Hyperliquid Taxes (2026): A CPA's Guide to Perps, Funding Payments, and the Airdrop the IRS Never Saw

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Hyperliquid is non-custodial and non-KYC, issues no tax forms, and reports nothing to the IRS. After Congress repealed the DeFi broker rule in April 2025, no Hyperliquid 1099-DA is coming, ever.

- ✓Hyperliquid perps fail the Section 1256 threshold test because the exchange is not CFTC-registered. Do not report them on Form 6781 as 60/40. The real fight is capital gain versus ordinary treatment.

- ✓Funding payments settle every hour and have no direct IRS guidance. The conservative position treats net funding received as ordinary income; document your method and apply it consistently.

- ✓The HYPE genesis airdrop (roughly 310 million tokens, 31% of supply, November 2024) was ordinary income at fair market value when you gained control, and that value became your cost basis.

- ✓Your activity is invisible until it isn't: the moment USDC touches a KYC'd exchange, a 1099-DA reports your proceeds with no basis, and the blockchain preserves everything else permanently.

Pro Tip

Written by Garrett Taylor, CPA (License #133092). Reviewed by Leanne Grant, EA (#00167954-EA). Last updated: July 9, 2026.

Quick answer: Hyperliquid taxes are 100% self-reported: profits are fully taxable to US taxpayers, and Hyperliquid reports nothing to the IRS. No 1099-DA, no 1099-B, no forms of any kind. Perpetual futures gains do not qualify for 60/40 Section 1256 treatment, funding payments have no direct IRS guidance, and the HYPE airdrop was ordinary income the moment you could control the tokens. Every piece of that lands on you to reconstruct from on-chain data and report under a documented, consistent method. This guide covers each open question, the conservative and aggressive positions, and one trader's complete year with real numbers.

Hyperliquid made on-chain perps feel like a real exchange: an order book, deep liquidity, one-click leverage, no account creation, no KYC, no emails.

Then tax season arrives, and the same features that made trading frictionless make reporting brutal. There's no statement in the mail. No export marked "for tax purposes." No form telling you, or the IRS, what happened. Just thousands of fills, hourly funding ticks, maybe an airdrop, all sitting on a public blockchain under a wallet address only you can connect to your Social Security number. Until someone else does.

Here's the deal: Hyperliquid taxes are hard because the platform gives you zero paperwork while the law gives you zero settled answers. We prepare returns for DeFi and derivatives traders every season, and Hyperliquid accounts are consistently the heaviest reconstruction lift on the desk: more taxable events, more open characterization questions, and less documentation than any centralized venue.

In this guide to Hyperliquid taxes we'll cover whether and what Hyperliquid reports, how Hyperliquid perps and funding payments can be taxed under current law, the HYPE airdrop bill most recipients never planned for, and one trader's full year priced under the competing frameworks.

Let's dig in.

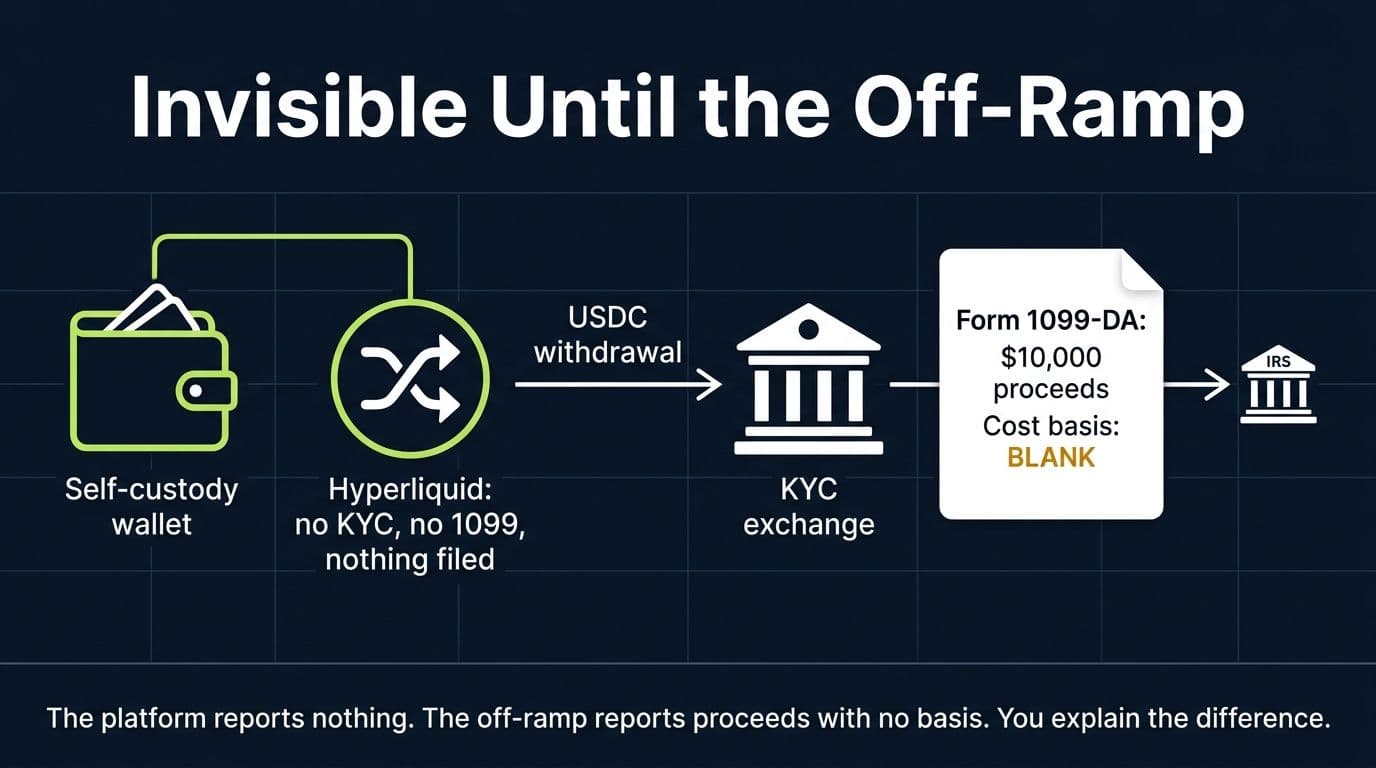

Does Hyperliquid Report to the IRS?

No. And unlike most crypto exchanges, this isn't a "not yet." It's structural.

Hyperliquid is a decentralized exchange running on its own Layer 1 blockchain. Trades execute and settle on-chain against USDC collateral, assets stay in your own wallet, and there is no custodian, no broker-dealer entity, and no KYC file with your name on it. There is no legal entity in the flow that collects the information a 1099 requires.

The regulatory chapter closed in April 2025. The Treasury regulation that would have forced DeFi front-ends to report like brokers (the so-called DeFi broker rule) was repealed by Congress under the Congressional Review Act when the President signed H.J.Res.25 on April 10, 2025. Under the CRA, the IRS cannot reissue a substantially similar rule without new legislation. Custodial exchanges like Coinbase and Kraken still file Form 1099-DA for their customers. Non-custodial platforms like Hyperliquid do not, and will not.

So the IRS gets no form. Here's what it gets instead:

Everything, eventually. Every Hyperliquid fill, transfer, and funding tick is permanently recorded on a public chain, readable by anyone with an explorer and analyzed at scale by the blockchain analytics firms the IRS already contracts with. And the moment your USDC touches a KYC'd exchange to cash out, that exchange's 1099-DA reports your proceeds to the IRS, usually with a blank cost basis. Proceeds with no explanation are exactly what triggers automated mismatch notices. The IRS digital asset rules put the reporting obligation on you either way, and you'll answer "Yes" to the Form 1040 digital asset question.

One more thing, because people ask: Hyperliquid geo-blocks US users at the website level, and its terms exclude US persons, but the protocol itself is permissionless. We're not here to advise on access. We'll just state the tax fact plainly: US taxpayers owe US tax on worldwide income, no matter what platform terms were violated, what VPN was involved, or how offshore the venue feels. The tax obligation and the platform rules are separate problems.

Every hour

Hyperliquid settles perp funding payments every single hour, which means an active trader can log thousands of micro income events per position in a year, none of them summarized on any tax document.

Do You Owe Taxes on Hyperliquid If You Never Cash Out?

Yes. The most persistent myth in Hyperliquid taxes is that nothing counts until dollars hit a bank account. "I never withdrew to my bank" has never been the test. Crypto is property, and tax attaches when property is disposed of or income is received, not when dollars land in checking.

Here's the taxable-event map for a typical Hyperliquid user:

What's Taxable on Hyperliquid (2026)

| Activity | Taxable? | Character |

|---|---|---|

| Bridging your own USDC to Hyperliquid | Generally no | Transfer of the same asset you already own |

| Closing a perp position at a profit or loss | Yes | Capital vs ordinary: unsettled (see below) |

| Receiving funding payments | Yes (conservative view) | Ordinary income (method-dependent) |

| HYPE airdrop or points converting to tokens | Yes | Ordinary income at fair market value on receipt |

| Spot trade, including USDC to token and token to token | Yes | Capital gain or loss on the asset disposed |

| Staking HYPE and receiving rewards | Yes | Ordinary income at receipt |

| HLP or other vault yield | Yes | Ordinary income (characterization nuances apply) |

| Withdrawing USDC to a centralized exchange | Not by itself | But the exchange's later 1099-DA makes you visible |

Almost everything on that list is invisible to the IRS in real time and fully taxable anyway. That combination rewards exactly one habit: complete Hyperliquid records, kept as you go.

How Are Hyperliquid Perps Taxed? The Open Question

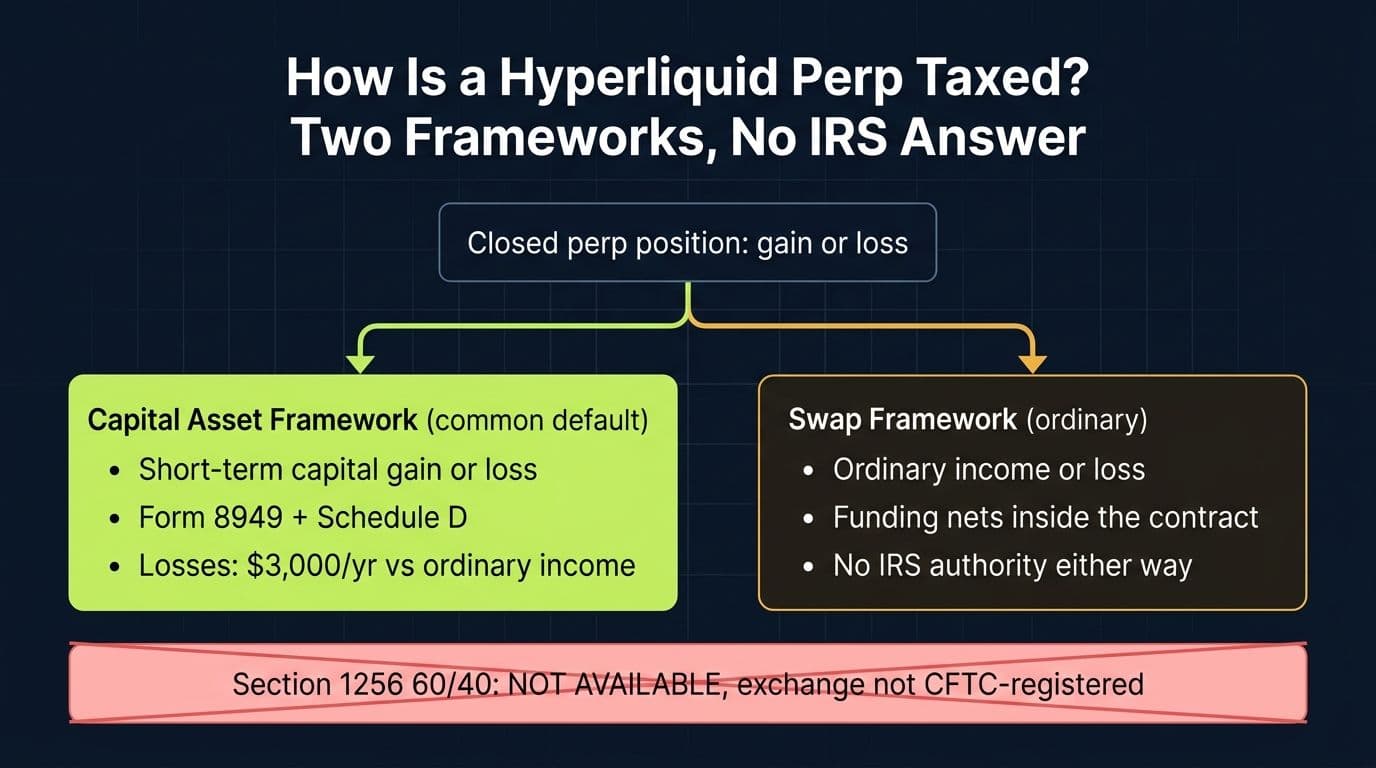

Perpetual futures are Hyperliquid's main event, and they're also the biggest unresolved question in Hyperliquid taxes, and honestly in crypto tax generally. A perp is a leveraged derivative that tracks a spot price with no expiration date, kept tethered to spot by funding payments between longs and shorts. The IRS has never said how these instruments are characterized. Let's take the question in three pieces.

First, Clear the Myth: No 60/40 Treatment

Section 1256 gives regulated futures contracts a blended 60% long-term, 40% short-term rate with mark-to-market accounting. To qualify, a contract generally must trade on a qualified board or exchange, meaning a CFTC-designated market or equivalent. CME Bitcoin futures qualify. Hyperliquid does not. It is not registered with the CFTC in any capacity, so Hyperliquid perps fail Section 1256 at the threshold, before the harder doctrinal questions even start. Reporting Hyperliquid perps on Form 6781 as 60/40 is not an aggressive position; it's an error.

The Real Fight: Capital Gain or Ordinary Income

With 1256 off the table, two frameworks compete, and each has real support and real problems.

The capital asset framework treats each closed perp position as a disposition producing capital gain or loss, short-term or long-term by holding period (in practice, almost always short-term). Supporters point to Section 1234A, which treats gain or loss from terminating rights or obligations with respect to property that would be a capital asset as capital gain or loss. A perp referencing Bitcoin, itself a capital asset, fits that frame comfortably. This is the treatment most crypto tax software applies by default and the position most filers are already on, knowingly or not.

The swap framework characterizes perps as notional principal contracts: the funding leg looks like the periodic payments of a financial swap, and under this view, gains and losses on close are ordinary, with net funding recognized as ordinary income or expense over the year. It has economic logic (no expiry, periodic payments) and one practical attraction we'll cover under funding below. It also has to explain away the swap regulations' exclusion of futures-like instruments and Section 1234A's pull toward capital treatment.

Which should you pick? For most individual traders, the capital framework is the conservative, widely used default: it matches how the software works, keeps you inside Form 8949 and Schedule D, and avoids claiming ordinary-loss benefits the IRS might challenge. What matters more than the choice is the discipline around it. Pick a framework deliberately, document why, and apply it consistently across positions and across years. Switching treatments year to year without documentation looks like an unauthorized accounting method change and reopens old returns to scrutiny. For material positions, a disclosure statement (Form 8275) is worth discussing with your preparer.

The 2026 Wrinkle: Onshore Perps and the CME Lawsuit

One development keeps confusing people this year. In May 2026 the CFTC approved the first US-regulated perpetual futures on designated contract markets, and registered US venues now list perp-style products. Some commentators argue those specific onshore products may qualify for Section 1256. Then CME Group sued the CFTC in June 2026, arguing perpetual contracts are swaps, not futures, and the litigation is live.

Whatever happens there, none of it changes the Hyperliquid answer. A regulatory label on someone else's exchange doesn't move a contract on an unregistered offshore protocol into Section 1256. Hyperliquid perps fail the exchange-registration test regardless of how the onshore fight resolves. If you trade both onshore perps and Hyperliquid, expect different tax mechanics for economically similar trades, and keep the records separated.

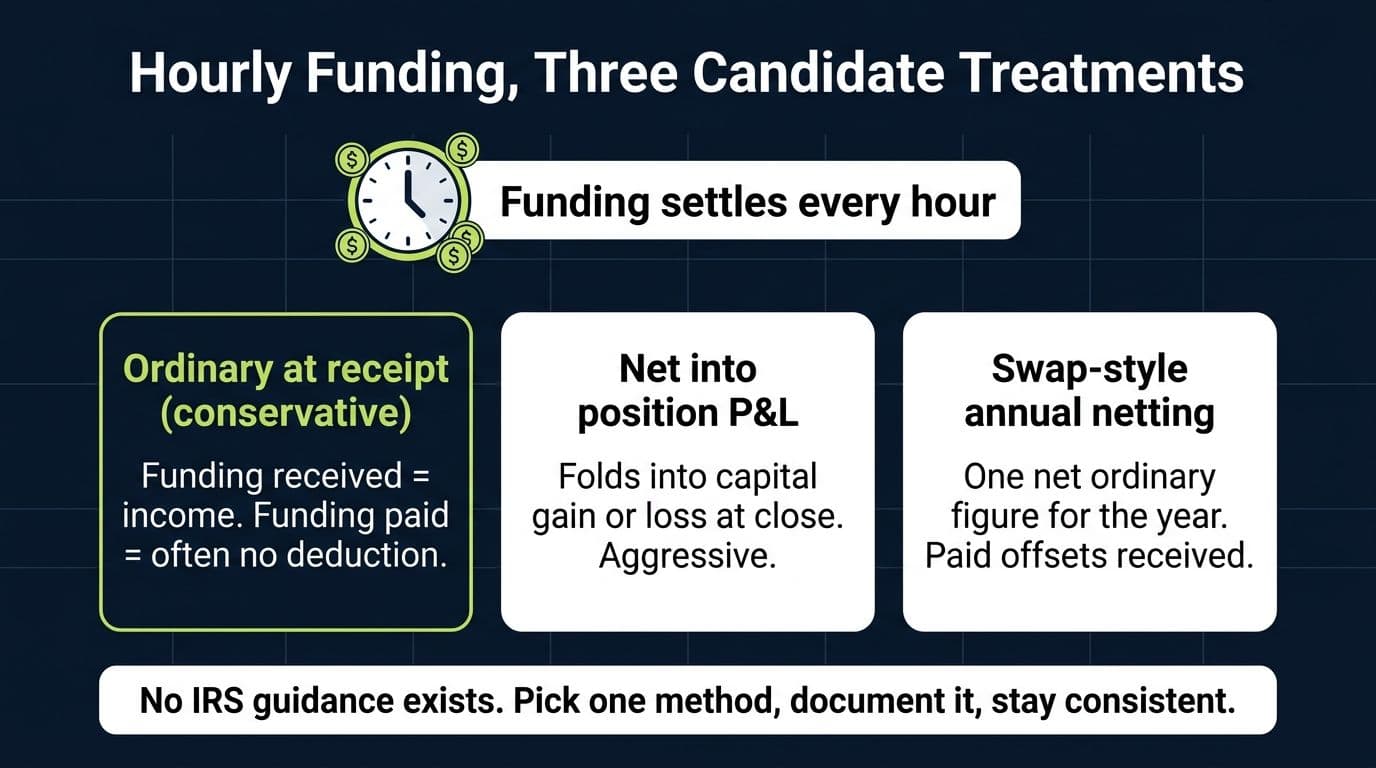

Funding Payments: Tiny, Hourly, and a Real Tax Problem

Every hour, Hyperliquid settles funding between longs and shorts. Individually the amounts are cents or dollars. Across an active year they add up to real money and a genuinely annoying tax question, because the IRS has never addressed funding at all.

Three treatments show up in practice:

- Ordinary income at receipt (conservative). Funding received is ordinary income; funding paid is an expense. The catch: for investors (not trade-or-business traders), that expense is a miscellaneous itemized deduction, which is currently disallowed. You pick up the income and may get nothing for the cost.

- Net into the position. Fold funding into the position's P&L so it lands inside the capital gain or loss at close. Operationally clean, arguably aggressive, and it can convert ordinary income into capital gain, which is exactly the kind of quiet recharacterization examiners look for.

- Swap-style annual netting. Under the swap framework, funding received and paid net into a single ordinary figure for the year. This is the one practical advantage of the swap framework: funding paid actually offsets funding received instead of vanishing into a disallowed deduction.

Our lean for most filers: treat net funding received as ordinary income and don't get clever. And a warning for the basis-trade crowd: if you're running delta-neutral funding capture (long spot, short perp), you're deep in straddle and conversion-transaction territory, where loss deferral rules and ordinary-income recharacterization can both apply. That's a sit-down-with-a-professional structure, not a software checkbox.

“The Hyperliquid returns that scare me are not the aggressive ones, they're the incomplete ones. Thousands of fills, funding ignored entirely, an airdrop nobody reported, and a 1099-DA from the off-ramp exchange showing proceeds the return never explains. Each piece is fixable. Together they read like concealment.”

, Leanne Grant, EA

The HYPE Airdrop: The Tax Bill Nobody Withheld

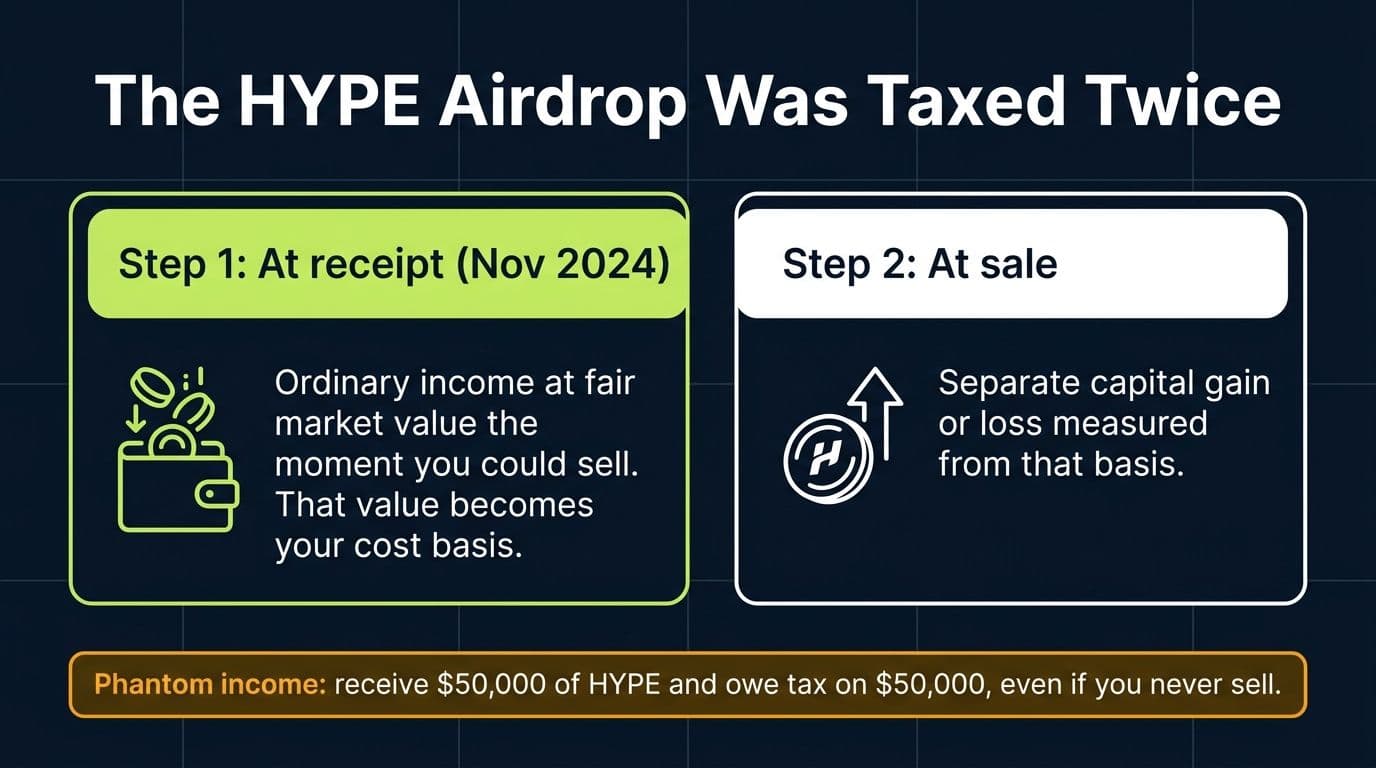

On November 29, 2024, Hyperliquid's genesis event distributed roughly 310 million HYPE, about 31% of total supply, to early users based on accumulated points. No VC carve-outs, no exchange allocations, just one of the largest airdrops in crypto history landing directly in user wallets.

It was also, for US recipients, a large pile of ordinary income. Under the IRS's airdrop framework (Rev. Rul. 2019-24), you recognize ordinary income equal to the tokens' fair market value at the moment you gain dominion and control, meaning the ability to transfer or sell. That value becomes your cost basis, and the clock starts for holding period. Sell later and the difference is a separate capital gain or loss.

Two traps inside that rule:

The valuation trap. Your income is measured at the moment control attached, not at the price a week later, and launch-window prices moved violently. Document the value at your actual receipt time with an exchange or aggregator snapshot. If your allocation had lockups, each tranche is income when it unlocks and becomes transferable, not at announcement.

The phantom income trap. Receive HYPE worth $50,000 and you owe tax on $50,000 of ordinary income even if you never sell. If the price then falls and you sell for $30,000, that's a separate $20,000 capital loss, and it does not undo the original income. Airdrop recipients who neither sold nor set aside cash have painted themselves into real corners this way.

If you received the airdrop and didn't report it on your 2024 return, deal with it now, not after a notice. An amended return filed proactively is a cleanup; the same correction after IRS contact is a negotiation. Our guide to responding to IRS crypto tax notices explains how the mismatch machinery works.

Points Farming and the Next Airdrop

Hyperliquid's points era didn't end with the genesis event, and the wider ecosystem (HyperEVM projects, vault protocols, ecosystem tokens) runs on the same points-then-token playbook.

The good news: under the prevailing view, accruing points is not itself taxable. Points typically have no ascertainable market value and no transferability; they're a marketing ledger, not property in your control. Income arrives when points convert into an actual token you can transfer or sell, taxed as ordinary income at that moment's value, exactly like the HYPE distribution. Keep the timeline evidence: screenshots of point balances, the conversion date, and the token's value at receipt. Farmers running multiple wallets should keep records per wallet, which segues into a rule that surprises people.

Spot Trading, Staking, and Vaults: The Quieter Tax Events

Perps get the attention in every discussion of Hyperliquid taxes, but most Hyperliquid users also generate a steady stream of ordinary crypto taxable events on the same wallet.

Spot trades. Standard property rules apply: every swap is a disposal, including USDC into HYPE, HYPE into an ecosystem token, and token back to USDC. Since January 1, 2025, basis must be tracked wallet by wallet under Rev. Proc. 2024-28, with FIFO as the default unless you document specific identification. Your Hyperliquid wallet's basis lives separately from your Coinbase account and your other wallets. Our crypto-to-crypto trades guide covers why every hop counts.

Staking HYPE. Staking rewards are ordinary income at fair market value when received, on the same dominion-and-control logic as airdrops, and each reward batch starts its own basis and holding period. Yes, that's tedious at daily reward frequency. It's still the rule.

HLP and other vaults. Hyperliquid's HLP vault pays depositors a share of market-making P&L and fees. How vault returns are characterized (yield versus allocated trading results) is genuinely unsettled, but the conservative posture is to pick up vault gains as ordinary income as they're credited and get professional advice if the amounts are material. What you cannot do is treat vault balances as a black box that only becomes taxable at withdrawal.

A Worked Example: Marcus's Hyperliquid Year

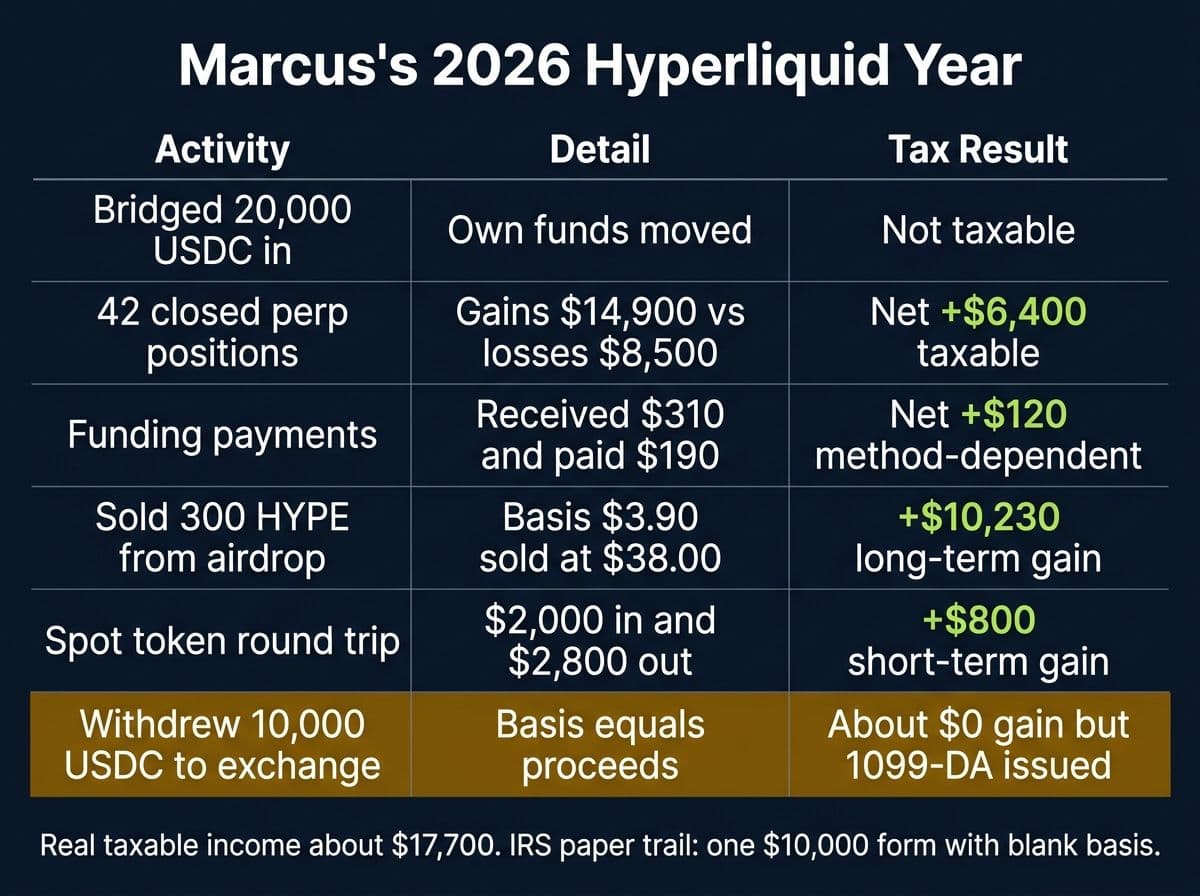

Numbers make Hyperliquid taxes concrete. Meet Marcus: 24% federal bracket, long-term capital gains rate of 15%, one Hyperliquid wallet. Here's his complete 2026.

Marcus's 2026 Hyperliquid Activity

| Activity | Detail | 2026 Tax Consequence |

|---|---|---|

| Bridged 20,000 USDC in January | Own funds moved from another wallet | Not taxable |

| 42 closed perp positions (BTC, ETH, SOL) | Gains $14,900, losses $8,500, net +$6,400 | Taxable; character depends on framework |

| Funding payments | Received $310, paid $190 | Method-dependent (see below) |

| Sold 300 HYPE from the 2024 airdrop | Received at $3.90 (2024 income then); sold at $38.00 | $11,400 proceeds minus $1,170 basis = $10,230 long-term gain |

| Spot round trip on an ecosystem token | 2,000 USDC in, sold for $2,800 | +$800 short-term capital gain |

| Withdrew 10,000 USDC to a KYC'd exchange, sold for USD | Basis roughly equals proceeds | Roughly $0 gain, but generates a 1099-DA |

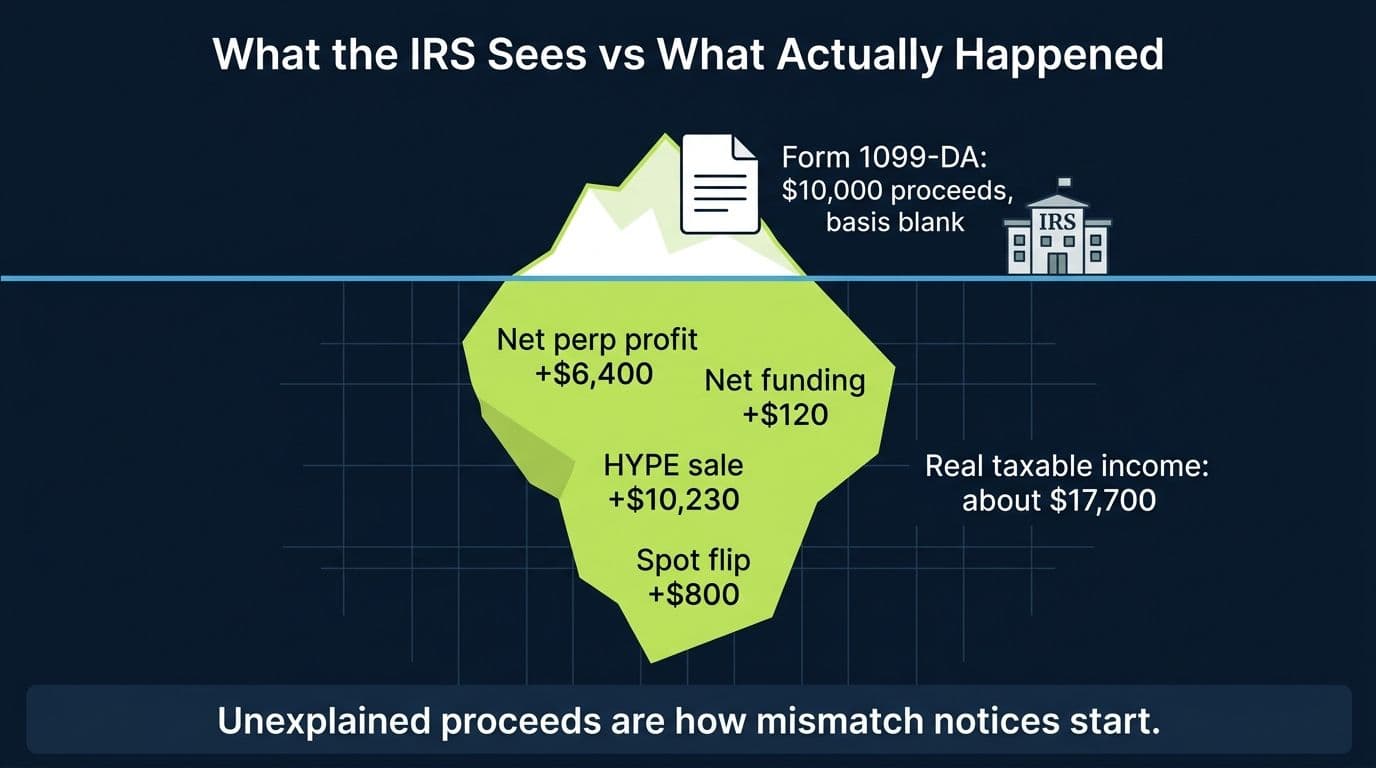

What the IRS Actually Sees in January

One document exists anywhere in the system: the off-ramp exchange's 1099-DA showing $10,000 of USDC proceeds with no cost basis. That's it. The $6,400 of perp profit, the funding, the $10,230 HYPE gain, the $800 token flip: none of it appears on any form.

Marcus's real 2026 taxable income from Hyperliquid is about $17,700. The IRS's paper picture is $10,000 of unexplained proceeds. Whichever way he files, that gap gets resolved: either his return explains it, or the automated matching system asks him to.

The Same Year Under Both Frameworks

Marcus's Federal Bill: Capital Framework vs Swap Framework (2026)

| Item | Capital Framework (conservative) | Swap / Ordinary Framework |

|---|---|---|

| Net perp P&L (+$6,400) | Short-term capital, 24% = $1,536 | Ordinary with funding netted: $6,520 at 24% = $1,565 |

| Funding received ($310) | Ordinary, 24% = $74 | Included above |

| Funding paid ($190) | No deduction (investor) | Netted above |

| HYPE sale (+$10,230 long-term) | 15% = $1,535 | 15% = $1,535 |

| Token flip (+$800 short-term) | 24% = $192 | 24% = $192 |

| USDC off-ramp | $0 | $0 |

| **Total federal** | **$3,337** | **$3,292** |

In a profitable year the frameworks land within $45 of each other, because short-term capital and ordinary rates match. The divergence shows up in bad years: a $30,000 net perp loss offsets only $3,000 of ordinary income per year under the capital framework, while ordinary characterization could be worth far more depending on how the activity is classified. Traders who pick a framework based on one good year's math, then want the other framework's loss rules later, are the audit story writing itself. Don't be that filing.

And don't forget the 2024 footnote: Marcus's 500 HYPE at $3.90 was $1,950 of ordinary income on his 2024 return. If it isn't there, an amended return belongs on this year's to-do list.

Sitting on a Hyperliquid Reconstruction Problem?

We rebuild full on-chain histories: perps characterized and documented, funding handled, airdrop basis established, and a return that explains every dollar the off-ramp reported. Flat-fee, done by a crypto CPA.

Book a callHow to Report Hyperliquid on Your Return, Step by Step

- Export everything, now. Pull your complete fill history, funding history, and transfer log from the interface and API while it's easy, and snapshot your wallet's activity from a block explorer. On-chain data is forever; convenient exports are not.

- Establish basis for every asset in the wallet. USDC bridged in carries its original basis. Airdropped and earned tokens take fair market value at receipt. Remember the per-wallet rule: this wallet's basis pool is its own.

- Compute realized perp P&L per closed position. Gains and losses separately, not just the net, and reconcile against your funding history so nothing double-counts.

- Pick your framework and write it down. Capital treatment on Form 8949 and Schedule D is the common conservative default. If you take swap-style ordinary treatment, document the analysis and consider disclosure. Never Form 6781.

- Report ordinary income items on Schedule 1. Airdrops and points conversions at receipt value, staking rewards, vault yield, and net funding received under the conservative method.

- Reconcile the off-ramp. Whatever a centralized exchange will report on a 1099-DA must tie to what your return shows, with basis documented from your own records, because the form's basis box will be blank or wrong.

- Answer the digital asset question "Yes" and plan estimates. Nothing was withheld all year. A good year means quarterly estimated payments, and a great year means making them on time.

Pro Tip

Run the export and reconciliation quarterly, not in April. Hyperliquid histories are painless to pull in small pieces and miserable to reconstruct across a full year of hourly funding events, delistings, and wallet hops.

Wash Sales, FBAR, and the Questions That Come Up Eventually

Wash sales. Under current law the wash-sale rule applies to securities, and crypto held as property sits outside it, so realized crypto losses are generally deductible even with quick repurchases. Proposals to extend wash-sale rules to digital assets keep circulating, so confirm the rule's status for the year you're filing. Cash-settled perp losses are even further from the rule's current text, but loss-harvesting patterns with no substance invite scrutiny under broader doctrines regardless.

FBAR and Form 8938. A self-custodied wallet is not an account with a foreign financial institution, and under current FinCEN guidance a crypto-only foreign account is not FBAR-reportable, though FinCEN has signaled intent to change that. Hyperliquid's structure (your keys, no custodian) sits outside today's FBAR net for most users. Form 8938 is murkier at the edges. If you also hold accounts on offshore centralized exchanges, that's a different analysis; flag it with your preparer.

Prediction markets on Hyperliquid. The Hyperliquid ecosystem now includes binary outcome markets alongside perps. Those raise the same unsettled characterization questions as every other crypto-settled prediction venue, which we cover across platforms in our prediction market taxes pillar and in depth for Polymarket, where the no-1099, USDC-settled mechanics look a lot like Hyperliquid's.

When to DIY and When to Bring In a Pro

Straight talk:

Handling Hyperliquid taxes yourself is workable if: your Hyperliquid volume is modest, your software ingests the full Hyperliquid history cleanly, you're comfortable with short-term capital treatment for perps and ordinary income for funding and airdrops, and your off-ramp amounts reconcile to your records.

Get professional help if: you're a high-frequency trader with thousands of fills, you received a significant HYPE allocation (especially unreported in 2024), you run delta-neutral or cross-venue basis trades, you're weighing ordinary treatment for losses, you use HLP or other vaults at scale, or a 1099-DA mismatch notice already arrived. Here's what a crypto-specialized CPA costs and how to vet one.

On a venue with no forms, no guidance, and permanent public records, the trader with documented methods and complete reconciliation holds every good card. The one improvising in April holds none.

Get Your Hyperliquid Year Filed Right

Flat-fee preparation for DeFi and perps traders: on-chain history reconstructed, framework documented, airdrop income handled, and every off-ramp dollar explained before the IRS asks.

Book a callFAQ: Hyperliquid Taxes

Frequently Asked Questions

Does Hyperliquid report to the IRS?

No. Hyperliquid is non-custodial and non-KYC, issues no tax forms, and files nothing with the IRS. After the DeFi broker rule was repealed in April 2025, non-custodial platforms have no 1099-DA obligation. Your activity is still fully taxable and permanently recorded on-chain.

Do you have to pay taxes on Hyperliquid if you never withdraw?

Yes. Tax attaches when you close positions, receive funding or airdrops, or swap tokens, not when dollars reach your bank. Never withdrawing changes your paperwork trail, not your tax bill.

Is Hyperliquid legal to use in the US?

Hyperliquid geo-blocks US users at the website level and its terms exclude US persons, though the underlying protocol is permissionless. That's a platform and regulatory question outside tax law. The tax rule is unaffected: US taxpayers owe tax on Hyperliquid profits regardless of how access happened.

How are Hyperliquid perpetual futures taxed?

There's no direct IRS guidance. The common conservative position treats each closed position as short-term capital gain or loss on Form 8949. An alternative framework characterizes perps as swaps producing ordinary income. Pick one, document it, and apply it consistently across years.

Do Hyperliquid perps qualify for Section 1256 60/40 treatment?

No. Section 1256 requires trading on a CFTC-designated or equivalent regulated exchange, and Hyperliquid is not registered with the CFTC in any capacity. The 2026 approval of onshore US perps does not change the analysis for offshore, unregistered venues. Do not use Form 6781.

How are Hyperliquid funding payments taxed?

Unsettled. The conservative approach reports net funding received as ordinary income; funding paid is generally a disallowed investment expense for non-trader individuals. Some filers net funding into position P&L or use swap-style annual netting. Whichever method you choose, document it and stay consistent.

Was the HYPE airdrop taxable?

Yes. The November 2024 genesis distribution was ordinary income at fair market value when you gained the ability to transfer or sell the tokens. That value became your cost basis, and later sales produce separate capital gains or losses. If it's missing from your 2024 return, amend proactively.

Are Hyperliquid points taxable?

Generally not while they're just points, because they have no transferable value. Income arises when points convert into an actual token you control, taxed as ordinary income at the token's value on receipt. Keep records of conversion dates and values.

Does the wash sale rule apply to Hyperliquid trades?

Under current law, no. The wash-sale rule covers securities, and crypto is treated as property, so crypto losses are generally deductible even with quick repurchases. Legislation extending the rule to digital assets keeps being proposed, so confirm the current-year status before harvesting losses.

Do I need to file an FBAR for Hyperliquid?

Generally no for a self-custodied wallet, which is not an account at a foreign financial institution, and current FinCEN guidance does not treat crypto-only foreign accounts as FBAR-reportable. The rules have been slated to change, and offshore centralized exchange accounts are a different analysis, so confirm with your preparer.

What tax forms do I use to report Hyperliquid?

Form 8949 and Schedule D for capital dispositions (perp P&L under the conservative framework, spot trades, HYPE sales), Schedule 1 for ordinary income (airdrops, points conversions, staking, vault yield, net funding), and a Yes on the Form 1040 digital asset question. Not Form 6781.

Can the IRS see my Hyperliquid wallet?

Yes, eventually. Everything is public on-chain forever, blockchain analytics firms map wallet clusters for the IRS, and any withdrawal to a KYC'd exchange links the wallet to your identity and generates a 1099-DA. The safe assumption is full future visibility.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

The Ultimate Guide to Crypto Tax (2026 Edition)

The most comprehensive crypto tax guide online, written by a CPA who files 500+ crypto returns a year. Every taxable event, form, strategy, and 2026 update.

Polymarket Taxes (2026): A CPA's Guide to Reporting When There's No 1099

Polymarket sends no 1099, but your winnings are still taxable. A CPA explains the forms, the four tax treatments, and the USDC layer, with worked numbers.

Prediction Market Taxes (2026): How Kalshi, Polymarket, Robinhood and Every Major Platform Gets Taxed

How prediction market taxes work on Kalshi, Polymarket, Robinhood and more. A CPA splits platforms by settlement type and shows exactly what to report.