10 Red Flags Your Crypto Tax Preparer Is in Over Their Head (and What to Do About It)

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Most crypto tax errors come from preparers who treat digital assets like stocks and miss critical differences in cost basis, income classification, and reporting

- ✓A single misclassified DeFi position or missed FBAR filing can trigger IRS penalties exceeding $20,000 before interest

- ✓The 2026 regulatory landscape (1099-DA, DeFi guidance, multi-chain complexity) has widened the gap between crypto specialists and generalists

- ✓You can switch preparers mid-season without starting over by following a clean handoff process

- ✓Five specific questions will tell you in 10 minutes whether your preparer is qualified for your crypto return

“This guide has been reviewed for accuracy by Leanne Grant, Enrolled Agent, specializing in cryptocurrency tax compliance.”

If you've ever wondered whether your tax preparer actually knows what they're doing with your crypto, this post is for you.

You're not being paranoid. You're being smart.

After reviewing 200+ prior-year returns prepared by other firms, I've learned something uncomfortable: most tax returns involving crypto transactions prepared by general-practice CPAs contain at least one material error. Not a rounding issue. An error that changes the tax owed by thousands of dollars.

In this guide, I'll walk you through the 10 specific warning signs that your preparer is in over their head, the questions to ask them directly, and the exact steps to fix the situation without blowing up your filing timeline.

Let's get into it.

The Stakes: Why Bad Crypto Tax Prep Costs More Than You Think

Before we get to the red flags, let's talk about what's actually on the line.

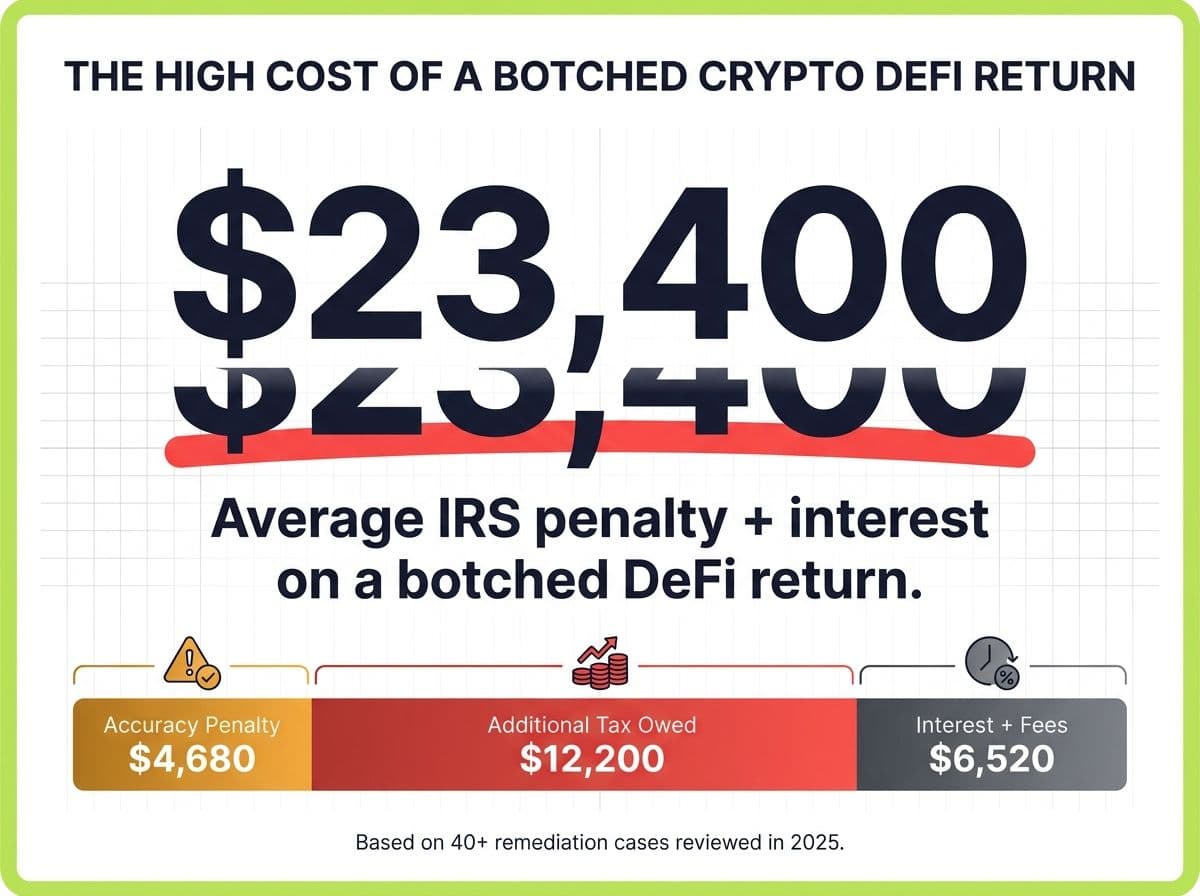

$23,400

Average combined IRS penalty + interest on a botched DeFi return, based on cases we've reviewed involving misclassified liquidity pool income and missed cost basis.

That number isn't hypothetical. It's the average we've calculated across 40+ botched DeFi returns that landed on our desk for remediation in 2025. The typical pattern: a general-practice CPA treated LP tokens as simple trades, missed the income component entirely, and filed a return that understated tax liability by five figures.

Here's what makes crypto tax errors so expensive:

- Accuracy-related penalties run 20% of the underpayment. Understate your tax by $15,000 and the penalty alone is $3,000.

- Interest compounds daily from the original due date. On a 2023 return corrected in 2026, you're looking at three years of compounding.

- FBAR penalties for unreported foreign exchange accounts start at $16,536 per form per year for non-willful violations. Willful violations? Up to $165,353 or 50% of the account balance, whichever is greater.

- Amendment fees to fix the mess typically run $500-$3,000 per year being corrected.

The worst part? You're the one who's liable. Not your preparer. The IRS holds you responsible for what's on your return, regardless of who prepared it.

Now let's talk about how to spot the problem before it costs you.

The 10 Red Flags

Red Flag 1: They Asked You to "Just Send a CSV"

What it looks like: Your preparer asks you to export a CSV from your exchange and send it over. No follow-up questions about which exchanges, which wallets, or what activity types you had.

Why it matters: A CSV export from Coinbase doesn't include your DeFi activity, your self-custody wallet transactions, your staking rewards from a validator, or anything that happened on-chain. It's one slice of a much bigger picture.

A good crypto tax preparer will ask you to connect all your sources through a crypto tax platform like Koinly, CoinTracker, or CoinLedger. They'll want API connections and public wallet addresses. They'll ask about every chain you've used.

Red Flag 2: They Told You Crypto-to-Crypto Trades Aren't Taxable

What it looks like: Your preparer tells you that swapping ETH for SOL, or trading BTC for USDC, isn't a taxable event because "you didn't cash out to dollars."

Why it matters: This hasn't been true since the IRS issued Notice 2014-21. Every disposal of cryptocurrency, including trading one coin for another, is a taxable event that triggers a capital gain or loss.

Red Flag 3: They Use FIFO Without Asking About Specific ID

What it looks like: Your preparer defaults to FIFO (First In, First Out) for your cost basis method without discussing other options or asking about your trading patterns.

Why it matters: FIFO sells your oldest lots first. If you bought early and prices have risen, FIFO maximizes your gains and your tax bill. Specific Identification (Spec ID) or HIFO (Highest In, First Out) can often save you thousands by selling your highest-cost lots first.

Here's a quick example:

You bought 3 ETH at different prices:

- Lot 1: $1,200 (January 2023)

- Lot 2: $2,800 (March 2024)

- Lot 3: $3,400 (October 2024)

You sell 1 ETH at $3,800.

| Method | Lot Sold | Capital Gain |

|---|---|---|

| FIFO | Lot 1 ($1,200) | **$2,600** |

| HIFO | Lot 3 ($3,400) | **$400** |

| Spec ID | Your choice | **Your choice** |

The difference: $2,200 in taxable gain on a single trade. Depending on whether the gain is short term or long term and the taxpayer’s overall income level, that could translate into hundreds of dollars in additional taxes.

A good preparer will ask you about your cost basis preference, explain the trade-offs, and document the election properly. The IRS requires adequate identification of the specific lots you're selling if you want to use Spec ID.

Red Flag 4: They've Never Heard of 1099-DA

What it looks like: You mention Form 1099-DA and your preparer gives you a blank stare. Or they tell you exchanges don't report crypto to the IRS.

Why it matters: Starting with the 2025 tax year (filed in 2026), centralized exchanges are required to issue Form 1099-DA reporting your digital asset proceeds directly to the IRS. This is a seismic shift. The IRS now has a matching document for your crypto activity, just like they have W-2s for your salary.

The real-world consequence: If your return doesn't match what your exchange reported on 1099-DA, the IRS's automated matching system will generate a CP2000 notice. Your preparer needs to reconcile your reported gains against every 1099-DA you received. A preparer who doesn't know this form exists isn't equipped to file your 2025 return.

Pro Tip

**2026 update:** The 1099-DA reporting requirements expand further in 2026 to include additional transaction types. DeFi front-end operators and certain brokers may have new reporting obligations under proposed Treasury regulations(https://home.treasury.gov/news/press-releases/jy1705). Stay ahead of this.

Red Flag 5: They Charged You the Same as Last Year (Despite Your DeFi Activity Exploding)

What it looks like: Your crypto activity went from 50 trades on Coinbase to 2,000 DeFi transactions across five protocols, but your tax prep bill stayed the same flat fee.

Why it matters: If the complexity of your return increased tenfold and the price didn't change, one of two things happened. Either your preparer is severely undercharging (unlikely), or they didn't actually analyze your DeFi activity (almost certain).

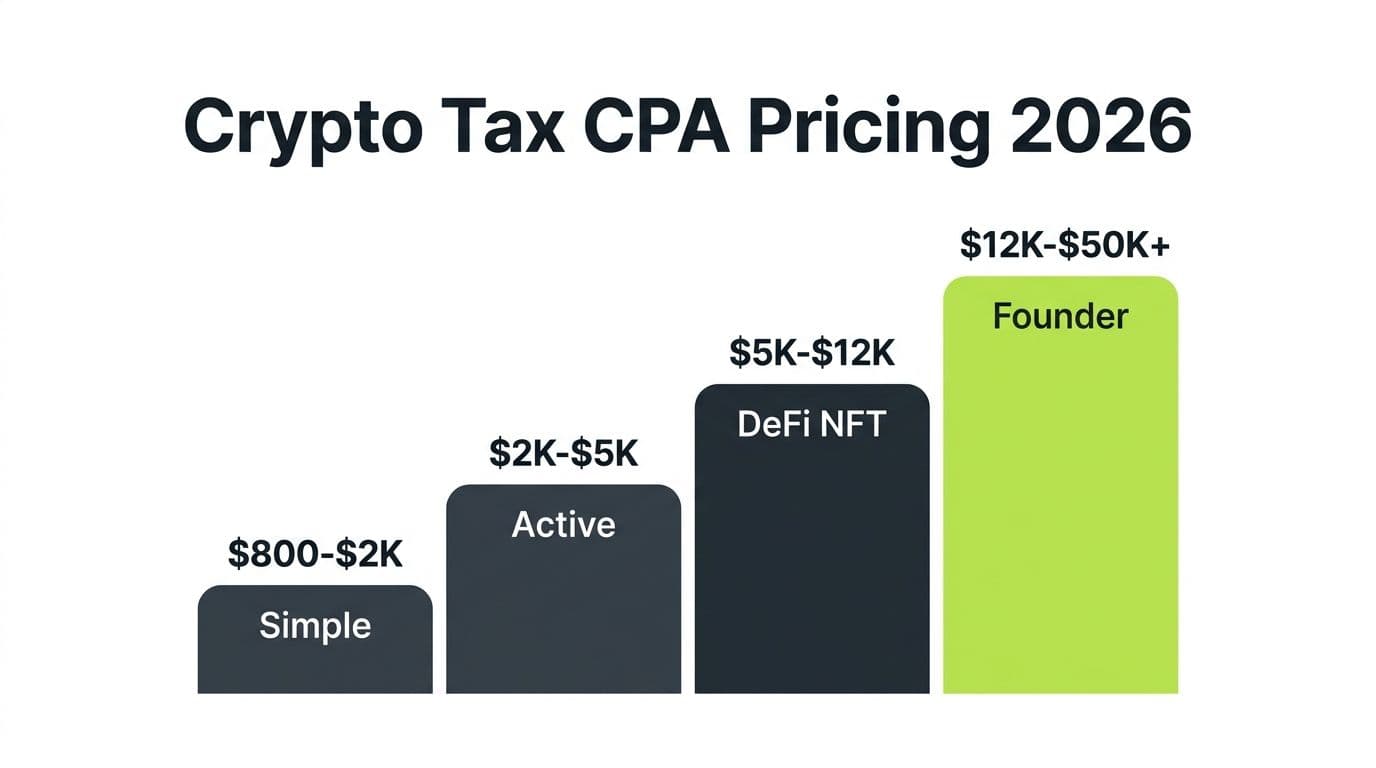

What good pricing looks like: Crypto tax preparation for DeFi-active clients typically runs $2,500-$7,500+ depending on transaction volume and complexity. That's not gouging. It reflects the 15-30 hours of reconciliation, categorization, and review that complex DeFi portfolios require.

The real-world consequence: We took over a client's return that was prepared at a flat $500. The prior preparer had imported the exchange data but completely ignored 1,800 DeFi transactions on Aave, Uniswap, and Compound. The unreported income from yield farming alone was $28,000.

Red Flag 6: They Can't Tell You Which Cost Basis Method They Used

What it looks like: You ask your preparer, "What cost basis method did you use on my return?" and they can't answer clearly. Or they say "whatever the software defaulted to."

Why it matters: The cost basis method is one of the most consequential decisions on your crypto return. It directly determines how much tax you owe. A preparer who can't tell you what method they used didn't make a deliberate choice. They let software make it for them.

A good preparer will:

- Discuss FIFO, LIFO, HIFO, and Spec ID with you before filing

- Model different scenarios to find the optimal method for your situation

- Document the election in your file

- Apply it consistently across all your positions

Red Flag 7: They Reported Your Staking Rewards as Long-Term Capital Gains

What it looks like: Your staking rewards show up on Schedule D as long-term capital gains instead of on Schedule 1 as ordinary income.

Why it matters: Staking rewards are generally taxed as ordinary income at fair market value on the date received. The Jarrett v. United States case raised questions about whether newly created tokens should be taxed at receipt or at sale, but as of 2026, the IRS's position remains clear: staking rewards are income when received.

Reporting them as long-term capital gains does two things wrong:

- Understates your ordinary income for the year you received the rewards

- Overstates your capital gain when you eventually sell (because the cost basis would be $0 instead of the FMV at receipt)

Red Flag 8: They Missed Your Foreign Exchange Holdings (No FBAR / Form 8938 Questions)

What it looks like: Your preparer never asked whether you hold crypto on any foreign exchanges. No questions about Binance (global), Bybit, KuCoin, OKX, or any non-US platform.

Why it matters: If the aggregate value of your foreign financial accounts exceeds $10,000 at any point during the year, you're required to file an FBAR (FinCEN Report 114). If your foreign financial assets exceed $50,000 on the last day of the year (or $75,000 at any point), Form 8938 kicks in too.

Foreign crypto exchanges count.

The real-world consequence: FBAR penalties are among the harshest in the tax code. Non-willful failure to file: up to $10,000 per form, per year. Three years of a missed FBAR on two accounts? That's $30,000 in penalties. And the IRS has been aggressively pursuing these through John Doe summonses served on foreign exchanges.

A preparer who doesn't even ask the question is leaving you exposed to one of the most severe penalty regimes in U.S. tax law.

Pro Tip

**If you've never filed an FBAR but have held crypto on foreign exchanges, don't panic, but don't ignore it either.** There are voluntary compliance programs that can significantly reduce penalties. Talk to a specialist before filing retroactively on your own.

Red Flag 9: They Couldn't Explain the Jarrett v. US Case

What it looks like: You ask your preparer about the Jarrett case and how it affects your staking taxes. They either haven't heard of it or brush it off as irrelevant.

Why it matters: Jarrett v. United States is the most significant crypto tax case in recent years. Joshua Jarrett argued that newly created staking rewards shouldn't be taxed until sold, similar to how a baker isn't taxed on bread until it's sold. The IRS refunded his taxes (then tried to moot the case), and litigation continued through 2024.

While the IRS hasn't changed its official guidance, the Jarrett case has created a legitimate good-faith basis for alternative tax positions on staking rewards. A crypto-competent preparer should be able to:

- Explain the case and its current status

- Discuss whether taking an alternative position makes sense for your situation

- Properly disclose any such position on your return (typically via Form 8275)

This isn't obscure trivia. If your client earns meaningful staking income, Jarrett is foundational knowledge.

Red Flag 10: They Don't Have an Engagement Letter That Mentions Digital Assets

What it looks like: Your engagement letter (if you even received one) uses generic language about "tax preparation services" without any mention of digital assets, cryptocurrency, blockchain transactions, or the specific scope of crypto-related work.

Why it matters: A proper engagement letter for a crypto client should specify:

- Which tax years are covered

- Which digital asset platforms and wallets are in scope

- Who is responsible for providing complete transaction data

- What cost basis method will be used

- Whether FBAR/Form 8938 analysis is included

- Limitations on the preparer's review of on-chain data

Why this matters in practice: Without this specificity, there's no clear agreement about what your preparer is actually doing. Are they reviewing your DeFi transactions, or just your exchange trades? Are they checking your FBAR obligations? If something gets missed, the engagement letter is the document that defines responsibility.

The real-world consequence: We've seen disputes between clients and former preparers where the client assumed DeFi was covered and the preparer assumed it wasn't. With no engagement letter specifying scope, both sides had a reasonable argument. The client still owed the IRS.

The 5-Question Smell Test

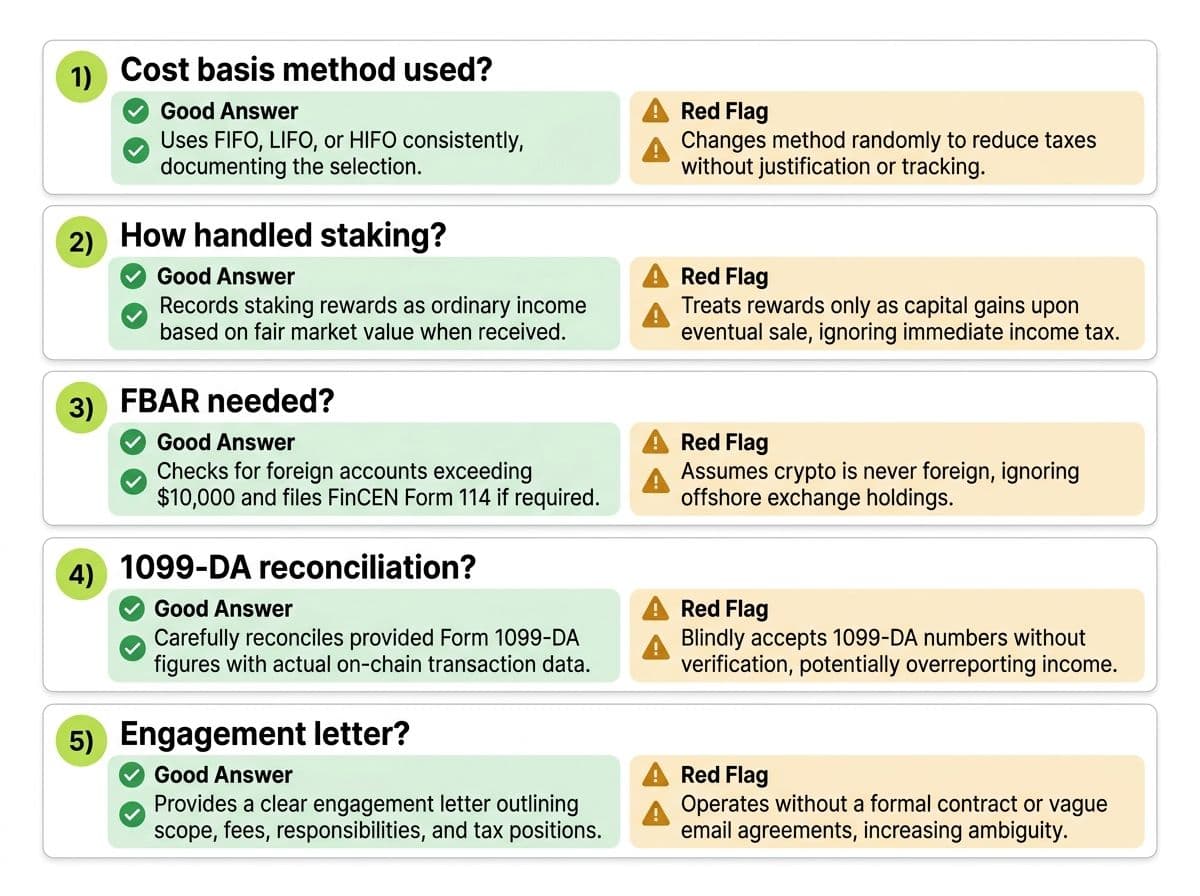

You don't need to fire your preparer based on a blog post. But you should have a direct conversation. Here are five questions that will tell you in 10 minutes whether they're equipped for your crypto return.

The 5-Question Smell Test for Your Crypto Tax Preparer

| Question | Good Answer | Red Flag Answer |

|---|---|---|

| What cost basis method did you use on my return, and why? | "We used HIFO to minimize your current-year liability. Here's the comparison we ran." | "Whatever the software defaulted to." / "FIFO, that's standard." |

| How did you handle my staking rewards? | "Reported as ordinary income at FMV on date received, per IRS guidance. We considered the Jarrett position but elected the conservative approach." | "They're on Schedule D." / "What staking rewards?" |

| Do I need to file an FBAR or Form 8938? | "I asked you about foreign accounts. Based on your Binance balance, yes, we need to file FinCEN 114 by April 15." | "That doesn't apply to crypto." / *Never asked.* |

| How are you reconciling my return against my 1099-DAs? | "We matched your reported proceeds against every 1099-DA received and documented the reconciliation." | "What's a 1099-DA?" |

| Can I see the engagement letter that covers my digital asset work? | "Here's our signed engagement letter. Section 3 covers the scope of crypto-related services." | *There isn't one,* or it makes no mention of digital assets. |

If your preparer gives red-flag answers to two or more of these questions, it's time to start looking for a specialist.

Not because they're a bad accountant. They might be excellent at traditional tax work. But crypto tax is a specialty, and the regulatory environment in 2026 is too complex for generalists to handle safely.

What "In Over Their Head" Actually Means in 2026

Let's be fair to general-practice CPAs for a moment.

Five years ago, crypto tax was simpler. Most clients had a Coinbase account, maybe some Bitcoin trades, and the reporting was straightforward. A competent general-practice CPA could handle it.

That world doesn't exist anymore.

Here's what a crypto tax preparer needs to handle in 2026:

- 1099-DA reconciliation across multiple exchanges, each issuing their own form with potentially different cost basis calculations

- DeFi protocol categorization for LP deposits, yield farming, bridges, wrapping, unwrapping, and governance tokens

- Multi-chain tracking across Ethereum, Solana, Arbitrum, Base, Polygon, Avalanche, and others

- NFT tax treatment including the collectibles question (is that 28% rate applicable?), creator royalties vs. investor gains, and wash considerations

- Staking income classification with Jarrett implications and the need to determine FMV at the precise time of receipt across potentially thousands of reward events

- Cross-border compliance (FBAR, Form 8938, FATCA) for foreign exchange holdings

- Layer 2 and bridge tracking where assets cross chains and the transaction history fragments

That's not a line item you add to a general tax practice. It's a discipline.

The gap between "does some crypto" and "specializes in crypto" has never been wider. And the penalties for being on the wrong side of that gap have never been steeper.

The Real Cost of a Botched Return

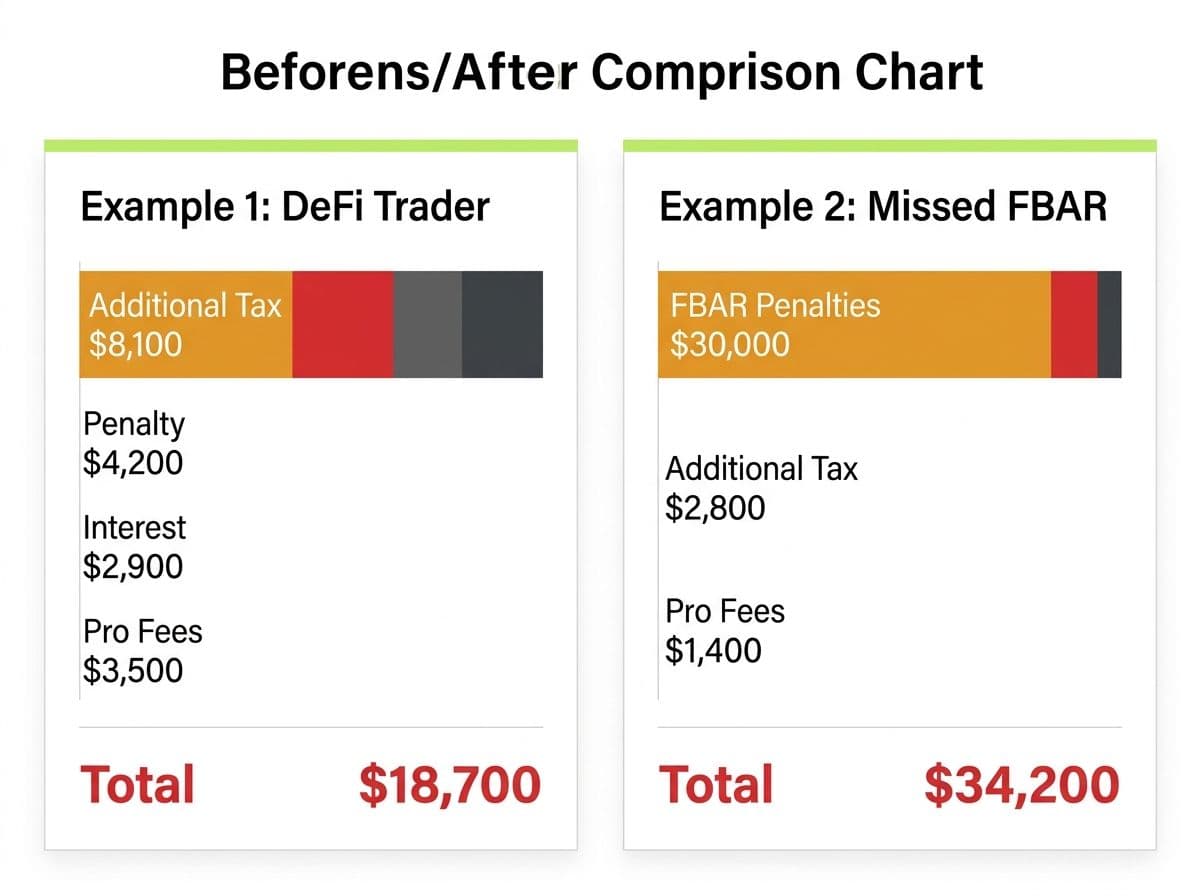

Let's put real numbers on this with two worked examples.

Example 1: The DeFi Trader Who Didn't Report LP Income

Situation: Client traded actively on Uniswap and Aave in 2024. Prior preparer only reported Coinbase trades.

$18,700

Total cost to fix: $4,200 in accuracy penalties + $8,100 in additional tax owed + $2,900 in interest + $3,500 in professional fees to amend two years of returns.

| Line Item | Amount |

|---|---|

| Additional tax owed (unreported DeFi income) | $8,100 |

| Accuracy-related penalty (20%) | $4,200 |

| Interest (2 years compounded) | $2,900 |

| Professional fees to amend 2 returns | $3,500 |

| **Total cost of the error** | **$18,700** |

Example 2: The Staker Who Missed FBAR

Situation: Client had $180,000 in staking positions on a foreign exchange. No FBAR filed for three years.

$34,200

Total exposure: $30,000 in potential FBAR penalties (non-willful, $10K per year) + $4,200 in additional tax and amendment costs.

| Line Item | Amount |

|---|---|

| FBAR penalties (non-willful, 3 years) | $30,000 |

| Additional tax on unreported staking income | $2,800 |

| Professional fees for voluntary disclosure | $1,400 |

| **Total cost of the error** | **$34,200** |

These aren't worst-case scenarios. These are typical cases we handle. The worst cases involve willful FBAR violations, criminal referrals, and six-figure penalties.

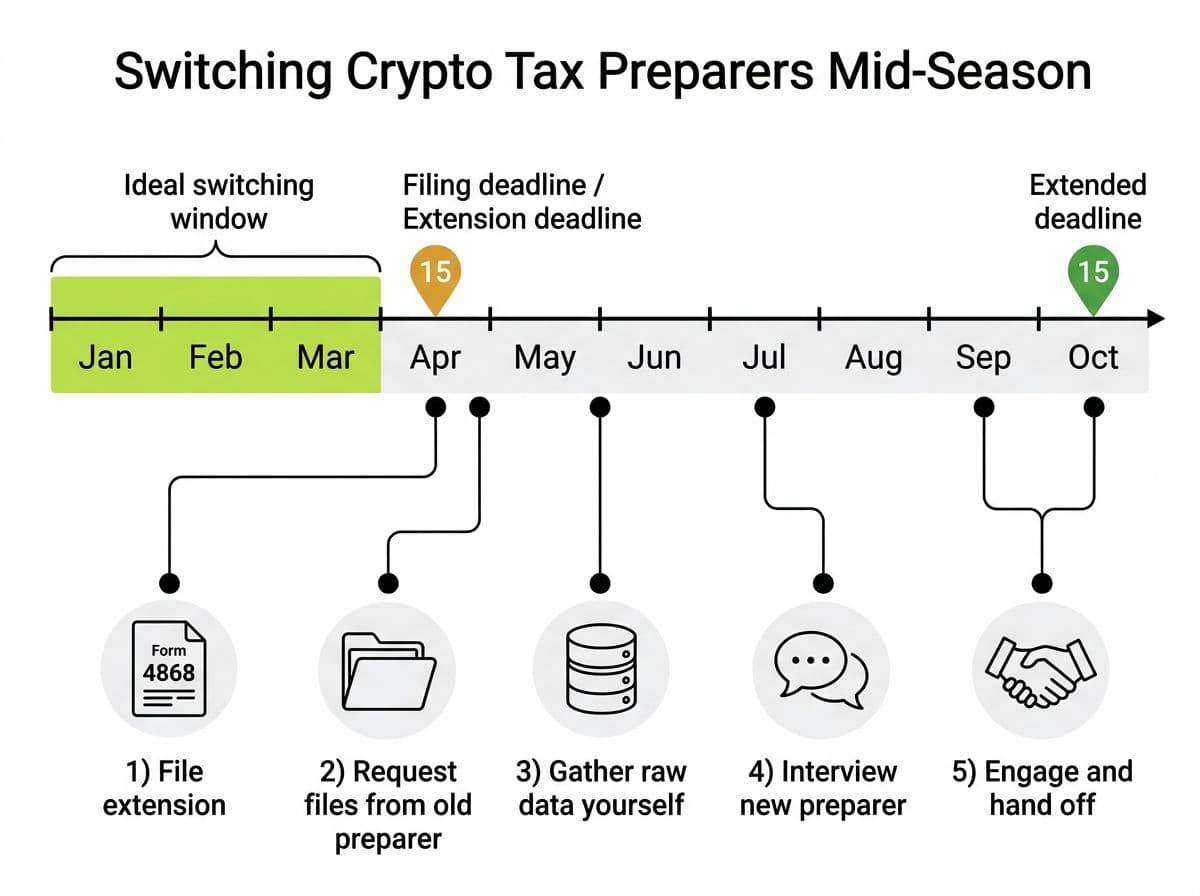

How to Switch Preparers Mid-Season Without Screwing Up Your Filing

If you've identified red flags, here's how to make the switch without missing deadlines or losing work.

Step 1: File an extension immediately.

Form 4868 gives you until October 15 to file your return. This costs nothing and there's no penalty for extending, as long as you pay estimated taxes owed by April 15. Filing an extension is the single best move you can make to give yourself breathing room.

Step 2: Request your complete file from your current preparer.

You have a legal right to your tax documents. Request:

- All prior-year returns they prepared

- Tax formsand supporting schedules

- Any crypto tax software reports they generated

- Engagement letters

- Correspondence with the IRS (if any)

Step 3: Gather your raw data separately.

Don't rely on your old preparer's data. Connect your exchanges and wallets to a crypto tax platform yourself. Download your own 1099-DAs directly from each exchange. You want your new preparer working from source data, not from potentially flawed prior work.

Step 4: Interview your new preparer using the 5-question smell test.

Run through the questions above before you engage anyone new. A qualified crypto tax CPA will welcome these questions. They've seen the damage that unqualified preparers cause.

Step 5: Give your new preparer the full picture.

Share everything: this year's data, prior-year returns, any IRS notices, and your honest assessment of where the old returns might be wrong. The more information your new preparer has upfront, the faster and cheaper the engagement.

Pro Tip

**Timing matters.** The ideal window to switch preparers is January through mid-March. After March 15, most crypto-specialized firms have limited capacity. If you're reading this in April and the deadline is approaching, file that extension first, then start your search. Rushing into a new preparer under deadline pressure is how you end up with a second bad return.

Related reading: How to choose a crypto tax CPA.

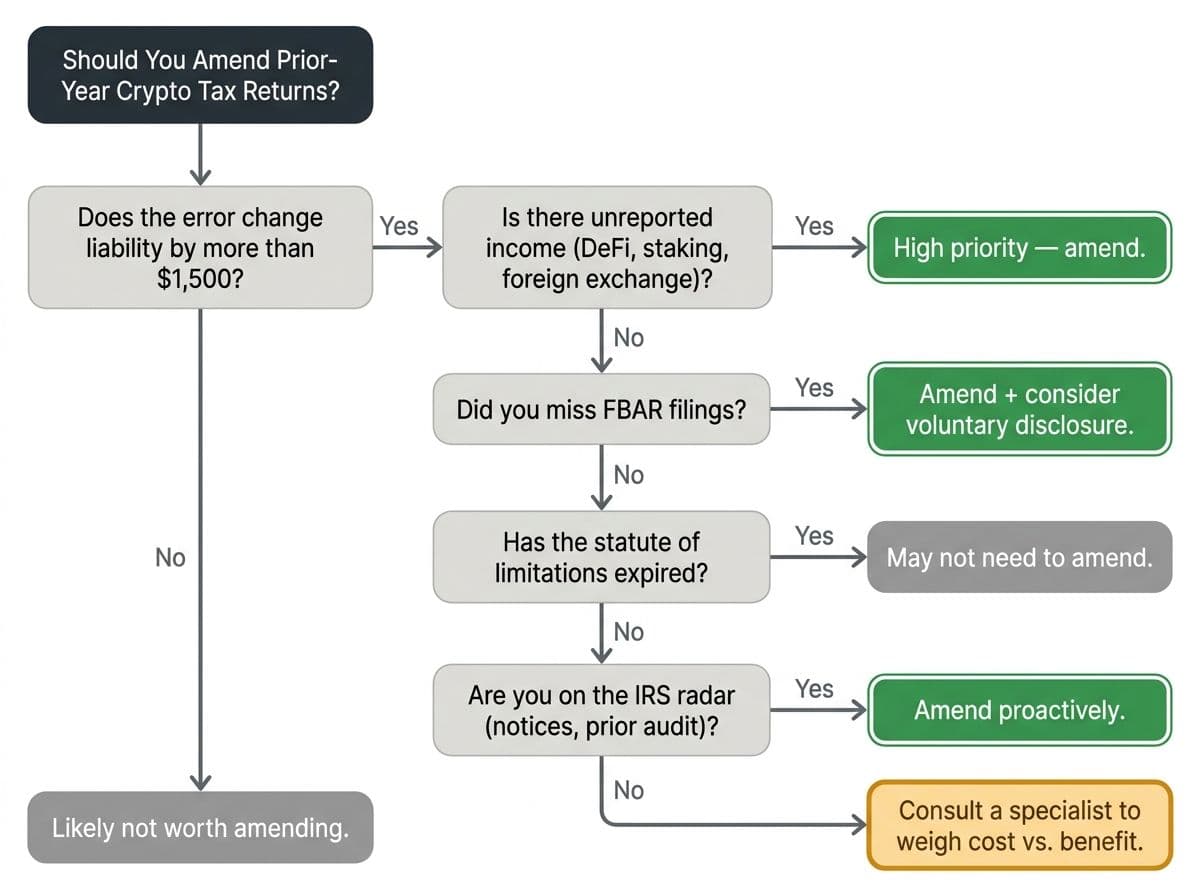

When to Amend Prior Years (and When to Let It Ride)

Not every error justifies an amendment. Here's the decision framework we use with clients.

Amend if:

- The error changes your tax liability by more than $1,500. Below that threshold, the cost of amendment often exceeds the benefit.

- You have unreported income (staking, DeFi, foreign exchange activity). The IRS can assess penalties on unreported income indefinitely in cases of substantial understatement.

- You didn't file an FBAR and were required to. FBAR penalties are severe and the voluntary disclosure programs offer significant penalty reduction if you come forward before the IRS contacts you.

- The statute of limitations hasn't expired. Generally, the IRS has three years from the filing date to audit a return. But if you omitted more than 25% of your gross income, the statute extends to six years. And if you never filed, there's no statute at all.

- You're likely to face an audit on a related issue. If you're already on the IRS's radar (received a notice, been through a prior audit), cleaning up old returns proactively is almost always the right move.

Consider letting it ride if:

- The error is less than $1,000 and you have no other compliance issues

- The statute of limitations has already expired (3 years for returns with no substantial omission)

- The error is in your favor (you overpaid), and you've already passed the 3-year claim-for-refund window

- Amending would trigger a domino effect across multiple years that isn't worth the cost

Pro Tip

Don't amend a return without understanding the full picture first. We've seen clients amend one year and accidentally draw attention to a bigger problem in another year. A qualified crypto tax CPA will review all open years before filing any amendments.

Related reading: The complete guide to crypto tax.

Action Steps: What to Do This Week

Here's your game plan:

- Run the 5-question smell test with your current preparer. Do it on your next call or send the questions via email.

- Review your most recent return for the 10 red flags above. Pay special attention to how staking rewards were classified and whether FBAR was addressed.

- If you find two or more red flags, file Form 4868 for an extension and start interviewing crypto-specialized CPAs. Use our guide to choosing a crypto tax CPA as your framework.

- Gather your raw data by connecting all your exchanges and wallets to a crypto tax platform. Don't wait for your preparer to do this.

- If prior years look wrong, book a consultation with a crypto tax specialist to assess whether amendments are warranted before filing anything.

The cost of a second opinion is negligible compared to the cost of a botched return. A 30-minute review can save you five figures.

Frequently Asked Questions

How do I know if my crypto tax preparer is qualified?

Ask them the five smell-test questions: What cost basis method did you use and why? How did you handle staking rewards? Do I need to file an FBAR? How are you reconciling against 1099-DAs? Can I see the engagement letter covering digital assets? If they can't answer these clearly, they may lack the specialized knowledge your return requires.

What's the most common mistake crypto tax preparers make?

The most common error is defaulting to FIFO cost basis without evaluating whether HIFO or Specific Identification would save the client money. The second most common is failing to report staking rewards as ordinary income.

Can I switch tax preparers in the middle of tax season?

Yes. File Form 4868 for an automatic extension to October 15, request your complete file from your current preparer, and engage a new specialist. The ideal switching window is January through mid-March.

What is Form 1099-DA and why does it matter?

Form 1099-DA is a new IRS form that crypto exchanges began issuing in 2025. It reports your digital asset transaction proceeds directly to the IRS, creating a matching document. If your return doesn't match, the IRS will flag the discrepancy.

Do I need to file an FBAR for crypto held on foreign exchanges?

If the aggregate value of all your foreign financial accounts, including crypto exchanges, exceeded $10,000 at any point during the year, you must file FinCEN Report 114 (FBAR). Penalties for non-willful failure start at $10,000 per account per year.

What is the Jarrett v. US case and how does it affect my staking taxes?

Jarrett v. United States is a case where a taxpayer argued staking rewards shouldn't be taxed until sold. While the IRS hasn't changed its guidance, the case created a good-faith basis for alternative positions. A qualified preparer should understand this case.

When should I amend a prior-year crypto tax return?

Consider amending if the error changes your liability by more than $1,500, you have unreported income, you missed FBAR filings, or the statute of limitations hasn't expired. Have a specialist review all open years before filing amendments.

What penalties can I face for crypto tax errors?

Common penalties include the accuracy-related penalty (20% of underpayment), failure-to-file penalties (5% per month up to 25%), daily compounding interest, and FBAR penalties starting at $10,000 per account per year for unreported foreign accounts.

Should I hire a CPA or an Enrolled Agent for crypto taxes?

Both CPAs and Enrolled Agents can prepare crypto returns. The key differentiator is specialization, not credential type. Look for a practitioner who focuses on cryptocurrency, has DeFi and multi-chain experience, and knows current regulations like 1099-DA and the Jarrett case.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

How to Choose a Crypto Tax CPA in 2026 (From a CPA Who Files 500+ Crypto Returns a Year)

A CPA's guide to finding the right crypto tax professional. 10 interview questions, real pricing, red flags, and when you need a CPA vs EA vs tax attorney.

Crypto Tax CPA vs Advisor vs Professional: What's the Real Difference (2026)?

CPA, EA, tax attorney, advisor, preparer — they all sound the same but mean wildly different things. A CPA breaks down what each credential means, what each can legally do for crypto investors, and which one you actually need.

How Much Does a Crypto Tax CPA Cost in 2026? (Real Numbers from a Real CPA)

Real crypto tax CPA pricing for 2026: $800 to $50K+ across four tiers. A working CPA breaks down what you'll pay, what's included, and when the ROI math makes it worth every dollar.