State Taxes on Prediction Market Winnings (2026): The Second Bill Kalshi, Polymarket, and Robinhood Traders Forget

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Every state with a broad income tax taxes prediction market profits, and no platform withholds state tax. Nine states (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming) have no broad individual income tax at all.

- ✓Your state bill usually follows your federal characterization. Ordinary income and capital treatment put the net profit into your state return. Gambling treatment puts gross winnings in and pushes losses into a deduction many states refuse to allow.

- ✓Illinois, Connecticut, Indiana, Kansas, Louisiana, Ohio, Rhode Island, Wisconsin, and (for out-of-state platforms) Massachusetts do not give recreational bettors a usable gambling loss deduction. In those states a gambling characterization can tax you on every winning trade while ignoring every losing one.

- ✓The map is moving fast: North Carolina added a gambling loss deduction retroactive to 2025, West Virginia added one for 2026 and rejected the federal 90% cap, and Kentucky, Illinois, and North Carolina enacted brand-new taxes on prediction market operators in 2026.

- ✓Whether a platform is legal in your state and whether your profits are taxable are two different questions. Maryland and Nevada residents blocked from trading still owe tax on profits they made.

Quick answer: Yes, your state almost certainly taxes your prediction market winnings too. If you live in one of the 41 states with a broad income tax, your Kalshi, Polymarket, or Robinhood event contract profits are taxable at the state level on top of the federal bill, and no platform withholds a dime of it. How much you owe depends on two things: where you live, and how your winnings are characterized. In the nine no-income-tax states the answer is usually zero. In most other states you pay your regular rate on the net profit. And in a handful of states, if your trading is ever characterized as gambling, you can owe state tax on your gross winnings with no deduction for losses, which can turn a small profit into a painful bill. This guide maps all three groups, prices the same trader in five states, and covers the moving-state, estimated-payment, and new-state-tax wrinkles nobody else does.

You did the hard part. You worked out that the IRS taxes your event contract profits even though no 1099 ever arrived, you picked a defensible treatment, and you reported the income on your federal return.

Then your state return loads, pulls in your federal numbers, and quietly adds a second bill you never planned for. Depending on where you live, that bill ranges from nothing at all to more than a third of your actual profit.

Here's the thing: state taxes on prediction market winnings are the least-covered part of the entire topic. The IRS question gets argued in every corner of the internet. The state question, the one that varies by thousands of dollars depending on your zip code, gets a one-sentence disclaimer. We prepare returns for prediction market traders in dozens of states, and the state layer is where the genuinely expensive surprises live.

In this guide we'll map the three kinds of states, show why characterization matters more on your state return than your federal one, price the same trader in Texas, California, New York, Illinois, and Massachusetts, and walk through the moving, estimated-payment, and new-operator-tax wrinkles that are reshaping the map in 2026.

Let's dig in.

Do States Tax Prediction Market Winnings? (Yes, With Nine Exceptions)

Start with the mechanical reason the answer is yes almost everywhere: nearly every state income tax begins with a number from your federal return, usually federal adjusted gross income or federal taxable income. Whatever prediction market profit you report federally flows into your state calculation automatically. There is no state that starts from your federal return and then carves out event contracts.

No state revenue department has issued guidance on prediction markets specifically, which mirrors the federal silence. But silence does not mean exemption. It means your profits ride into the state return under whatever character they carried federally, and the state's ordinary rules for that kind of income take over from there.

Two practical points before the map. First, no prediction market platform withholds state income tax. Kalshi, Polymarket, and Robinhood Derivatives all pay out gross. Second, state tax agencies increasingly mirror IRS information. If your federal return shows the income, your state return needs to match, and if you amend federally, most states require a corresponding state amendment within a fixed window.

41 states

have a broad individual income tax that reaches prediction market profits. No platform withholds any of it, and no state has carved event contracts out.

The 60-Second Federal Recap (Your State Answer Depends on It)

Your state bill is downstream of one federal question: what is this income? The IRS has never said how event contracts are taxed, so filers and their preparers choose among four candidate treatments: ordinary income, capital asset, Section 1256 contract, and gambling. Our complete guide to prediction market taxes walks through all four with worked numbers, and our dedicated Kalshi taxes guide applies them to a full trading year.

For state purposes, the four treatments collapse into two buckets:

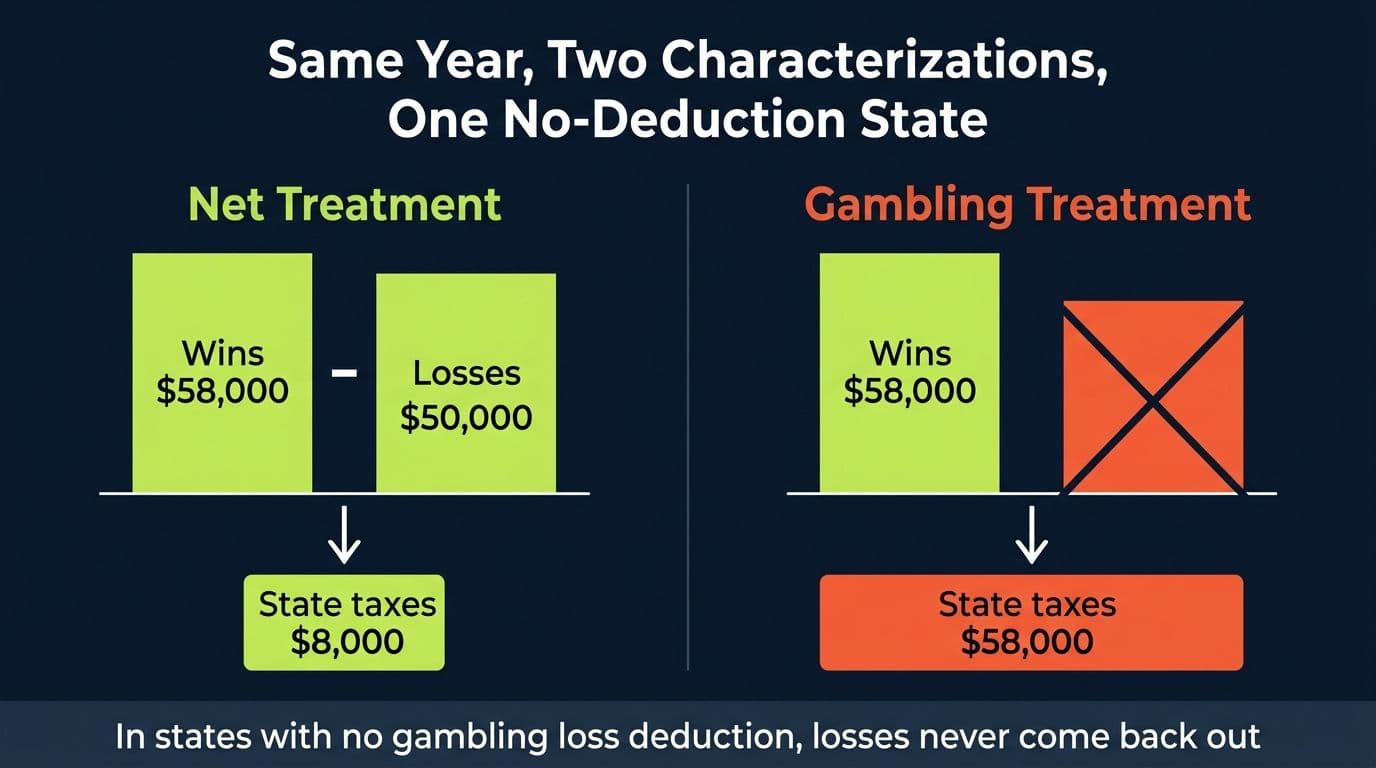

Net-number treatments. Ordinary income, capital, and Section 1256 all put your net result into federal AGI. Win $58,000 on winning trades and lose $50,000 on losing ones, and an $8,000 number flows to your state.

Gross-number treatment. Gambling characterization splits the year in two. Gross winnings go into AGI above the line. Losses come back, if at all, only as an itemized deduction below it. Federally that mostly works out for itemizers. At the state level, it breaks, because a large group of states never lets the losses back in.

One more federal-to-state wrinkle worth knowing: Section 1256's famous 60/40 rate blend is a federal-only benefit in nearly every state. Most states tax capital gains at the same rates as wages, with no preferential long-term rate, so a characterization that saves you real money on Form 6781 federally usually saves you nothing on the state line.

The State Map: Three Kinds of States for Prediction Market Traders

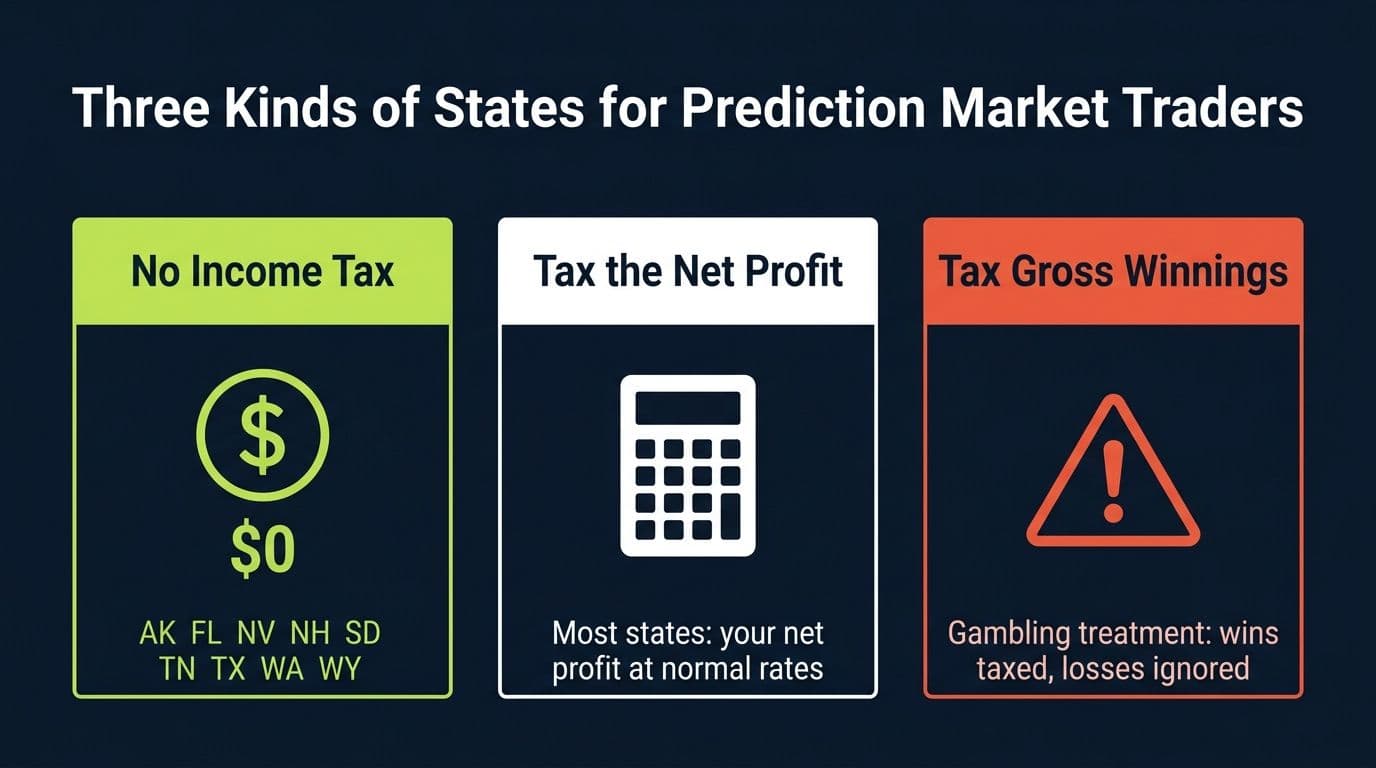

Bucket 1: The Nine No-Income-Tax States

Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming impose no broad individual income tax. For most traders in these states, the state bill on prediction market profits is zero. Two of them deserve a footnote.

New Hampshire taxed interest and dividends for decades, but that tax was repealed for tax periods beginning on or after January 1, 2025. Nothing remains in New Hampshire that reaches trading profits, and even the interest Kalshi pays on cash balances is now outside the state's reach.

Washington is the interesting one. Washington has no income tax but does impose a 7 percent capital gains excise tax on long-term capital gains above an inflation-indexed standard deduction ($278,000 for 2025), with an additional 2.9 percent surtax on gains above $1 million. Event contracts resolve in days or weeks, so even under a capital characterization your gains are short-term and outside the tax. The realistic exposure is different: a Polymarket trader who funds with USDC bought years ago, or who lets winnings sit in crypto that appreciates for over a year before selling, can generate long-term gains that count toward that threshold. The contracts escape Washington's tax. The crypto layer around them might not.

Bucket 2: The Net-Taxing Majority

Most income-tax states simply tax whatever net number your federal characterization produces, at their normal rates. California's brackets run to 12.3 percent plus a 1 percent surcharge above $1 million of income. New York runs to 10.9 percent, and New York City residents add roughly another 3.9 percent on top. Flat-tax states like Colorado (4.4 percent), Illinois (4.95 percent), and Pennsylvania (3.07 percent) apply one rate to the whole number.

In this bucket the planning question is rarely dramatic. Your net profit is taxed like the rest of your income, the bill scales with your bracket, and the main failure mode is simply forgetting the state layer exists when you set money aside during the year.

Bucket 3: The Gross-Winnings Trap States

Here's the bucket that produces the horror stories. If your prediction market activity is characterized as gambling, a specific group of states will tax your gross winnings while giving you no usable deduction for your losses:

States With No Usable Gambling Loss Deduction for Recreational Bettors (July 2026)

| State | Rule | Detail |

|---|---|---|

| Illinois | No deduction | Flat 4.95% on federal AGI; the state explicitly disallows gambling losses |

| Connecticut | No deduction | Starts from federal AGI, allows no itemized deductions; nonresidents are not taxed on gambling winnings |

| Indiana | No deduction | Federal AGI start, no itemized deduction for losses |

| Kansas | No deduction | Loss-deduction bills introduced in 2025 and 2026 died in committee |

| Louisiana | No deduction | Individual gambling losses not deductible |

| Ohio | No deduction | Federal AGI start, no gambling loss deduction |

| Rhode Island | No deduction | Federal AGI start, no itemized deductions |

| Wisconsin | Session method only | Winning sessions taxed in full; losing sessions cannot offset them |

| Massachusetts | Licensed venues only | Losses deductible only from Massachusetts-licensed gaming establishments, which prediction market exchanges are not |

The mechanics are worth spelling out, because they surprise even experienced filers. These states start from federal AGI, and gambling winnings sit inside AGI while gambling losses live below it as a federal itemized deduction. A state that allows no itemized deductions, or none for gambling, taxes the top-line number. Illinois says it in one sentence: the state does not allow a deduction for gambling losses. Connecticut's guidance reaches the same result for residents. Massachusetts law allows losses only against winnings from gaming establishments licensed in the state, a category no prediction market exchange fits. Wisconsin uses a session method: each winning session is income, and losing sessions cannot net against them.

And the map is genuinely in motion:

North Carolina was a gross-winnings state until this month. The budget signed July 8, 2026 added a gambling loss deduction, retroactive to tax years beginning January 1, 2025. Filers who paid North Carolina tax on gross winnings for 2025 should look hard at amending.

West Virginia added a gambling loss modification for tax years beginning on or after January 1, 2026, and wrote it to preserve the full deduction even though the federal One Big Beautiful Bill Act caps federal gambling losses at 90 percent from 2026. West Virginia also excluded losses from unlawful gambling, a detail that matters in a world where regulators dispute which platforms may operate where.

Michigan flipped back in 2021, allowing wagering losses for residents who itemize federally. Nonresidents can deduct only losses placed at Michigan-based venues.

“The federal characterization debate is abstract until you put a state on it. The same break-even year is a non-event in Texas, a rounding error in California, and a five-figure bill in a gross-winnings state. When a client tells me where they live, I can usually tell them how much the characterization question is worth before we run a single number.”

, Leanne Grant, EA

Why Characterization Matters More on Your State Return Than Your Federal One

Put the buckets together and a strange conclusion falls out: the characterization fight can be worth more at the state level than the federal level.

Federally, an itemizing bettor in 2025 deducted losses up to winnings, so ordinary versus gambling treatment changed the shape of the return more than the size of the bill. From 2026 the federal deduction is capped at 90 percent of losses, which creates phantom income at the margins. Painful, but bounded.

At the state level the difference is not bounded. In a no-deduction state, gambling characterization means the state taxes a number that can be many times your actual profit. An active trader who wins $58,000 across winning positions and loses $50,000 across losing ones made $8,000. Illinois, under a gambling characterization, taxes the $58,000.

This cuts the other way too. The dominant practitioner view treats exchange-traded event contracts as financial instruments rather than wagers: they trade on CFTC-regulated exchanges, price continuously, and can be sold before resolution. Most filers we see report under ordinary income or capital treatment, which keeps the net number and defuses the gross-winnings trap entirely. But sports event contracts sit closest to the gambling line, several states actively argue in court that they are gambling, and a trader whose book is all sports contracts in a no-deduction state is carrying real state-level risk on the characterization question. If that's you, the treatment memo you attach to your federal position is doing double duty, and it's worth getting right. Our Robinhood prediction market taxes guide covers why sports and macro contracts may not even belong under the same treatment.

One more state quirk in the gambling bucket: California never adopted the federal 90 percent loss cap. California's conformity to the federal code stops before the One Big Beautiful Bill Act, so a California itemizer characterizing winnings as gambling still deducts losses in full up to winnings on the state return. The federal return takes the 90 percent haircut, the California return doesn't. Same trades, two different loss numbers, both correct.

Worked Example: The Same Trader in Five States

Meet Maya. Single filer, $110,000 salary, and a busy year trading Fed decisions and playoff games. Her winning positions gained $58,000, her losing positions lost $50,000, and her net profit is $8,000. Here's her state bill on that $8,000 under the two paths that matter.

Path one: net treatment (ordinary income or capital). The $8,000 flows into state income and gets taxed at her marginal state rate.

Path two: gambling treatment. The $58,000 goes in gross, and the state decides whether the $50,000 comes back out.

Maya's State Tax on the Same $8,000 Profit (2026, Approximate)

| State | Net Treatment (Ordinary or Capital) | Gambling Treatment | Why |

|---|---|---|---|

| Texas | $0 | $0 | No state income tax |

| California | ~$744 (9.3% marginal) | ~$744 if she itemizes for CA | CA allows full gambling losses; no 90% cap |

| New York (outside NYC) | ~$480 (6.0% marginal) | ~$480 if she itemizes | NY follows the federal itemized deduction |

| New York City | ~$790 (state + city) | ~$790 if she itemizes | Add ~3.9% city tax on the same income |

| Illinois | ~$396 (4.95% flat on $8,000) | **~$2,871** (4.95% on $58,000 gross) | No gambling loss deduction |

| Massachusetts | ~$400 (5% flat on $8,000) | **~$2,900** (5% on $58,000 gross) | Losses deductible only from MA-licensed venues |

Read the Illinois and Massachusetts rows again. Under gambling characterization, Maya's state tax is roughly 36 percent of her actual profit, and that's before her federal bill, which from 2026 also includes phantom income from the 90 percent loss cap. A slightly worse year makes it uglier: if Maya had broken exactly even ($58,000 won, $58,000 lost, $0 profit), Illinois would still tax the full $58,000 under a gambling characterization. That's $2,871 of state tax on zero income.

Now the comparison that shows why this is the quiet second bill: the difference between Maya's best case (Texas, $0) and her worst case (Massachusetts gambling treatment, $2,900) is bigger than the entire federal swing between her cheapest and most expensive treatment on the same numbers. The state layer isn't a footnote to the federal question. For traders in the wrong states, it is the question.

Trading From a Gross-Winnings State?

If you trade event contracts from Illinois, Connecticut, Wisconsin, Massachusetts, or any state in the no-deduction bucket, your characterization memo is worth real money. We prepare federal and state returns for prediction market traders and document the treatment so both returns hold up.

Book a callLegal in Your State vs Taxable in Your State (Two Different Questions)

Prediction markets are in open regulatory warfare with state gaming authorities, and traders keep drawing the wrong tax conclusion from the legal headlines. So let's separate the questions.

Whether you can trade is a licensing fight. Maryland regulators treat sports event contracts as sports wagering that requires a state license. A federal judge declined to let Kalshi keep offering sports contracts there while the case proceeds, and the appeal was argued in the Fourth Circuit in May 2026. Nevada regulators won an injunction that has blocked Kalshi's sports contracts for Nevada residents since December 1, 2025, with the Ninth Circuit appeal argued in April 2026. A New York court declined to block that state's gambling enforcement in July 2026, and Kalshi is appealing. Robinhood simply doesn't offer event contracts to Maryland residents at all.

Whether you owe tax is not. Income is taxable whether the activity that produced it was licensed, unlicensed, or actively banned. The tax code has taxed unlawful income for a century; that principle is exactly how the government won cases against bootleggers. If you traded before your state's restriction took effect, or traded through an out-of-state address, or used a platform your state regulator says shouldn't have served you, the profit is still taxable federally and still taxable by your state of residence.

There's even a sharp edge where the two questions touch: West Virginia's new loss deduction explicitly excludes losses from unlawful gambling activity. If a state characterizes your platform as unlawful gambling and your trading as wagering, you could face the worst of both worlds: winnings taxed in full, losses disallowed twice over. Nobody has litigated that fact pattern yet. You do not want to be the test case.

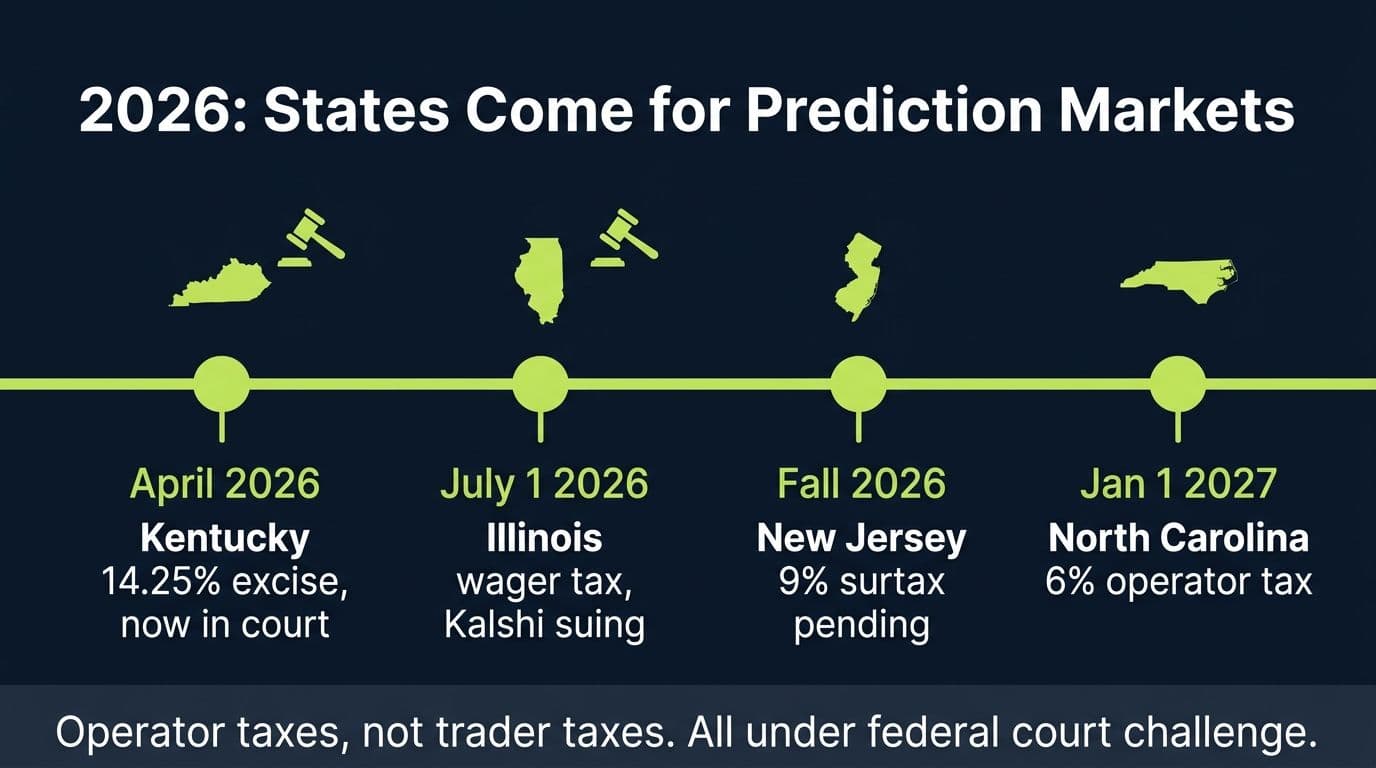

The New State Taxes on Prediction Markets Themselves (2026's Big Story)

Until 2026, prediction markets paid none of the excise taxes that sportsbooks pay, which is a big part of why their prices beat sportsbook odds. States noticed the revenue gap, and this year they moved. Four developments matter, and it's important to understand what they are and are not:

Kentucky enacted a 14.25 percent excise tax on prediction market transactions in April 2026, the first of its kind. A coalition including Kalshi, Polymarket, and Crypto.com sued in June 2026, arguing the tax discriminates against federally regulated exchanges, and the CFTC has filed its own federal suit asserting exclusive jurisdiction.

Illinois passed a law effective July 1, 2026 imposing a tax on sports-related prediction market wagers (1.75 percent on the first $5 million, 3.5 percent above) plus a $15 million licensing requirement. Kalshi sued in federal court on June 23, 2026, and the CFTC moved for a preliminary injunction against the state on July 8, 2026.

North Carolina's new budget imposes a 6 percent tax on prediction market operators' net trading fee revenue starting January 1, 2027, alongside raising the sports betting tax from 18 to 23 percent.

New Jersey advanced a 9 percent surtax on prediction market operator revenue through committees in June 2026, then held it for the fall session.

Here's the taxpayer takeaway: none of these are taxes you calculate or remit. They are levied on operators, and every one of them is under active constitutional challenge, with most observers expecting the federal-versus-state jurisdiction fight to reach the Supreme Court. What they mean for you is indirect but real. Operator taxes get passed through as wider spreads, higher fees, or contract delistings in specific states, and they signal that your state's revenue department is now paying close attention to this asset class. The era of prediction markets flying under the state radar ended in 2026.

Moving, Nonresident, and Part-Year Problems

Prediction market income lives on your phone, which makes people assume geography doesn't matter. State tax law disagrees.

The default rule: your state of residence taxes the income. Online trading profit on a federally regulated exchange has no physical situs. It isn't like walking into a casino in another state, where the winning has a location and the source state may claim withholding. Your Kalshi profit is taxed where you live when the income lands. Connecticut makes the point explicitly in its gambling guidance: nonresidents are not taxed on gambling winnings, residents are.

Part-year residents allocate by date. Move from California to Texas on July 1 and your January-through-June settlements belong on the California part-year return while the rest escape state tax. That makes settlement timing around a move worth actual money, and it makes your trade history export, with dates, the document that proves the split. Note that it's when the income was realized that controls, not when you withdrew it to your bank.

The statutory residency trap. Moving your driver's license to Florida while keeping an apartment in New York and spending most of the year there doesn't work. New York treats anyone who maintains a permanent place of abode and spends more than 183 days in the state as a full resident, taxable on everything, including the trading income you thought you'd relocated. High-tax states audit exactly this pattern, and a big prediction market year is exactly the kind of income spike that draws the audit.

Michigan-style nonresident quirks. A few states with venue-based rules limit nonresident loss deductions to in-state establishments, which maps awkwardly onto online exchanges. If you file in multiple states, the gambling characterization multiplies the complexity, one more argument for documenting a financial-instrument treatment instead.

State Estimated Taxes: The Quarterly Bill Nobody Warns You About

A good prediction market year creates two estimated tax problems, and traders reliably handle only the federal one.

States run their own estimated payment systems with their own thresholds, schedules, and penalties. New York requires estimated payments once you expect to owe $300 or more beyond withholding. California's system is front-loaded, collecting 30 percent of the year's estimate in April, 40 percent in June, nothing in September, and 30 percent in January.

The safe harbors have teeth for high earners. Both California and New York demand 110 percent of last year's tax, rather than 100 percent, once prior-year AGI clears $150,000. And California disallows the prior-year safe harbor entirely once current-year AGI reaches $1 million: at that level you must pay in 90 percent of the current year's actual tax as you go, which is brutal when the income is as lumpy as a big election-cycle trading run.

The practical move is simple. When you set aside your federal reserve on a big settlement, set aside the state layer at the same time at your marginal state rate, and check your state's quarterly schedule instead of assuming it matches the IRS. A trader who banks 24 percent federal plus 9.3 percent California on every big win never meets an underpayment penalty from either government.

How to Get the State Side Right: A Five-Step Checklist

Step 1: Fix your federal characterization first. Everything downstream depends on it. Document the treatment, apply it consistently across platforms, and understand what it does to your state's math before you file, not after.

Step 2: Identify your bucket. No-income-tax state, net-taxing state, or gross-winnings state. If you're in the third bucket and any part of your book is sports contracts, treat the characterization memo as a state-tax document, because that's where it's worth the most.

Step 3: Reconcile the numbers that flow through. Your state return inherits federal AGI, so the platform-by-platform reconstruction you did federally (trade exports, PnL statements, fee allocation) is also your state workpaper. Keep the export with dates; it's what proves a part-year allocation or a session calculation.

Step 4: Handle the crypto layer separately if you trade Polymarket. USDC-settled trading adds property dispositions that carry their own state consequences, including in Washington, where long-held crypto can hit the capital gains excise even though the contracts themselves never will.

Step 5: Pay your state quarterly alongside the IRS. Same calendar reminder, second payment. Use your state's own schedule and safe harbor, and remember the 110 percent rule if you had a big prior year.

Pro Tip

If you paid state tax on gross gambling winnings in North Carolina for 2025, the July 2026 budget made the new loss deduction retroactive to tax years beginning January 1, 2025. Amending that return may put real money back in your pocket. Check before the amendment window closes.

When the State Layer Means You Need a Professional

Handling state taxes on prediction market winnings yourself is fine if: you live in a no-income-tax state, or you're a modest-volume trader in a net-taxing state reporting ordinary income, where the state return mostly takes care of itself.

Get professional help if: you trade meaningful volume from a gross-winnings state, your book is sports-heavy anywhere the characterization fight is live, you moved states mid-year with open positions, you're facing a statutory residency question, you have Polymarket crypto layers on top of the contracts, or you already filed a 2025 return in a state whose rules just changed retroactively.

The state layer is where a defensible federal position either holds together or falls apart, and it's where we see the most money left on the table, in both directions: traders who never reported the state income, and traders who overpaid a gross-winnings state they had strong grounds to fight.

Get Both Returns Right, Federal and State

Flat-fee preparation for prediction market traders: characterization documented, all platforms reconciled, state return matched to your state's actual rules, amendments filed where the law moved in your favor. Signed by a CPA who does this every season.

Book a callFAQ: State Taxes on Prediction Market Winnings

Frequently Asked Questions

Do you have to pay state taxes on Kalshi winnings?

Yes, if you live in a state with an income tax. Kalshi profits flow from your federal return into your state return automatically, taxed under whatever characterization you used federally. Kalshi withholds no state tax, so the full payment obligation is yours. Residents of the nine no-income-tax states generally owe nothing at the state level.

Do states tax prediction market winnings?

All 41 states with a broad income tax do. State returns start from federal numbers, and no state has exempted event contracts. The nine exceptions are Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming, which have no broad individual income tax.

Which states have no income tax on prediction market winnings?

Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. New Hampshire's separate interest and dividends tax was repealed for periods beginning in 2025, and Washington's capital gains excise reaches only long-term gains above an indexed threshold, which short-lived event contracts don't produce.

Can I deduct my prediction market losses on my state return?

Under ordinary or capital treatment, losses are already netted into the number your state taxes. Under gambling treatment it depends entirely on your state: many states follow the federal itemized deduction, but Illinois, Connecticut, Indiana, Kansas, Louisiana, Ohio, Rhode Island, and Wisconsin give recreational bettors no usable deduction, and Massachusetts allows losses only from state-licensed venues.

Which states do not allow gambling loss deductions?

As of July 2026: Illinois, Connecticut, Indiana, Kansas, Louisiana, Ohio, Rhode Island, and Wisconsin (which uses a session method), plus Massachusetts for anything outside its licensed venues. North Carolina left the list in 2026 with a deduction retroactive to 2025, West Virginia added one for 2026, and Michigan flipped in 2021. Verify your state's current rule before filing; this list keeps moving.

Do I pay state taxes where I live or where the platform is based?

Where you live. Online trading profit on a federally regulated exchange has no physical location, so it's taxed by your state of residence when the income is realized. The platform's home state is irrelevant, and Connecticut's guidance states directly that nonresidents aren't taxed on gambling winnings.

What happens to my prediction market taxes if I move states mid-year?

You file part-year returns and allocate by date: settlements while you lived in the old state belong to it, later ones to the new state. Keep your dated trade export as proof. And beware statutory residency: keeping a home in a high-tax state and spending more than 183 days there can make you a full resident regardless of where your license says you live.

Is Kalshi legal in my state, and does that change my taxes?

Legality and taxability are separate questions. Maryland and Nevada have blocked Kalshi's sports contracts through licensing fights, and litigation is active in several other states. None of that erases tax on profits you made. Income from restricted or even unlawful activity is fully taxable, federally and at the state level.

Does Kalshi, Polymarket, or Robinhood withhold state taxes?

No. No prediction market platform withholds federal or state income tax on trading profits. Every dollar arrives pre-tax, and both your federal and state payment obligations, including quarterly estimates, are entirely yours to handle.

Do I need to make state estimated tax payments on prediction market profits?

If your state has an income tax and your winnings are meaningful, almost certainly. States run their own quarterly systems with their own schedules: New York's threshold is $300 of expected tax, and California front-loads payments at 30/40/0/30 percent. High earners typically need 110 percent of prior-year tax to stay penalty-free.

What are the new Kentucky and Illinois prediction market taxes? Do I have to pay them?

No. Kentucky's 14.25 percent excise, Illinois' wager tax, and North Carolina's 6 percent levy are taxes on operators, not traders, and all face active federal court challenges. You'll feel them, if at all, through wider spreads, higher fees, or delisted contracts, not on your return.

Does Washington's capital gains tax apply to prediction market profits?

Generally no. Washington's excise applies only to long-term capital gains above an inflation-indexed deduction ($278,000 for 2025), and event contracts resolve far too quickly to generate long-term gains. The exception is the crypto layer: USDC or other crypto held over a year and disposed of in connection with Polymarket trading can count toward the threshold.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Prediction Market Taxes (2026): How Kalshi, Polymarket, Robinhood and Every Major Platform Gets Taxed

How prediction market taxes work on Kalshi, Polymarket, Robinhood and more. A CPA splits platforms by settlement type and shows exactly what to report.

Kalshi Taxes (2026): A CPA's Guide to the Forms You'll Get, the One You Won't, and What You Owe

Kalshi sends 1099s for interest, rewards, and crypto conversions, but nothing for your trading profit. A CPA walks through every form, four tax treatments, and one full worked year.

Robinhood Prediction Market Taxes (2026): The Statement You Get, the 1099 You Don't, and What You Owe

Robinhood issues no 1099 for event contracts, just an Annual Statement the IRS never sees. A CPA explains the form gap, four tax treatments, and a full worked year.