Crypto Scam Tax Deduction (2026): A CPA's Guide to Writing It Off

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓✓IRS Chief Counsel Memo 202511015 (Q1 2025) appears to support that crypto scam losses may qualify as deductible under §165(c)(2), provided three conditions are satisfied.

- ✓The three tests are simple. The loss must qualify as theft under state law, must come from a profit-motivated transaction, and must be claimed in the year you discovered it with no reasonable prospect of recovery.

- ✓Pig butchering, phishing, compromised account scams, and fake NFT minting platforms all typically qualify. Romance scams, ransoms, and gift transfers do NOT qualify (no profit motive).

- ✓These losses are reported on Form 4684 Section B, flow to Schedule A as an itemized deduction, and reduce your AGI dollar for dollar. Any excess loss carries forward under §172.

- ✓✓Most traditional CPAs refuse to file these even with clear IRS guidance. If you have a material loss, you need a crypto tax CPA who understands the memo and the §165(c)(2) framework.

- ✓✓Critical detail: your deduction is limited to your cost basis, not the inflated value the scam showed you on screen. If you bought $80,000 of crypto, sent it to a fake exchange when valued at $200,000, and saw the asset appreciate to $400,000 on the fake exchange, your deduction is still only $80,000.

“This guide has been reviewed for accuracy by Leanne Grant, Enrolled Agent, specializing in cryptocurrency tax compliance.”

Crypto scams are as rampant as ever. I have multiple clients per week asking me the same question: "I got scammed. Can I get any tax benefit for the loss?"

My answer is always: potentially, let's talk through the facts.

The frustrating part is that most CPAs still tell their clients no. Even after the IRS releases a memo laying out the IRS interpretation of the §165(c)(2) framework, traditional preparers refuse to file the deduction. Their clients leave significant tax savings on the table.

I am hoping this guide can help provide insight as to when a scam victim can substantiate a tax loss that can ease some tax burden surrounding money lost. It covers the five scam types I see most often, the IRS guidance that finally provided some clarity (Chief Counsel Memo 202511015, released in Q1 2025), how to actually report the loss on Form 4684, and the documentation you need to make the position defensible.

If you lost crypto to a scam and your CPA told you it is not deductible, contact us before ruling out your options.

The Headline: Yes, Crypto Scam Losses Are Deductible in 2026

Before the IRS released Chief Counsel Memo 202511015 in Q1 2025, the tax treatment of crypto scam losses was genuinely vague. Practitioners argued about whether scams qualified as theft, whether the loss should be ordinary or capital, and which form to file it on. Some CPAs claimed the deductions anyway. Most refused.

The IRS memo provided much of the clarity we were looking for.

Under §165(c)(2), a crypto loss from a scam is deductible as a theft loss when three conditions are met. I will walk through each one below with the facts that matter, but here is the summary:

- The loss qualifies as theft under your state's law. This means a criminal act such as fraud, swindling, or false pretenses. The taxpayer must show the property was illegally taken and there was criminal intent.

- The transaction was profit-motivated. You sent the crypto intending to maintain or grow an investment. You were not gifting it, paying a ransom, or sending it to a romantic interest.

- The loss is claimed in the year you discovered it with no reasonable prospect of recovery. Not when you sent the crypto, but rather the year you realized it was not recoverable.

That is the basic framework. If your situation checks all three boxes, the loss may qualify for a deduction. The amount is limited to your cost basis (more on that below) and it gets reported on Form 4684 Section B.

The rest of this article is the practical version: which scams qualify, which do not, how to fill out the form, and how to keep the IRS happy if they ever ask.

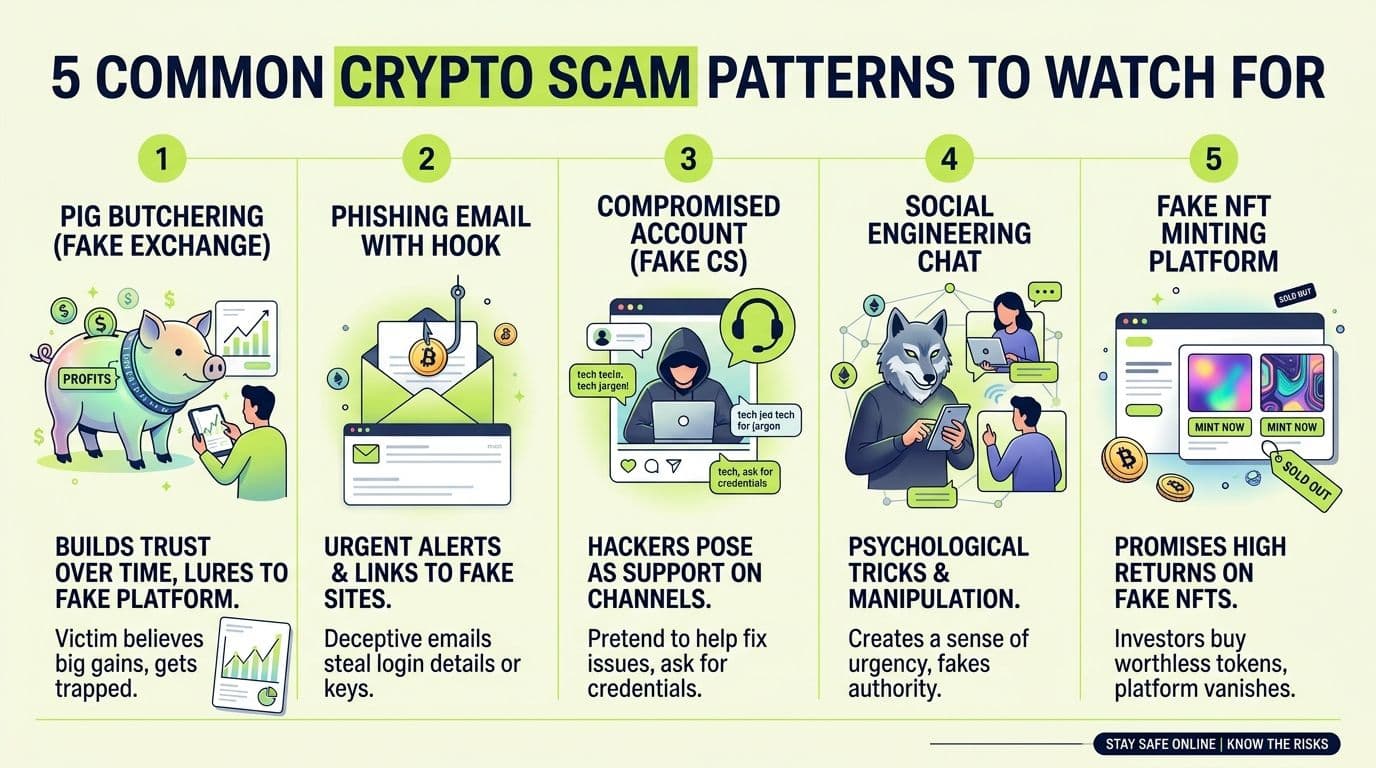

The Five Scam Types I See Most Often

Across hundreds of client engagements, almost every crypto scam I see falls into one of five patterns. Each one I can typically get comfortable that the client reasonably qualifies for the §165(c)(2) deduction. The names of the scams matter less than the underlying facts.

1. Pig Butchering Scams

This is the most common scam I see, by a wide margin.

The taxpayer invests crypto onto a fake exchange. The exchange promises high yields through leveraged staking, proprietary trading algorithms, or "insider" signals. The taxpayer keeps increasing their investment, watching big numbers grow on screen. When they try to withdraw, the withdrawal fails.

The fake exchange then claims there are "fees" or "taxes" or "liquidity requirements" that must be paid before withdrawal is allowed. They may even send a small distribution to keep the taxpayer engaged and convinced the platform is real. Eventually, once the operators believe they have extracted everything they can, the exchange disappears. Login no longer works. The "customer service" representative stops responding.

The cost basis is whatever crypto the taxpayer actually sent to the fake exchange. The fabricated balance on the screen is irrelevant for tax purposes.

2. Phishing Wallet Attacks

The taxpayer receives an email, text, or DM claiming their exchange account or wallet has been compromised. The message includes a link to a fake login page that mimics the real exchange's branding. The taxpayer enters their credentials. The attacker uses those credentials to drain the actual account.

Variations include fake Ledger updates, fake MetaMask "security alerts," and fake exchange password reset emails. The end result is the same: the attacker takes the crypto.

This is straightforward theft. The §165(c)(2) deduction is typically available as long as the underlying crypto was held for investment (which it almost always is).

3. Compromised Account Scams (Fake Customer Service)

A fake customer service representative contacts the taxpayer, claiming to be from an exchange where the taxpayer holds an account. The "rep" warns that the account has been compromised and instructs the taxpayer to "transfer assets to a new, secure wallet" for safekeeping.

Once the transfer happens, the funds are gone.

These scams often combine spoofed phone numbers, fake support tickets, and urgency tactics. The taxpayer is in panic mode and complies before verifying. The deduction is defendable because the loss is plainly theft under state law and the underlying crypto was and investment held for profit.

4. Social Engineering Scams (Fake Investment Platforms)

The taxpayer meets someone online they are attracted to or who positions themselves as a successful crypto investor or mentor. After weeks or months of conversation and trust-building, the contact introduces a "crypto investment opportunity." The taxpayer believes they are investing in a real crypto platform. Once funds are transferred, they disappear, or the situation morphs into a pig butchering scenario.

The key tax question for these scams is whether the loss was profit-motivated or personal.

If the taxpayer sent crypto because they believed they were investing in a real platform, the §165(c)(2) deduction is available. If the taxpayer sent crypto as a romantic gift or because the other person asked for help, the deduction is generally not available (failure of the profit-motive test).

The line is sometimes blurry, and the facts need to be made very clear and supportable.

5. Fake NFT Minting Platforms

The taxpayer wants to create and sell NFTs. They find a website claiming to help creators mint and sell NFTs in exchange for a fee paid in crypto. After sending the crypto, the platform appears to generate the NFTs and even shows successful sales with large profits.

The taxpayer keeps minting more, watching their fake balance grow. When they try to withdraw the proceeds, the platform either denies the withdrawal, demands additional "gas fees" or "platform fees" or "tax payments," or imposes increasingly tight limits.

Eventually it becomes obvious: the NFTs were never actually sold, the balances were fabricated, and every dollar of crypto sent to the platform is gone.

The deductible loss is the cost basis of the crypto the taxpayer paid the fake platform. The fake "sale proceeds" displayed on screen never existed and are not relevant to the tax calculation.

The IRS Unlock: Chief Counsel Memo 202511015

In Q1 2025, the IRS Office of Chief Counsel released Memorandum 202511015. This is the single most important development in crypto theft loss.

The memo clarifies that scam losses on crypto qualify for the §165(c)(2) deduction for losses arising from a "transaction entered into for profit, though not connected with a trade or business."

This matters for two reasons:

First, it bypasses the TCJA suspension. From 2018 through 2025, the Tax Cuts and Jobs Act suspended personal casualty and theft losses under §165(c)(3). Many practitioners assumed crypto scam losses fell under §165(c)(3) and were therefore non-deductible. The memo confirms they fall under §165(c)(2) instead, which was never suspended.

Second, it gives a clear path to report the loss. Before the memo, even practitioners who believed the loss was deductible disagreed on how to file it (Schedule D capital loss, Form 4684, miscellaneous itemized deduction, etc.). The memo confirms Form 4684 Section B is the correct path.

I will not pretend the memo is binding precedent. Chief Counsel Memoranda are advisory and do not have the force of regulation. But they reflect the IRS's official position, and tax courts give them weight. In practice, this memo is a yellow light informing taxpayers to “proceed with care and caution.”

The Three Tests You Must Pass

To claim the deduction under §165(c)(2), your loss must satisfy all three of these tests. Miss any one and the deduction is not available.

Test 1: Theft Under State Law

The loss must qualify as theft under your state's criminal law. This includes:

- Fraud

- Swindling

- False pretenses

- Embezzlement

- Larceny by trick or deception

In practice, virtually every crypto scam I have seen meets this standard. Pig butchering, phishing, fake exchanges, fake NFT platforms, compromised account schemes -- all of them involve criminal intent and unlawful taking of property under any state's definition of theft.

The few situations that fail this test: voluntary transfers that turned sour without criminal intent (a project failed without fraud), bad investments in legitimate-but-failed projects (project went bust but no theft), and personal disputes that do not rise to criminal fraud.

Test 2: Profit-Motivated Transaction

The taxpayer must have intended to maintain or grow investment crypto when they sent the funds to the scam.

This passes when:

- You sent crypto to what you believed was a real exchange or investment platform

- You sent crypto to mint and sell NFTs as an investment activity

- You sent crypto to what you believed was a legitimate trading or staking opportunity

This fails when:

- You sent crypto as a gift to a romantic partner (romance scams)

- You sent crypto to pay a ransom

- You sent crypto as a personal gift, donation, or to help someone

Romance scams are the most painful category. The victim often feels they were investing through the relationship, but the IRS and courts treat romance-driven transfers as personal, not investment. The deduction is generally not available.

If your facts are mixed (you were in a relationship with the scammer AND they introduced a "platform"), get a CPA involved before assuming either yes or no.

Test 3: Year of Discovery, No Reasonable Prospect of Recovery

You claim the loss in the tax year you discovered the scam with no reasonable prospect of recovery,not the year you sent the crypto.

If you sent crypto across 2024 and 2025 and only realized in 2025 that the withdrawal was permanently impossible, the entire loss is a 2025 loss for tax purposes.

"No reasonable prospect of recovery" is a facts-and-circumstances test. If law enforcement is actively investigating and there is a real chance of seized funds being returned, you may need to wait. If the operators are anonymous and gone, the prospect of recovery is essentially zero, and you can claim the loss in the year you discovered it.

Pro Tip

**Document the discovery date.** Save the email or screenshot showing the withdrawal denial. Save the moment the platform went dark. Save your communication with the scammer after the failure. The discovery date determines what year the deduction belongs in, and the IRS will sometimes question it.

How to Actually Report The Loss on Your Tax Return: Form 4684 Section B → Schedule A → 1040

Here is the exact reporting flow for a §165(c)(2) crypto scam loss:

Step 1: Form 4684, Section B

Form 4684 is the Casualties and Theft Losses form. Section B is specifically for "Business and Income-Producing Property" theft losses, which is where §165(c)(2) profit-motivated losses go.

On Section B, you report:

- The property stolen (crypto, by type and amount)

- The cost basis (what you actually paid)

- The fair market value before the theft (often equal to or higher than basis)

- The fair market value after the theft (zero, because it is gone)

- Any insurance or expected recovery (usually zero)

- The resulting loss

Key point: your deduction is limited to your cost basis. If you sent 2 ETH that cost you $4,000 to a pig butchering exchange that showed a balance of $80,000 before vanishing, your loss is $4,000. The fake balance is irrelevant.

Step 2: Schedule A (Itemized Deductions)

The loss from Form 4684 flows to Schedule A as an itemized deduction. It adds to the same deduction category that includes mortgage interest, state and local taxes (subject to SALT cap), and charitable contributions.

You must itemize to use this deduction. If your standard deduction is larger than your total itemized deductions including the scam loss, the deduction does not help you.

Step 3: Form 1040

Total itemized deductions on Schedule A flow to Form 1040 and reduce your adjusted gross income dollar for dollar.

Step 4: §172 Carryforward (If the Loss Exceeds Income)

If your scam loss is larger than your taxable income for the year, the excess generates a net operating loss (NOL) under IRC §172.

Post-2017 NOLs carry forward indefinitely (no expiration) and can offset up to 80% of taxable income in each future year. This is a meaningful benefit for large losses. A taxpayer who lost $500,000 to a scam in a year they earned $200,000 still gets full value from the deduction over time.

What If Your CPA Says No?

I see this constantly. A taxpayer brings their scam loss to their long-time CPA. The CPA says "we cannot deduct that, the rules are too vague" or "the IRS will audit you." Sometimes they cite outdated guidance from before Chief Counsel Memo 202511015. Sometimes they simply admit they are not well versed on the issue.

The result is the same: the taxpayer leaves $20,000, $50,000, or $200,000 in tax savings on the table.

There are real reasons traditional CPAs are cautious. The deduction can attract IRS scrutiny. Some taxpayers do misuse it. The penalties for an aggressive position that does not hold up can be meaningful. A CPA who has not actually researched the area is making a defensible choice when they decline to file the deduction.

But the law is on the taxpayer's side when the facts are clean. Chief Counsel Memo 202511015, the §165(c)(2) framework, the Form 4684 Section B reporting flow -- they are all relatively clear. The only question is whether your CPA has read the guidance and is comfortable defending the position given the fact pattern.

Common Mistakes That Wreck Otherwise Valid Claims

I see these errors constantly. Any one of them can convert a clean deduction into a contested IRS adjustment.

1. Deducting fake on-screen value instead of cost basis. This is the #1 error. Your deduction is what you actually paid for the crypto you sent, not the appreciated value at the time it was invested or the inflated number the scam displayed.

2. Claiming the loss in the wrong year. The deduction belongs in the year you discovered the scam with no reasonable prospect of recovery, not the year you first sent crypto.

3. Filing the wrong form. Scam losses go on Form 4684 Section B, not Schedule D, not a generic itemized miscellaneous deduction. Using the wrong form can delay processing and generate additional IRS scrutiny.

4. Skipping the police or IC3 report. Not technically required by the IRS, but the absence of any contemporaneous filing makes the theft element harder to defend. File something within days of discovery.

5. Claiming a romance scam under §165(c)(2). The profit-motive test almost always fails. Look for other paths, but do not claim a §165(c)(2) deduction on a clear romance scam without strong supporting facts.

6. No supporting memo. For losses above $10,000, your return should be accompanied by (or your preparer should have on file) a memo establishing each §165(c)(2) element with citations to Chief Counsel Memo 202511015 and the underlying state-law theft definition. If the IRS examines, this memo is your first line of defense.

7. Forgetting the §172 carryforward. If the loss exceeded current-year income, the excess carries forward indefinitely. Make sure your preparer tracks the NOL and uses it in future years.

8. Ignoring state tax conformity. Some states fully conform to federal §165(c)(2) and give you the same deduction. Others have limitations. Always check the state-level treatment before assuming the deduction works identically.

When You Need a Crypto Tax CPA

If you lost crypto to a scam, you need professional help. The §165(c)(2) framework is straightforward in theory, but the practical execution (cost basis documentation, memo preparation, state conformity analysis, §172 carryforward planning) is where most returns go wrong.

Specifically, work with a crypto tax CPA if:

- Your loss was more than $10,000

- The facts are mixed (romance + investment, multiple transfers across years, partial recovery)

- Your current CPA has refused to file the deduction

- You need to amend a prior-year return to claim a loss you missed

- The scam loss is large enough to generate a §172 carryforward

- The state-level analysis is non-trivial (multi-state filer, state of residence does not conform to §165(c)(2))

The cost of getting this right is meaningfully smaller than the tax savings on a properly claimed loss.

Lost Crypto to a Scam? Let's Talk.

If you were a victim of a crypto scam in 2024, 2025, or 2026, you may have a significant tax deduction available under IRS Chief Counsel Memo 202511015 and §165(c)(2). I have filed dozens of these returns and can produce a defensible position memo. Bring me your facts and I will tell you straight whether the deduction works.

Talk to GarrettFree 15 minute call. No commitment.

Go Deeper on Each Scam Type

Each of the five scams below has its own detailed guide covering how it works, the red flags, and exactly how the theft-loss deduction applies to that fact pattern.

- Pig butchering scam: how to write off the loss

- Crypto phishing scam: claiming the wallet-drain loss

- Fake crypto customer service scam: how to deduct the loss

- Fake crypto investment platform scam: deducting the loss

- Fake NFT minting scam: how to write off the loss

Frequently Asked Questions

Can I deduct crypto I lost to a scam on my 2025 or 2026 tax return?

Yes, in most cases. IRS Chief Counsel Memo 202511015, released in Q1 2025, made the framework explicit. Crypto scam losses qualify for a theft deduction under §165(c)(2) if three conditions are met: the loss qualifies as theft under your state's law, the transaction was profit-motivated (you intended to grow or maintain investment crypto), and the loss is claimed in the year you discovered it with no reasonable prospect of recovery. Pig butchering, phishing wallet attacks, fake exchanges, fake NFT minting platforms, and compromised account scams all typically qualify.

What is IRS Chief Counsel Memo 202511015 and why does it matter?

It is the guidance the IRS released in Q1 2025 that finally clarified how crypto scam losses are treated for tax purposes. Before this memo, the rules were vague and many CPAs refused to claim these losses because the reporting position was unclear. The memo confirms scam losses are deductible under §165(c)(2) as long as the three conditions are met. This is the single most important development in crypto loss taxation in years, and almost no other content on the internet covers it correctly.

What types of crypto scams qualify for a §165(c)(2) deduction?

The five most common qualifying scam types we see: (1) Pig butchering scams (fake exchanges promising high yields), (2) Phishing wallet attacks (credential theft followed by wallet drains), (3) Compromised account scams (fake customer service rep asks you to transfer assets to a 'secure' wallet), (4) Social engineering scams that include a fake investment platform, and (5) Fake NFT minting platforms that fabricate sales then demand more crypto to withdraw fake balances. All five involve criminal intent, state-law theft, and profit motive when the victim was trying to grow their crypto.

What does NOT qualify as a deductible scam loss?

Losses that fail the profit-motivated requirement do not qualify. This includes: romance scams where the taxpayer was sending crypto to someone they were emotionally involved with (the courts treat this as personal, not investment), ransomware payments, gift transfers that turned out to be scams, and any situation where the taxpayer cannot show they intended to maintain or grow investment crypto. The key question is always: were you trying to invest, or were you trying to help, gift, or be in a relationship?

What tax year do I claim the loss in?

You claim the loss in the tax year you discovered the scam with no reasonable prospect of recovery. If you sent crypto in 2024 and 2025 and only realized in 2025 that it was a scam (withdrawal denied, exchange went dark), the entire loss is claimed on your 2025 return. The 'discovery year' rule is in the IRS memo and is non-negotiable. If you discovered the scam in 2026, you claim it on your 2026 return regardless of when the deposits happened.

Why do most CPAs refuse to claim these scam loss deductions?

Three reasons: (1) The rules were genuinely vague before Chief Counsel Memo 202511015, so many practitioners learned to say no out of caution. (2) Scam loss claims can attract IRS scrutiny because some taxpayers misapply the rules or inflate the loss above their cost basis. (3) Most CPAs do not specialize in crypto and have not read the memo or the §165(c)(2) framework. The fix is to work with a CPA who has actually filed these returns and can produce a defensible memo to support the position.

Will claiming a crypto scam loss trigger an IRS audit?

It can attract scrutiny, especially for larger losses. The IRS is aware that some taxpayers misuse these deductions. The good news: if your loss is real, properly documented, and reported correctly under Chief Counsel Memo 202511015 and §165(c)(2), the position is defensible. The key is documentation: blockchain evidence of transfers, communications with the scammer, police or FBI IC3 reports, screenshots of the fake platform, and a CPA-prepared memo establishing each element of the deduction.

What documentation do I need to claim a crypto scam loss?

At minimum: (1) Records of the original crypto purchase (cost basis), (2) Blockchain transaction hashes of every transfer to the scam, (3) Screenshots of the fake exchange, platform, or wallet showing your balance, (4) Communications with the scammer (Telegram, WhatsApp, email), (5) A police report or FBI Internet Crime Complaint Center (IC3) filing, (6) Documentation of when you discovered the scam and your attempts to recover funds, (7) A CPA-prepared memo establishing the §165(c)(2) elements. The more documentation, the stronger the position.

What if my scam loss is bigger than my income that year?

Under §172, any portion of the loss that exceeds your taxable income that year carries forward to future years. The carried-forward loss can offset up to 80% of taxable income in each future year until the loss is fully used. There is no fixed expiration on §172 net operating loss carryforwards generated after 2017. This is a significant benefit for large losses, since you do not lose the deduction just because your current year income was lower than the loss.

What if I lost crypto to a romance scam? Can I still deduct it?

Probably not under §165(c)(2). The IRS memo specifically excludes romance scams from the profit-motivated requirement. The argument is that you sent the crypto as part of a personal relationship, not as an investment. There may be other arguments to explore (capital loss treatment if the transaction technically completed, abandonment loss in narrow cases), but the §165(c)(2) theft deduction is generally not available. This is a heartbreaking result for victims and a place where we sometimes spend hours looking for any defensible path. Bring the facts to a crypto tax CPA before assuming there is no deduction.

Can I amend a prior-year return to claim a scam loss I missed?

Yes, within the statute of limitations (generally 3 years from the original filing date or 2 years from when you paid the tax, whichever is later). If you discovered a scam in 2023 or 2024 and never claimed the deduction, you can typically file an amended return on Form 1040-X to claim it. The same §165(c)(2) framework and Chief Counsel Memo 202511015 guidance apply. Get a CPA to prepare the amendment with a supporting memo before filing.

Do state taxes treat scam losses the same way?

It varies by state. Some states fully conform to federal §165(c)(2) treatment, so you get the same deduction at the state level. Other states have their own rules. A few states do not allow itemized deductions at all, which can limit the state-level benefit. Always check your specific state's conformity rules, or have a CPA who handles your state run the analysis. For California, New York, and other major filing states, the rules vary meaningfully.

Do I need to file a police report to claim the deduction?

Not legally required by the IRS, but strongly recommended. A police report (or FBI Internet Crime Complaint Center / IC3 filing) is one of the cleanest pieces of evidence supporting that a state-law theft occurred. The IRS does not require it, but if your return is examined, having a contemporaneous police report makes the position significantly more defensible. We recommend filing one within days of discovering the scam, even if you do not expect law enforcement to recover the funds.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Pig Butchering Scam (2026): How to Write Off the Loss on Your Taxes

A pig butchering scam can wipe out a life savings. The lesser-known part: that loss is often deductible. Here is how the §165(c)(2) theft-loss rules apply to pig butchering, and how to actually claim it.

Crypto Phishing Scam (2026): Claiming the Wallet-Drain Loss on Your Taxes

A crypto phishing scam can empty a wallet in one signature. If the drained crypto was held for investment, that loss is often deductible. Here is how the theft-loss rules apply and how to claim it.

Fake Crypto Investment Platform Scam (2026): Deducting the Loss

A fake crypto investment platform shows you climbing profits you can never withdraw. If you invested for profit, that loss is often deductible. Here is how the theft-loss rules apply.