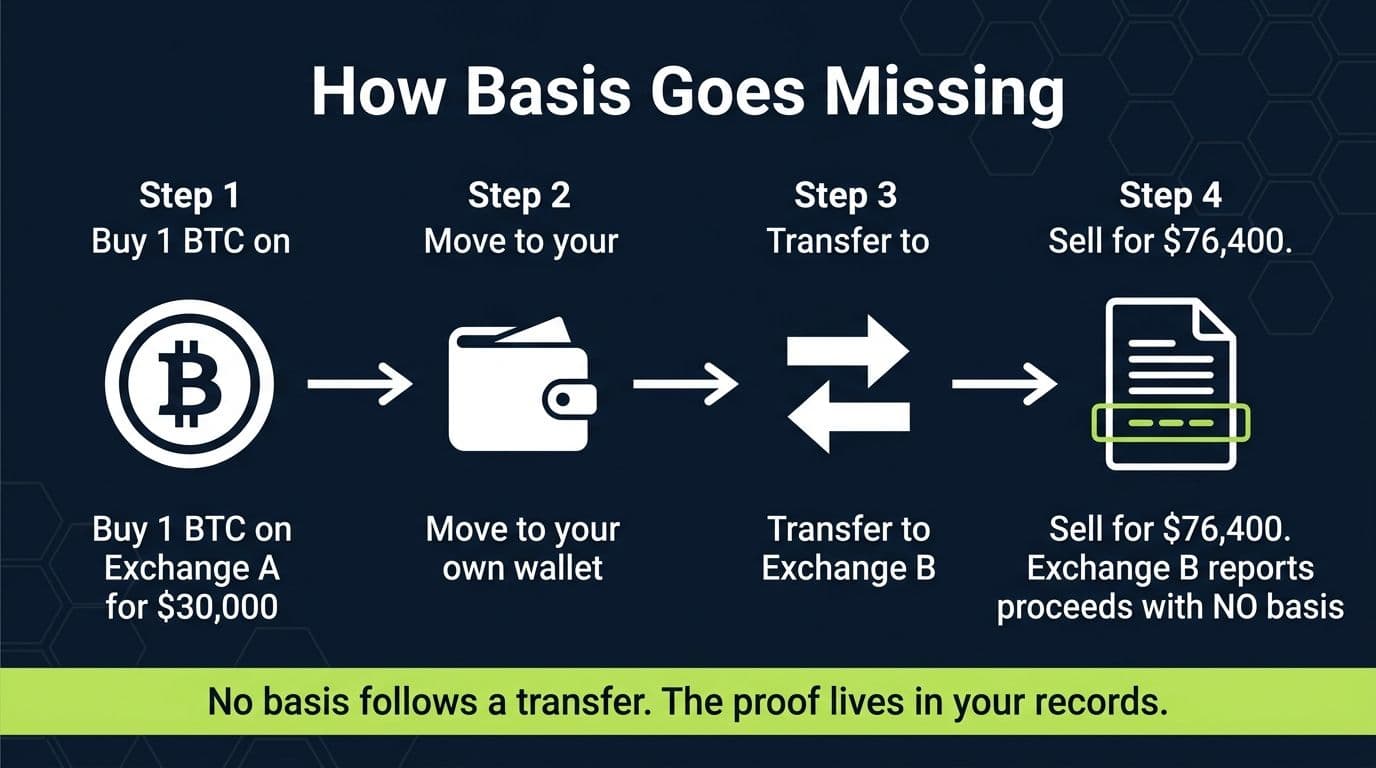

Reason three: transfers destroy basis visibility. When you move coins from a wallet or another exchange into a broker, the broker sees units arrive with no price tag attached. There is no basis-sharing system between crypto platforms the way there is between stock brokerages. Deposit 2 BTC you bought elsewhere in 2021 and sell them in 2025, and the broker can truthfully report only one number: what you sold them for.

The result is a form that systematically overstates your gain if taken at face value. A blank basis box is not the IRS claiming you owe tax on the full proceeds. It's an unfinished sentence you're expected to complete. Complete it with documentation and you're fine. Leave it blank and you pay tax on money you never made; that failure mode is common enough that we wrote a dedicated reconciliation guide for it.

“The most expensive number on a 1099-DA is the one that isn't there. People see a big proceeds figure, an empty basis box, and assume the IRS's version wins. Your documented basis is just as legitimate as the broker's proceeds. You're allowed to finish the math.”

, Leanne Grant, EA

Does a 1099-DA Mean I Owe Taxes?

Not by itself. The form reports proceeds, and proceeds are not profit.

Tax is owed on gain: proceeds minus cost basis. Sell $40,000 of ETH you bought for $45,000 and your 1099-DA shows $40,000 of proceeds while your return shows a $5,000 loss that reduces your taxes. The form and the outcome point in opposite directions, and both are correct.

Whether you owe also depends on holding period (long-term rates of 0%, 15%, or 20% versus short-term at ordinary rates), your other income, and prior capital loss carryforwards. Which cost basis method you use to identify the lots you sold matters too, and it changed meaningfully in 2025; our guide to crypto cost basis methods covers FIFO, specific identification, and the wallet-by-wallet rules now in force.

So treat the 1099-DA as what it is: one input. An important one, because the IRS has it too, but an input.

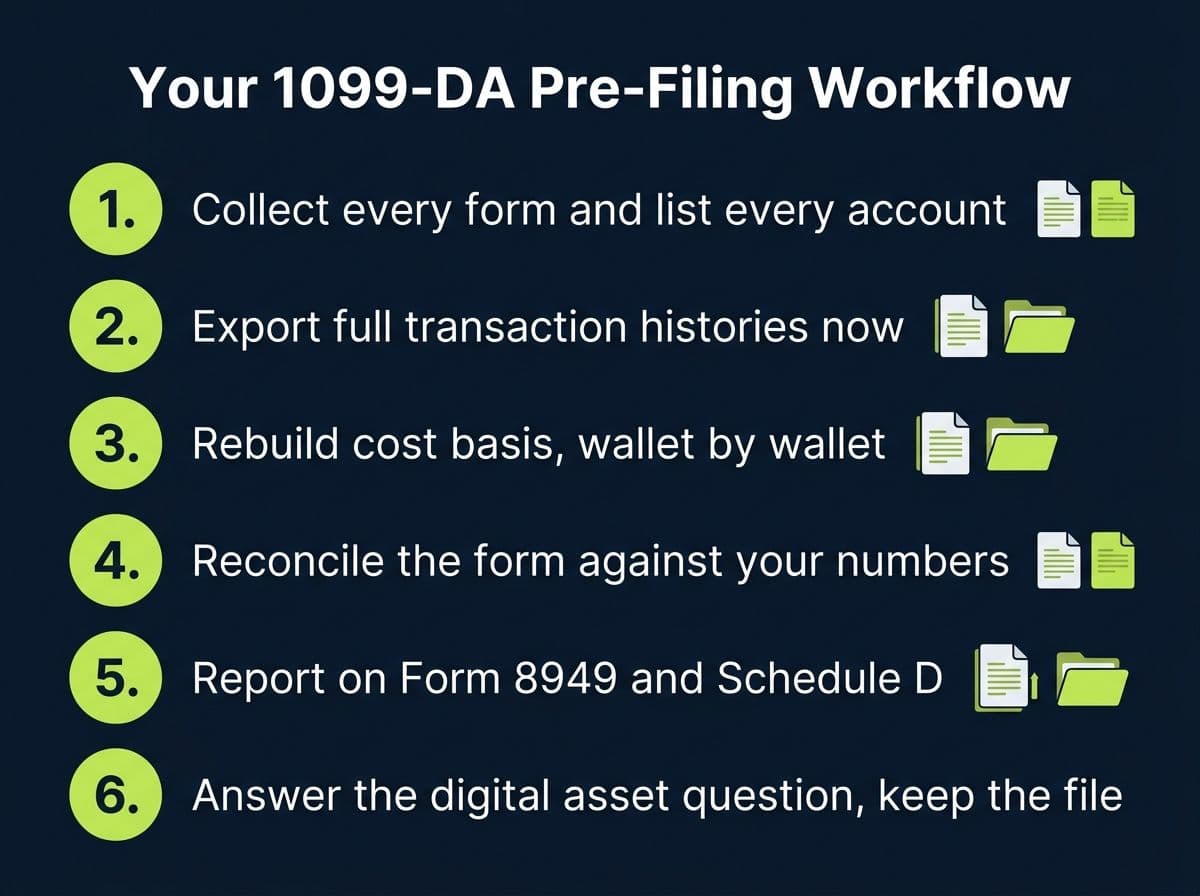

What to Do With Your 1099-DA Before You File: A 6-Step Workflow

Here's the process we run on every 1099-DA that comes through our office. It works whether you have one form or nine.

Step 1: Collect every form and inventory every account. Check the tax section of every exchange you touched in 2025, not just the ones that emailed you. Then list every platform and wallet you used, form or no form. Your return covers all of them; the forms cover some of them.

Step 2: Export complete transaction histories. Full history from each exchange, plus wallet activity for self-custody. Do this now: platforms change export formats, delist users, and bury old data. If an exchange you used has shut down, start reconstructing from emails, bank records, and blockchain explorers immediately.

Step 3: Rebuild your cost basis. For each disposal on each 1099-DA, determine what you actually paid, including fees, and when. Since January 1, 2025, basis must be tracked wallet by wallet, not in one universal pool; if you held crypto before then, Revenue Procedure 2024-28 governed how your old pooled basis got allocated to each wallet or account. And under Notice 2026-20, through the end of 2026 you can make specific identification of the units you sold using your own books and records, because most brokers still can't accept lot-level instructions. Translation: your documentation carries real legal weight right now. Build it.

Step 4: Reconcile the form against your numbers. Does Box 1f match the proceeds your records show, net of the fee treatment the broker used? Do the unit counts in Box 1c match? If Box 1g is populated, does the broker's FIFO math match the lots you intended to sell? Discrepancies here are extremely common and fixable; they're the entire subject of our three-record mismatch guide.

Step 5: Report on Form 8949 and Schedule D. Each disposal (or properly grouped summary) goes on Form 8949, which flows to Schedule D. The "applicable checkbox on Form 8949" field near the top of your 1099-DA tells you which part and box to use, depending on whether basis was reported to the IRS. When the form's numbers need correction, you don't ignore the form; you report it and adjust with the adjustment columns and codes on Form 8949 (code B covers incorrect basis) so the IRS computer can follow your math.

Step 6: Answer the digital asset question and keep the file. The Form 1040 digital asset question gets a Yes. Keep the 1099-DA, your exports, your basis workpapers, and your lot identification records together for at least seven years. If the IRS ever asks, this file is the difference between a five-minute reply and a five-month ordeal.

Pro Tip

Before you file, pull your IRS Wage and Income transcript (free at irs.gov). It shows every information return the IRS has under your Social Security number, including 1099-DA forms you never received because of an old address or a dead email account. Matching against the IRS's actual list beats guessing.

A Worked Example: Maya's Blank-Basis Bitcoin Sale

Numbers make this concrete. Meet Maya: single filer, $95,000 salary, a long-term crypto holder rather than a trader.

Her history: in March 2021, Maya bought 1.0 BTC on Exchange A for $30,000, fees included. In 2023 she moved it to a hardware wallet. In June 2025 she transferred 0.8 BTC to Exchange B, and in December 2025 she sold all 0.8 BTC for $76,400 net of fees.

What arrives in February 2026: a 1099-DA from Exchange B showing:

Maya's 1099-DA (What Exchange B Reported)

| Box | Entry | Meaning |

|---|---|---|

| 1a to 1c | BTC, 0.8 units | The asset and quantity sold |

| 1d, Date acquired | Blank | Exchange B has no idea |

| 1e, Date sold | 12/15/2025 | The December sale |

| 1f, Proceeds | $76,400 | Reported to the IRS |

| 1g, Cost basis | Blank | Not reported, not zero |

| 6, Gain or loss character | Blank | Unknown to the broker |

| 9, Noncovered | Checked | Transferred-in asset |

| 12a, 12b | 0.8 units, 06/10/2025 | Her June transfer, on the record |

Exchange A reported nothing (she disposed of nothing there), and her hardware wallet is invisible to the reporting system. So the IRS's complete picture of Maya is one number: $76,400 of proceeds.

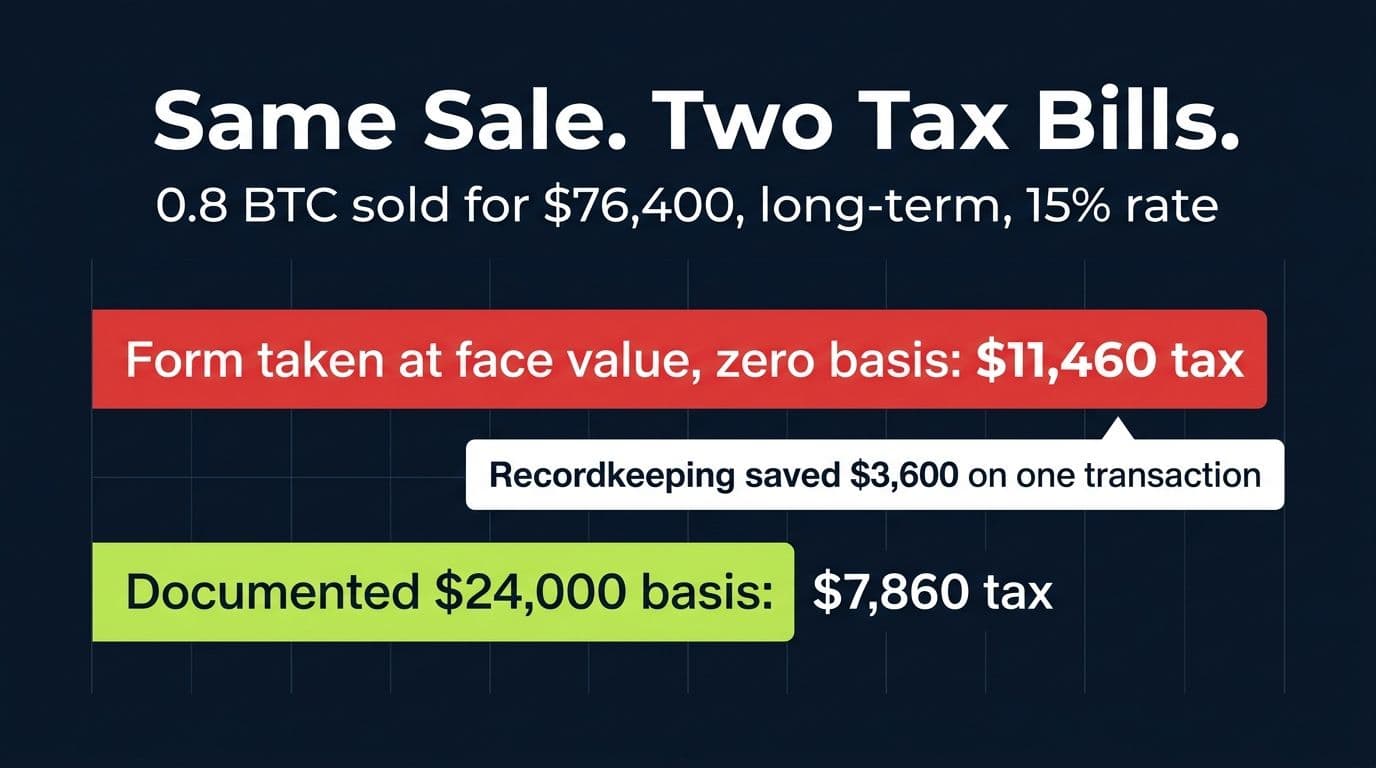

The wrong way to file: Maya assumes the form is the whole story, reports $76,400 of proceeds with zero basis, and treats it as gain. At her income, long-term capital gains are taxed at 15%. Tax on the sale: $11,460.

The right way to file: Maya's basis in the 0.8 BTC is 0.8 x $30,000 = $24,000, documented by her 2021 purchase confirmation from Exchange A and the transfer trail (which Box 12 of the form itself corroborates). Her acquisition date makes the gain long-term.

- Proceeds: $76,400

- Basis: $24,000

- Long-term capital gain: $52,400

- Tax at 15%: $7,860

Same sale, same form, $3,600 of difference, purchased entirely with recordkeeping. On Form 8949 she reports the sale in the long-term section for basis not reported to the IRS, proceeds $76,400, basis $24,000, gain $52,400. The IRS matches Box 1f, finds all $76,400 accounted for, and the return sails through with her gain calculated correctly.

Notice what did the work: Maya could prove the $30,000 purchase. If Exchange A had vanished and taken her purchase history with it, she'd be reconstructing basis from bank statements and blockchain data, which is exactly the situation covered in our reconciliation guide.

Holding a 1099-DA With a Blank Basis Box?

Garrett rebuilds cost basis across exchanges, wallets, and dead platforms, then files the return with documentation that survives IRS matching. Flat-fee, CPA-signed.

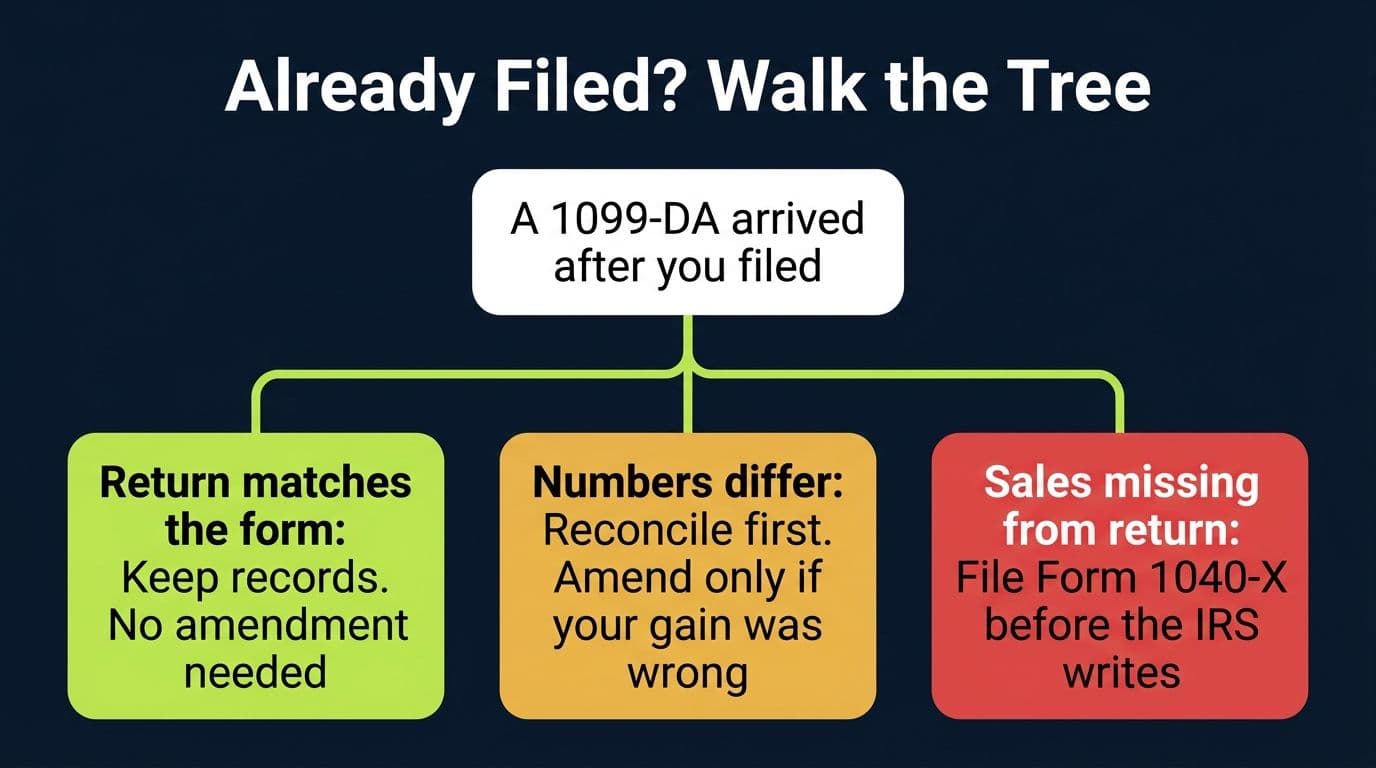

Book a callI Already Filed My Taxes. Am I at Risk? Do I Need to Amend?

This is the other half of the panic, and the answer depends entirely on which of three situations you're in. Walk the tree honestly.

Situation one: you reported all your crypto activity accurately, and the late-arriving 1099-DA matches your return. You're fine. There is no rule requiring you to amend just because a form showed up after you filed. Staple the form to your records and move on. This includes the case where the form shows blank basis and your return shows real basis: your return is the complete document, the form never claimed to be.

Situation two: the form's proceeds don't quite match what you reported. Maybe fees were treated differently, maybe the broker's totals include a transaction you booked in a different year because of timestamp differences. Don't reflexively amend. First reconcile: figure out exactly why the numbers differ and whether your return's bottom line (the gain or loss) is actually right. If your gain was correct and the difference is presentational, document the reconciliation and hold it in case the IRS asks. If your gain was wrong, amend. Our mismatch guide walks through this diagnosis step by step.

Situation three: the 1099-DA reveals sales you never reported at all. Maybe you forgot an account, maybe you didn't know a crypto-to-crypto swap was taxable. This is the one where you act. File Form 1040-X, which can now be e-filed for recent years, report the missing transactions with their real basis, and pay the additional tax plus interest.

Why amend proactively instead of waiting to see if the IRS notices? Cold math:

- The IRS will notice. Document matching is automated. Box 1f from every 1099-DA gets compared to your Form 8949 totals by computer, and unexplained gaps generate a CP2000 notice, typically 12 to 24 months after filing.

- The CP2000 math is the worst-case version. The automated system knows your proceeds and not your basis, so it proposes tax on the full amount, plus an accuracy-related penalty of 20% of the underpayment, plus interest that has been compounding the whole time.

- A voluntary amendment reframes everything. You calculate the real gain with real basis, penalties are frequently avoided or reduced when you self-correct before contact, and you cut off the interest clock at the amendment date.

One deadline to know: refunds have a statute of limitations (generally three years from your original filing deadline), but there's no deadline for amending to report more income. Sooner is strictly better; every month of delay is another month of interest, and amending after the IRS's letter arrives loses you most of the credibility benefit.

Pro Tip

If you receive a CP2000 before you get around to amending, do not file a 1040-X in parallel and do not panic-pay the proposed amount. The CP2000 proposes tax on proceeds without your basis, which is almost always overstated. Respond to the notice itself with corrected figures and documentation. The proposed amount is an opening position, not a bill.

What Happens If You Ignore a 1099-DA?

Nothing, for a while. That's what makes it dangerous.

Your return gets accepted, your refund arrives, and the matching happens quietly in the background over the following year or two. Then the CP2000 notice shows up: proposed additional tax computed from the unreported proceeds, penalty, interest, and a response deadline. It isn't an audit and it isn't a bill yet, but it must be answered, with documentation, on the IRS's timeline. Ignore that too and it hardens into an assessment, followed by collections.

The pattern is familiar to anyone who remembers what happened when exchanges sent 1099-K forms years ago: taxpayers received IRS letters proposing absurd tax bills computed from gross proceeds with zero basis. The 1099-DA system is that, industrialized. The IRS also now has a dedicated digital asset question on every 1040, years of John Doe summons data from major exchanges, and a purpose-built form feeding the matching engine.

If you've already received an IRS letter about crypto, whether a CP2000 or one of the softer education letters, move deliberately: our guide to responding to IRS crypto notices covers each letter type and the response strategy for it.

When to Bring In a Crypto CPA

Honest triage, because plenty of 1099-DA situations are DIY-able.

Handle it yourself if: you used one or two exchanges, never self-transferred significant amounts, have complete purchase records, and your form's proceeds reconcile to your history within rounding. Good software plus care gets you there; see our crypto tax software roundup for what actually works.

Get professional help if: basis is blank on large disposals and your acquisition records are incomplete; you moved coins across many wallets or through platforms that no longer exist; multiple 1099-DA forms overlap or contradict your own numbers; you already filed and the amendment math is scary; or a notice has already arrived. This is also the moment to be choosy about who you hire; here's how to vet a crypto CPA and what it should cost.

The economics usually decide it. In Maya's example, documentation was worth $3,600 on a single sale. Multiply by a real portfolio, add penalty exposure if it's handled wrong, and the fee for getting it professionally reconciled is small against the spread.

Turn Your 1099-DA Into a Filed, Defensible Return

Bring the forms and whatever records you have. Garrett reconciles proceeds, rebuilds basis, handles amendments when needed, and signs the return as your CPA.

Book a callFAQ: Form 1099-DA

Frequently Asked Questions

What is a 1099-DA for?

Form 1099-DA reports proceeds from digital asset sales and exchanges made through a custodial broker to you and to the IRS. Starting with 2025 transactions, U.S. exchanges and other custodial brokers must file it for each customer who disposed of digital assets, giving the IRS direct visibility into crypto sales for the first time.

Do I have to claim a 1099-DA on my taxes?

Yes. Every disposal shown on the form must be reported on your return, normally on Form 8949 and Schedule D. The IRS receives its own copy and matches the proceeds against what you file, so leaving the form off your return triggers automated underreporter notices.

Will everyone get a 1099-DA?

No. Only customers of U.S. custodial brokers who disposed of digital assets receive one. Buy-and-hold investors, self-custody and DeFi users, and customers of most foreign exchanges generally get nothing. All taxable activity must be reported either way; the form changes what the IRS sees, not what you owe.

Does a 1099-DA mean I owe taxes?

Not by itself. The form reports gross proceeds, and tax is owed only on gain: proceeds minus your cost basis. Depending on what you paid, holding period, and your other income, a large proceeds number can produce a small gain, no gain, or a deductible loss.

Why is the cost basis blank on my 1099-DA?

For 2025 sales, brokers were required to report proceeds but not basis. Basis is also permanently missing for noncovered assets, meaning anything acquired before 2026 or transferred into the broker from a wallet or another platform. A blank basis box means the broker doesn't know what you paid, and you must supply it from your own records.

How do I report a 1099-DA on my tax return?

Report each disposal on Form 8949, using the part and checkbox indicated near the top of the 1099-DA, then carry the totals to Schedule D. Where the form's data is incomplete or wrong, report your correct basis and use the Form 8949 adjustment codes rather than ignoring the form. Also answer Yes to the digital asset question on Form 1040.

What happens if I don't report a 1099-DA?

The IRS matches the form's proceeds against your return by computer. An unexplained gap typically produces a CP2000 notice 12 to 24 months later proposing tax on the full proceeds with no basis credit, plus a 20% accuracy-related penalty and interest. Responding with real numbers usually shrinks it, but prevention is far cheaper.

I already filed my taxes and then got a 1099-DA. Do I need to amend?

Only if your return is actually wrong. If you reported all your crypto activity accurately, a late-arriving form that matches your return requires nothing. If the form reveals unreported sales or a materially wrong gain, file Form 1040-X promptly with correct basis, before IRS matching generates a notice.

Is a 1099-DA just informational?

Treat it as enforceable, not informational. The IRS copy feeds a matching system that compares broker-reported proceeds to your Form 8949. The basis side may be incomplete, but the proceeds side is actively checked, and mismatches generate notices.

Does the IRS get a copy of my 1099-DA?

Yes, every one. Brokers file the same form with the IRS that they send you, including state copies where applicable. You can see everything filed under your Social Security number by pulling your Wage and Income transcript from the IRS.

Do foreign crypto exchanges send 1099-DA forms?

Generally not for 2025, since the current requirements apply to U.S. brokers. You must still report all activity on foreign platforms yourself, and significant foreign accounts can carry separate FBAR or FATCA disclosure obligations worth reviewing with a professional.

Does my 1099-DA account for wash sales?

Almost never, and for most crypto it doesn't need to. The wash sale rule currently applies to stock and securities, which ordinary digital assets are not, so crypto losses generally survive a quick rebuy. The form's wash sale box exists for digital assets that also qualify as securities, a rare case.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

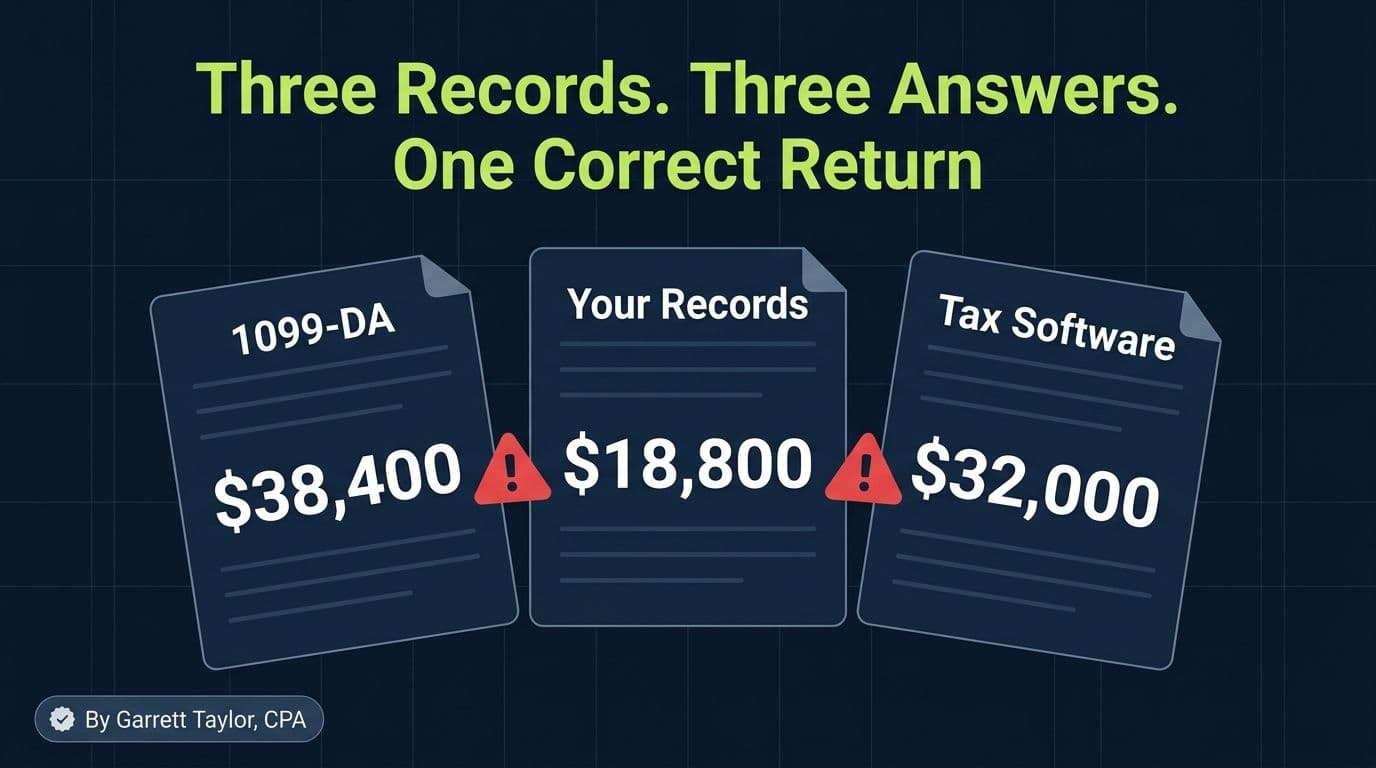

Your 1099-DA Doesn't Match Your Records: The Three-Record Problem, Fixed (2026)

Your 1099-DA, your wallet history, and your tax software all disagree. A CPA explains the five common mismatches and the exact reconciliation workflow.

The Ultimate Guide to Crypto Tax (2026 Edition)

The most comprehensive crypto tax guide online, written by a CPA who files 500+ crypto returns a year. Every taxable event, form, strategy, and 2026 update.

Crypto Cost Basis Methods: FIFO vs Specific ID vs HIFO

Compare FIFO, LIFO, HIFO, and Specific ID for crypto taxes. Worked example shows how the same sale produces 4 different tax bills. Updated for Rev. Proc. 2024-28 and 1099-DA.