Crypto Options Taxes (2026): A CPA's Guide to Premiums, Exercise, Assignment, and the 60/40 Question

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

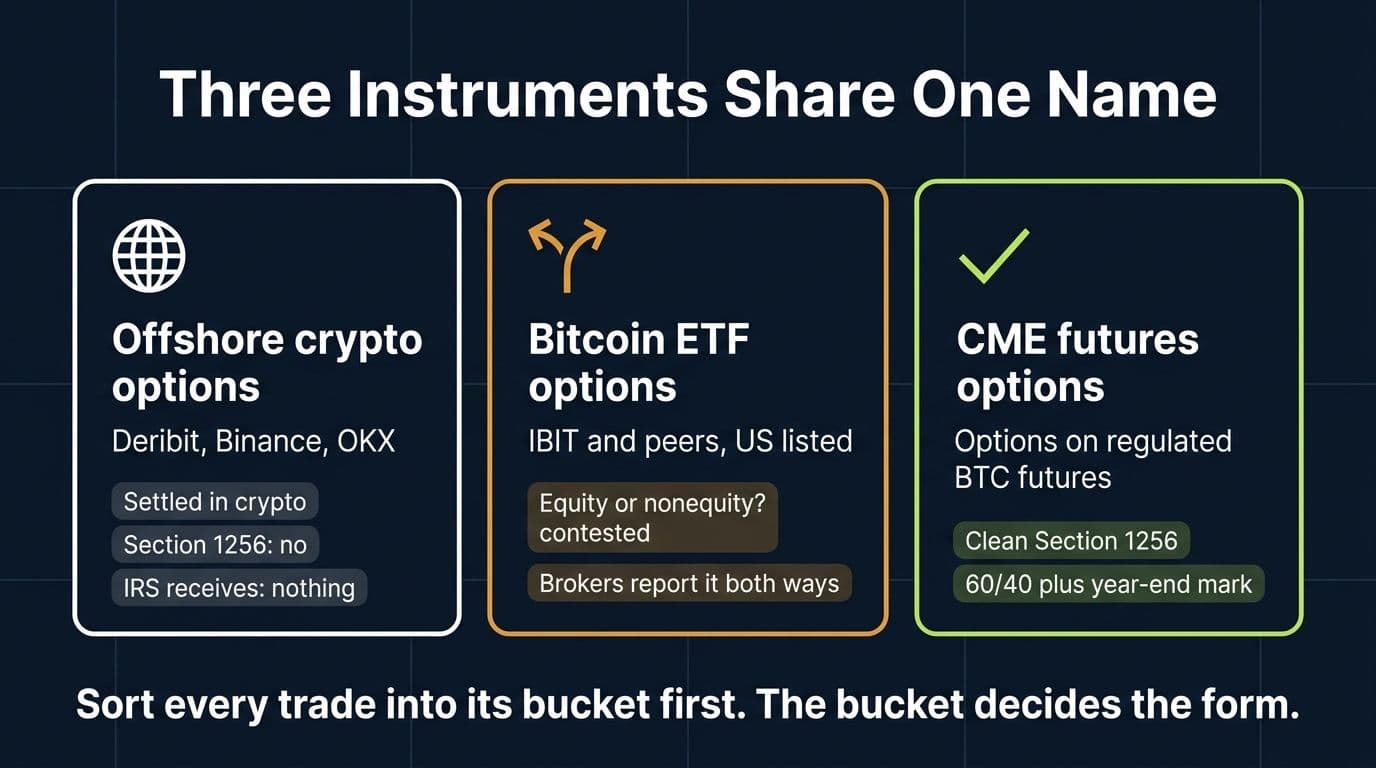

- ✓Crypto options is three different instruments in one phrase: offshore crypto-settled options (Deribit, Binance, OKX), listed options on spot bitcoin ETFs, and options on CME bitcoin futures. Each has different Section 1256 status, reporting, and traps.

- ✓The core mechanics are settled law: a buyer's premium becomes basis, a writer's premium is short-term gain at expiration or an adjustment at assignment, and writers' option gains are short-term no matter how long the contract ran.

- ✓Offshore crypto options never qualify for 60/40 treatment, and paying or receiving premiums in BTC adds a second taxable layer: the crypto you pay with is disposed of at that moment.

- ✓Options on the spot bitcoin ETFs are the honest gray zone: 1256 status turns on whether a grantor trust share is stock, and brokers report identical instruments both ways. Document whatever you file.

- ✓Deribit sends nothing to the IRS, hedging coins you hold can trigger the straddle rules, and covered calls on bitcoin ETFs sit on top of both questions at once.

Quick answer: Crypto options taxes depend on which of three very different instruments you actually traded. Options on offshore crypto exchanges like Deribit follow the general option rules (premiums become basis or short-term gain, exercise and assignment fold into the underlying, expirations are gains or losses), with no Section 1256 treatment and an extra layer of taxable events because premiums and settlements are paid in crypto. Listed options on the spot bitcoin ETFs (IBIT and its peers) trade on regulated US exchanges, and whether they are standard equity options or 60/40 Section 1256 nonequity options is a genuinely contested question that brokers themselves report inconsistently. Options on CME bitcoin futures are the one clean case: Section 1256, full stop. No offshore crypto options venue sends anything to the IRS, hedged positions can trigger the straddle rules, and the reporting burden is yours. This guide walks all four option outcomes with real numbers, the instrument-by-instrument 1256 analysis, and the traps that turn covered calls into examination issues.

Crypto options went mainstream in two directions at once. Offshore, Deribit built the deepest BTC and ETH options market in the world, and the big perp exchanges bolted on options books of their own. Onshore, the spot bitcoin ETFs got listed options in late 2024, and covered-call strategies on IBIT became a retail staple almost overnight.

Which means the same phrase, crypto options taxes, now covers instruments with almost nothing in common at tax time: a BTC-settled call on an offshore venue that reports nothing, an exchange-listed option on an ETF share held at a US broker, and a CME futures option living inside the one regime Congress actually wrote down.

Here's the deal: the option mechanics are the settled part, and everything wrapped around them is not. Premium, exercise, expiry, and assignment have clear rules that have existed for decades. What's unsettled is which rate regime applies to which instrument, what happens when the premium itself is paid in bitcoin, and how hedged positions interact with the straddle rules. We prepare returns for options traders on all three instrument types, and the expensive mistakes are almost never the mechanics; they're the wrapper.

In this guide we'll walk the four option outcomes with numbers, layer in the crypto-settlement rules for offshore venues, take the Section 1256 question instrument by instrument (including the bitcoin ETF options fight nobody warns you about), price a full options year, and cover the straddle and reporting traps at the end.

Let's get into it.

The Three Kinds of "Crypto Options" (and Why They're Taxed Differently)

Before any mechanics, sort your trades into the right bucket, because the buckets don't share rules:

Crypto Options by Instrument Type (2026)

| Instrument | Examples | Section 1256? | Settlement | What the IRS Receives |

|---|---|---|---|---|

| Offshore crypto options | Deribit BTC/ETH options, Binance and OKX options, on-chain protocols | No; venue fails the exchange test | Usually cash-settled in crypto | Nothing |

| Listed options on spot bitcoin ETFs | IBIT options and peers on US exchanges | Contested: equity option vs nonequity option | Physical delivery of ETF shares | 1099-B from your broker, but classification varies by broker |

| Options on CME bitcoin futures | CME BTC and ETH futures options | Yes, clean 1256 treatment | Into the futures contract | 1256-formatted 1099-B with the 60/40 math done |

The third row is the only comfortable one. Options on regulated futures are Section 1256 contracts: marked to market at year end, taxed on the 60/40 blend, reported by your futures broker on a 1099-B with the aggregate computed for you, and filed on Form 6781. If your crypto options exposure runs through CME futures options at a registered futures broker, your tax season is genuinely easy, and the rest of this article is context.

Everyone else, keep reading.

Option Mechanics 101: Premium, Exercise, Expiry, Assignment

These rules come from Section 1234 and decades of settled practice (IRS Publication 550 lays them out for securities options). They apply to options generally, and they're the baseline for every crypto option that isn't a Section 1256 contract.

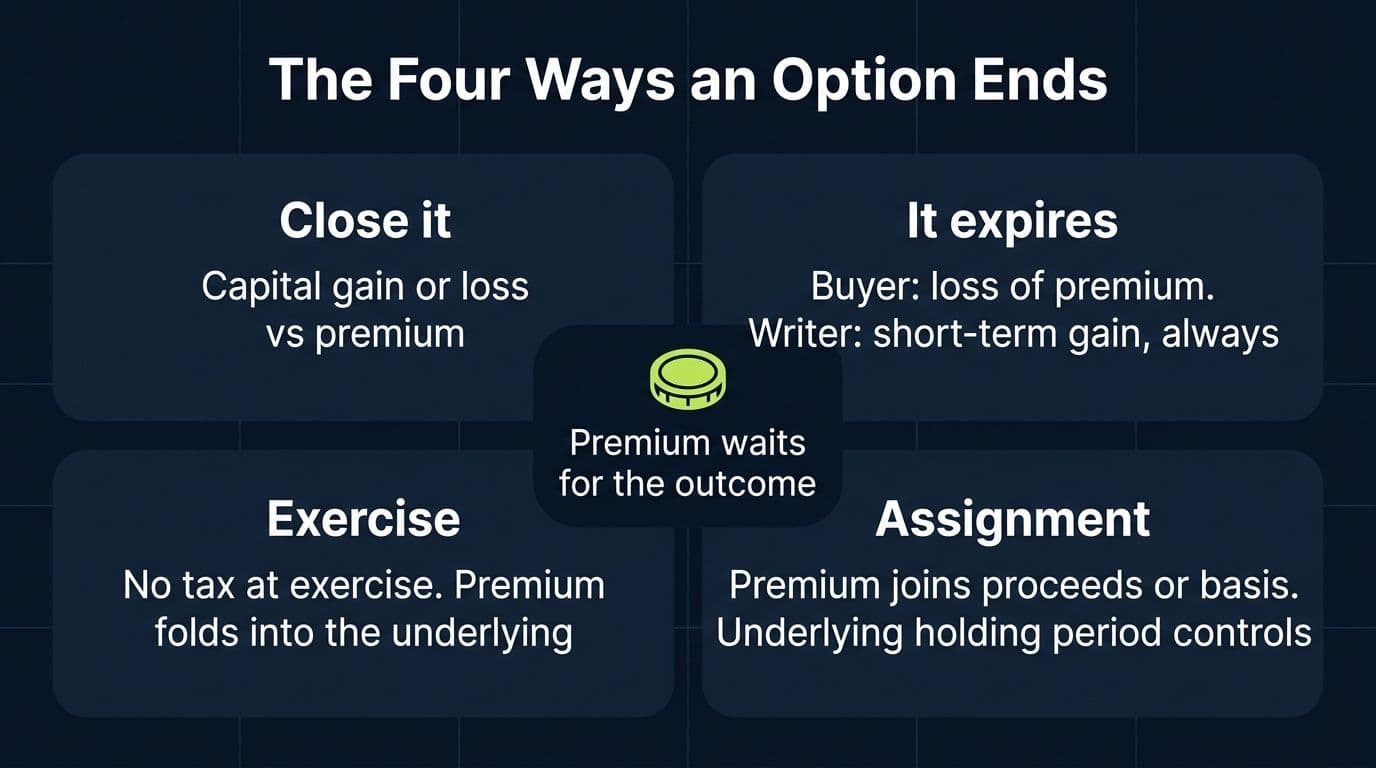

If you buy an option, the premium you pay is not a deduction. It's your basis in the option, and one of three things happens to it:

- You sell or close the option: capital gain or loss equal to proceeds minus premium, short-term or long-term by how long you held the option.

- It expires worthless: capital loss equal to the premium, realized on the expiration date.

- You exercise it: no gain or loss at exercise. For a call, the premium adds to the basis of what you acquire. For a put, the premium reduces your proceeds on the sale of the underlying. The tax event happens in the underlying, not the option.

If you write (sell) an option, the premium you receive is not income when it lands, which surprises everyone. It sits in suspense until the position resolves:

- The option expires worthless: the premium becomes gain at expiration, and it is short-term regardless of how long the option was open. That's the statutory rule for writers, not a quirk.

- You buy it back to close: short-term gain or loss equal to premium received minus what you paid to close.

- You're assigned: for a written call, the premium adds to your proceeds on the shares or coins you deliver. For a written put, the premium reduces your basis in what you're forced to buy. Again, the tax event migrates into the underlying, and the underlying's holding period controls the character.

Those rules are the good news: they're knowable. Now the crypto layers.

The Crypto-Settled Layer: When the Premium Itself Is Bitcoin

On Deribit and most offshore venues, options are priced, margined, and settled in crypto. A BTC call costs 0.02 BTC, not $1,900. That one design choice doubles your taxable events, because crypto is property, and every time you pay with it, you dispose of it.

Concretely:

Paying a premium in BTC is two things at once: a disposal of the BTC (capital gain or loss against your basis in those coins, at that moment's value) and the purchase of an option with a basis equal to that value. Traders who paid premiums out of a long-held BTC stack all year have a string of small BTC disposals they never noticed making.

Receiving a premium in BTC gives you coins whose dollar value at receipt measures the premium, and those coins start their own basis and holding period immediately. When the option later expires or closes, your writer gain is measured off that receipt value under the conservative approach. The precise timing interplay (value measured at receipt, gain recognized at resolution) has no crypto-specific guidance, which is a sentence you should be used to by now; document your method and apply it consistently.

Cash settlement in crypto creates a new lot. Deribit-style options settle in the underlying coin: an in-the-money BTC call pays you the intrinsic value in BTC. That settlement is your option proceeds (measured in dollars at settlement) and simultaneously a new BTC lot with that basis. Sell it later and the movement from settlement day is a separate gain or loss.

None of this changes the option rules above. It bolts a property-disposal transaction onto each side of them. If you also trade perps on these venues, the same layering logic applies to funding and collateral, which we covered in our crypto perpetual futures guide, this article's sibling.

2x the events

A crypto-settled option generates roughly twice the taxable events of a dollar-settled one: every premium paid is also a crypto disposal, and every settlement received is also a new crypto lot with its own basis clock.

Does Section 1256 Apply? Instrument by Instrument

Section 1256 taxes qualifying contracts at a blended 60% long-term, 40% short-term rate with year-end mark-to-market, and for option traders the relevant doorway is the nonequity option: a listed option, traded on a qualified board or exchange, that is not an equity option. We walked the full statute in our Section 1256 guide; here's how it lands for each options instrument.

Offshore Crypto Options: No, at the Threshold

A listed option only reaches Section 1256 if the venue is a qualified board or exchange: a CFTC-designated contract market, a registered national securities exchange, or a Treasury-designated foreign exchange. Deribit is none of these. Neither is Binance, OKX, or any on-chain options protocol. The analysis ends at the venue, before the contract-type question is reached. Claiming 60/40 on Deribit options is an error, not a position. Character defaults to the general option rules above, almost always short-term capital.

Worth repeating for 2026: Deribit's acquisition by a US-listed company and the CFTC staff's new tolerance for US access to certain Deribit products change market structure, not tax character. No crypto venue has a Treasury designation, and access relief is not an exchange designation.

CME Bitcoin Futures Options: Yes, Cleanly

Options on regulated futures contracts, traded on a CFTC-designated market like CME, are Section 1256 contracts. 60/40, mark-to-market, Form 6781, broker-computed reporting. This is the instrument the statute was built for, and for high-bracket traders who want crypto options exposure with settled tax treatment, it's the venue where the law already works.

Bitcoin ETF Options: The Honest Gray Zone

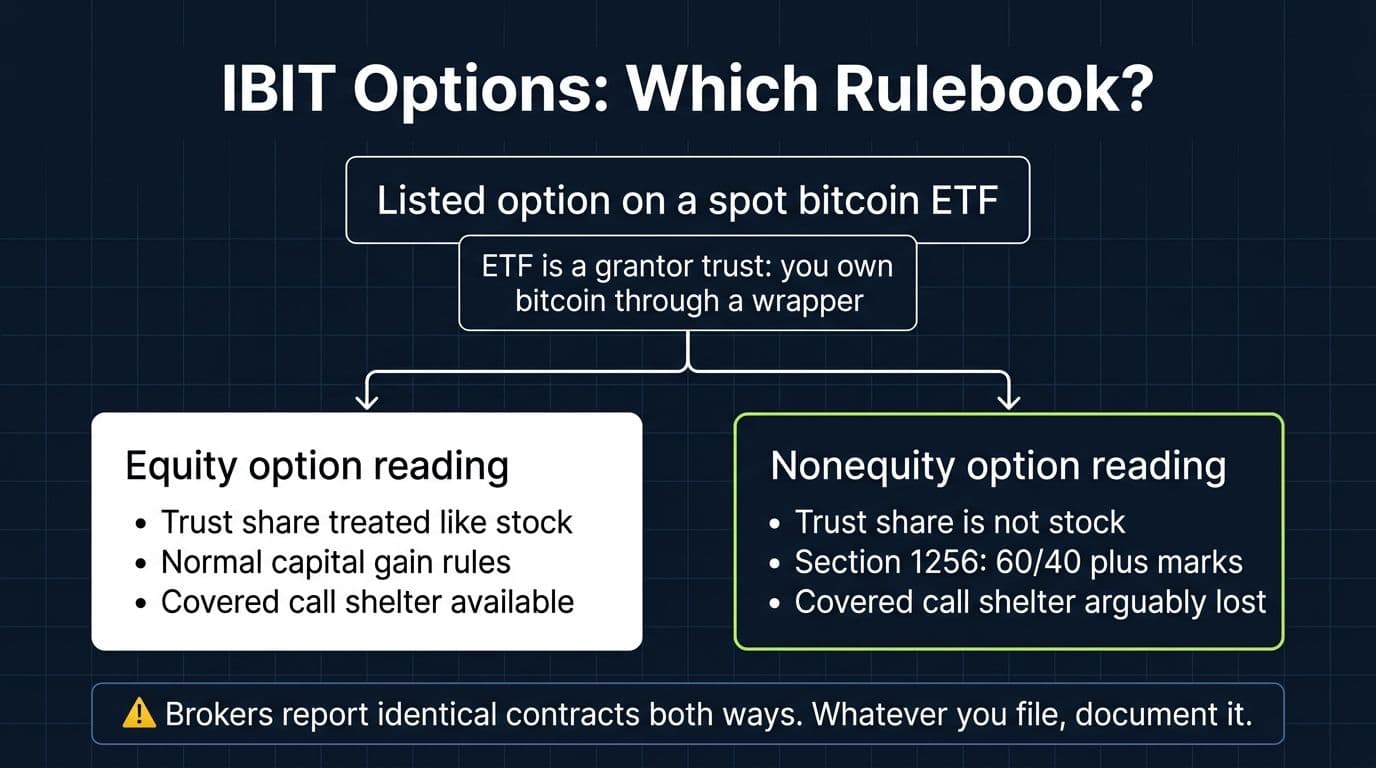

Now the fight. Options on IBIT and the other spot bitcoin ETFs trade on registered US securities exchanges, so the qualified-exchange prong is satisfied automatically. Everything turns on the second question: is an option on a spot bitcoin ETF an equity option or a nonequity option?

The statute defines an equity option as an option on stock or on a narrow-based stock index. Here's why that's not a clean answer for IBIT: the spot bitcoin ETFs are structured as grantor trusts, not corporations. For tax purposes, a grantor trust share is treated as direct ownership of a pro rata slice of the trust's bitcoin; you own bitcoin through a wrapper, not stock in a company that owns bitcoin. If a grantor trust share is not "stock," then a listed option on it is not an equity option, which would make it a nonequity option, which would make it a Section 1256 contract with 60/40 treatment and year-end marks.

That argument is not fringe. It's the same analysis practitioners have applied for years to listed options on the gold and silver grantor trusts, and brokers themselves are split on it: some report bitcoin ETF options as Section 1256 contracts in the 1256 section of the 1099-B, while others report them as ordinary equity options. Two traders with identical trades at different brokers can receive contradictory tax documents for the same instrument, and both brokers will insist their classification is right.

Our posture, consistent with every unsettled question in this series: this is a documentable position in either direction, and the worst answer is not noticing the question. If your broker reports 1256 and you file 1256, keep the broker's classification with your records. If you take a position against your broker's paper (in either direction), you need a written analysis, consistency across years, and a conversation about disclosure. What you cannot defensibly do is pick whichever character produced less tax each year and hope the 1099-B agrees.

“The bitcoin ETF options returns worry me more than the Deribit ones. Deribit traders know they're offshore and expect homework. ETF options traders assume the 1099-B settled everything, and half of them have never checked whether their broker called the same instrument a 1256 contract that another broker called an equity option.”

, Leanne Grant, EA

Covered Calls on Bitcoin ETFs: Where Every Question Meets

The most popular crypto options strategy of 2026 is also the one sitting on top of every unsettled issue at once. A covered call on IBIT (own the shares, write calls against them) touches the mechanics, the classification fight, and the straddle rules simultaneously.

The mechanics are the easy part, and we price them in the worked example below: the premium waits in suspense, expiration makes it short-term gain, assignment folds it into your share proceeds, and the shares' holding period controls that character.

The wrapper is the hard part, in two ways:

First, the classification tension cuts both directions. If IBIT options are equity options, covered-call writers get the benefit of the qualified covered call exception: a body of rules (in Section 1092 and its regulations) that protects at-or-out-of-the-money covered calls on stock from straddle treatment. If IBIT options are nonequity options taxed under 1256, the option leg gets 60/40 and year-end marks, but the qualified covered call shelter, written for equity options on stock, arguably isn't available, and the position may need straddle analysis instead. You don't get to claim 60/40 rates and the stock-based straddle exception at the same time; the two positions contradict each other. Almost nobody trading these strategies has noticed.

Second, deep in-the-money calls suspend holding periods either way. Write a call that's too deep in the money against shares you haven't held twelve months, and the holding period clock stops or restarts. Traders running aggressive covered-call ladders on ETF shares they bought recently can discover that gains they assumed were going long-term never got there.

If you're writing covered calls at real size on bitcoin ETFs, this specific intersection is worth a professional review before year end, while positions can still be managed, rather than at filing time when the answers are locked.

Straddle Rules: The Trap Around Hedged Crypto

The straddle rules deserve their own section because they reach beyond ETF options, into any hedged crypto structure.

Section 1092 applies to offsetting positions in actively traded personal property, and bitcoin is about as actively traded as personal property gets. Hold BTC and buy a BTC put (on any venue, in any wrapper), and you likely have a straddle. Run long spot against short calls, or long ETF shares against offshore options, and mixed cross-venue versions of the same question appear.

When the straddle rules apply, three things happen, all bad for the unprepared:

- Losses defer. Realize a loss on one leg while the other leg has unrecognized gain, and the loss is disallowed this year to the extent of that gain. It carries forward instead of deducting now.

- Holding periods terminate. A put purchased against BTC you've held eight months doesn't pause the clock; it kills it. The holding period restarts when the hedge comes off, and gains you assumed were nearly long-term go back to zero.

- Carrying costs capitalize. Interest and carrying charges allocable to the straddle stop being deductible and get added to basis instead.

We flag this as complexity rather than walking every computation, because straddle mechanics with crypto legs (identified straddles, mixed straddles with a 1256 leg, the interaction with the wash-sale rule's absence) are genuinely intricate and fact-specific. The practical takeaway fits in one sentence: if you hedge crypto you also hold, your losses and holding periods are not what your trading app thinks they are, and that's a CPA conversation before you file, ideally before you hedge.

What Deribit Reports (Nothing) and What That Means

The largest crypto options market on earth sends the IRS exactly nothing. Deribit issues no 1099 of any kind: no 1099-DA, no 1099-B, no year-end tax document. That did not change when Coinbase acquired the platform in 2025, and no reporting has been announced since. The venue has required identity verification since late 2020, so your account is not anonymous; it's simply unreported, which is a very different thing.

The consequences run exactly parallel to what we detailed for Hyperliquid and the offshore perp world:

Everything is taxable anyway. Premiums earned, options settled, coins disposed to pay premiums, and settlement lots sold later, all reportable by you, per the IRS digital asset rules, with a "Yes" on the digital asset question.

Visibility arrives at the off-ramp. Move profits to a US exchange and cash out, and that exchange's 1099-DA reports proceeds, usually with no basis, and your options year becomes the unexplained gap behind a number the IRS can see.

The offshore account questions apply. A Deribit account is an account at a foreign institution. Under current guidance, crypto-only foreign accounts have not been FBAR-reportable, but the rules have been slated to change for years, accounts touching fiat are a different analysis, and Form 8938 is broader still. Material offshore options balances belong in front of your preparer with the balance history, proactively.

And exports decay. Pull your full trade, settlement, and transfer history now, not in April. Offshore venues change export formats, delist products, and truncate histories without any obligation to preserve your paperwork.

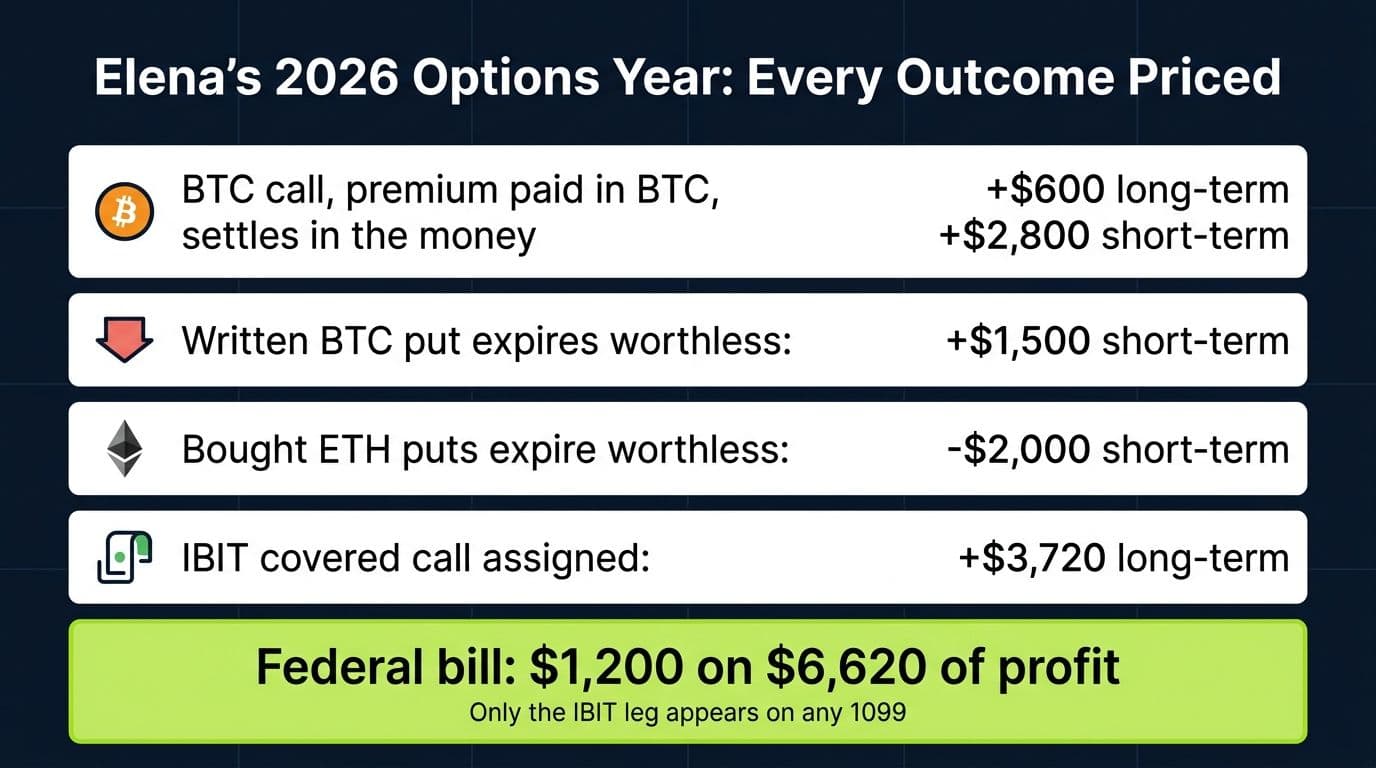

A Worked Example: Elena's Options Year

Meet Elena: 24% federal bracket, 15% long-term capital gains rate, trading options on Deribit and covered calls on IBIT at a US broker during 2026. Four positions, four different outcomes, every mechanic priced.

Elena's 2026 Options Year

| Position | What Happened | Tax Result |

|---|---|---|

| Bought 1 BTC call (Deribit), premium 0.02 BTC | Paid with BTC bought in 2023: basis $1,300, worth $1,900 at payment. Call settles in the money at expiry; she receives BTC worth $4,700 | Two events: $600 long-term gain on the BTC used to pay (15% = $90), then $2,800 short-term gain on the option ($4,700 minus $1,900 basis; 24% = $672). New BTC lot: basis $4,700 |

| Wrote 1 BTC put (Deribit), premium 0.015 BTC worth $1,500 at receipt | BTC stays above the strike; the put expires worthless | $1,500 short-term gain recognized at expiration (24% = $360), regardless of how long the option ran. The premium BTC starts with $1,500 basis |

| Bought 2 ETH puts (Deribit), $2,000 in USDC | ETH rallies; the puts expire worthless | $2,000 short-term capital loss at expiration (saves $480 against her other short-term gains) |

| Covered call on IBIT: 300 shares, basis $18,000 ($60), held 14 months; wrote 3 calls at the $70 strike for $720 total premium | Shares assigned at $70 | Premium folds into proceeds: $21,000 plus $720 minus $18,000 = $3,720 long-term gain (15% = $558), because the shares' 14-month holding period controls |

The totals: long-term gains of $4,320 ($600 + $3,720) taxed at 15% is $648; net short-term of $2,300 ($2,800 + $1,500 minus $2,000) taxed at 24% is $552. Federal bill: $1,200 on $6,620 of net profit, an 18% blended rate, with every dollar self-reported except the IBIT leg.

Now the classification kicker on that IBIT covered call. Elena's broker reported it as an equity option, so the premium folded into her long-term share sale. Had her broker (or her own documented position) treated the calls as Section 1256 contracts, the option leg would be severed and taxed separately at 60/40: $720 splits into $432 at 15% and $288 at 24%, about $134, while the shares' $3,000 gain stays long-term at $450, totaling $584 against $558 under equity treatment. On these facts, the boring equity-option answer is $26 cheaper, because assignment folded the premium into a long-term gain that beats the 60/40 blend. Flip the facts (shares held short-term, or calls expiring instead of assigned) and 1256 wins instead. The classification fight has no universal winner, which is exactly why it needs to be a documented decision rather than an accident of which broker you use.

And the January reality: the IRS receives a 1099-B for the IBIT leg and nothing for the other three positions. Elena's return reports $6,620 of profit against paper showing $3,720. That gap is normal, legal, and entirely hers to substantiate.

Options Year Spread Across Deribit and a US Broker?

We reconstruct crypto options histories end to end: premiums, exercises, assignments, and crypto-settled lots priced correctly, the ETF options classification documented, straddle exposure reviewed, and every venue reconciled. Flat-fee, done by a crypto CPA.

Book a callWash Sales: One Rule, Two Answers

Crypto options produce a split answer on wash sales, and it mirrors the instrument map.

Bitcoin ETF shares and their listed options are securities. The wash-sale rule fully applies: sell IBIT at a loss and repurchase within 30 days (or write deep puts that effectively repurchase it), and the loss defers into the replacement position's basis. Options count both as triggers and as replacement property.

Crypto-native options and the coins themselves are property, not securities, so the wash-sale rule does not currently apply: a Deribit loss followed by an immediate re-entry generally remains deductible. Congress keeps proposing to close this, so verify the rule's status for your filing year, and remember that economic-substance doctrines still police loss patterns that exist only on paper. The full analysis, including the ETF-versus-coin boundary, is in our crypto wash sale guide.

Traders running both books at once, harvesting ETF losses while trading offshore options on the same underlying, are stacking a securities rule, a property rule, and the straddle rules on one position. That's not a software workflow; that's an engagement.

How to Report Your Crypto Options, Step by Step

- Sort every position into its instrument bucket first: offshore crypto options, listed ETF options, CME futures options. The bucket decides the form.

- Export complete histories now: trades, settlements, premium flows, and transfers from every venue, plus your broker's 1099-B classification for ETF options.

- Price the crypto legs of every offshore trade: the disposal when you paid premiums in coin, the receipt value of premiums collected, and the new lots created by settlements, per wallet under the current basis rules.

- Apply the option outcomes: closed options to Form 8949 as capital gains and losses, expired long options as losses, expired written options as short-term gains, and exercised or assigned options folded into the underlying's basis or proceeds.

- Handle the 1256 instruments on Form 6781: CME futures options always; ETF options only per your broker's classification or your own documented position, marks included.

- Check straddle exposure before finalizing losses: any period where you held crypto and an offsetting option needs Section 1092 review before those losses deduct.

- Reconcile the paper: your 1099-Bs and any off-ramp 1099-DA must tie to the return, answer the digital asset question "Yes," and pay estimates in profitable years, because nobody withheld anything.

Pro Tip

Before you file, pull last year's 1099-B and check which section your broker put your bitcoin ETF options in. If you trade the same instrument at two brokers, check both. Contradictory classifications for identical contracts are common, and finding the discrepancy yourself beats having a matching program find it for you.

When to DIY and When to Bring In a Pro

Straight talk:

Handling crypto options taxes yourself is workable if: your activity is a handful of listed ETF options at one US broker, your 1099-B is consistent and you follow its classification, you wrote nothing against appreciated shares you've held under a year, and you have no offshore or crypto-settled positions.

Get professional help if: you traded crypto-settled options on Deribit or any offshore venue, you're writing covered calls at size on bitcoin ETFs, your brokers classify the same instrument differently, you hedged coins you hold (straddle territory), you want the 1256 position documented in either direction, offshore balances raise FBAR questions, or a notice already arrived. Here's what a crypto-specialized CPA costs so you can price the decision honestly.

Options give you defined risk on the trade and undefined risk on the return. Define both: documented classifications, complete histories, and consistent positions turn the gray zones from threats into footnotes.

Get Your Crypto Options Filed Right

Flat-fee preparation for options and derivatives traders: every premium, exercise, expiry, and assignment priced correctly, classifications documented, straddles reviewed, and offshore activity reconciled before the IRS asks. Signed by a CPA who does this all season.

Book a callFAQ: Crypto Options Taxes

Frequently Asked Questions

How are crypto options taxed in the US?

Under the general option rules unless the instrument qualifies for Section 1256. A buyer's premium becomes basis, then produces capital gain or loss when the option is sold, expires, or folds into the underlying at exercise. A writer's premium becomes short-term gain at expiration or adjusts the underlying at assignment. Offshore crypto-settled options add a second layer: the crypto used to pay or settle is itself disposed of.

Do crypto options get Section 1256 60/40 treatment?

It depends on the instrument. Options on CME bitcoin futures: yes, cleanly. Options on offshore venues like Deribit: no, the venues are not qualified exchanges. Listed options on spot bitcoin ETFs like IBIT: genuinely contested, because the answer turns on whether a grantor trust share is stock, and brokers report it both ways.

Is the premium I receive for writing an option taxable when I receive it?

No. Premium received sits in suspense until the position resolves. If the option expires worthless, the premium is short-term capital gain at expiration regardless of how long the option ran. If you're assigned, it folds into the proceeds or basis of the underlying. If you buy to close, the difference is short-term gain or loss.

What happens tax-wise when my option expires worthless?

For a buyer, a capital loss equal to the premium paid, realized on the expiration date, short-term or long-term by how long you held the option. For a writer, short-term capital gain equal to the premium received, always short-term by statute.

How is exercising a crypto option taxed?

Exercise itself is not the taxable moment for standard options. A call buyer adds the premium to the basis of what's acquired; a put buyer subtracts it from sale proceeds. Cash-settled crypto options work differently in practice: settlement pays out intrinsic value, which closes the option (gain or loss against premium basis) and, if paid in crypto, creates a new lot at that value.

How does assignment on a covered call work at tax time?

The premium you received is added to your proceeds on the shares you deliver, and the shares' holding period controls the character. Shares held over a year produce long-term gain including the premium; shares held under a year make the whole result short-term. Deep in-the-money calls can suspend or reset holding periods, so strike selection has tax consequences.

Are IBIT options equity options or Section 1256 contracts?

Unresolved. The spot bitcoin ETFs are grantor trusts, and if a trust share is not stock, listed options on it would be nonequity options qualifying for Section 1256. Some brokers report them as 1256 contracts and others as equity options, for identical instruments. Whichever treatment you file, keep the broker's classification and document your position.

Does Deribit report to the IRS?

No. Deribit issues no tax forms of any kind and files nothing with the IRS, a posture unchanged by its acquisition by Coinbase in 2025. The platform has required identity verification since late 2020, so the activity is documented, just unreported. Your profits are fully taxable and self-reported, and off-ramping through a US exchange creates the paper trail.

Do I owe tax if my premiums and settlements never left Deribit?

Yes. Tax attaches when options close, expire, or settle, and when crypto is disposed to pay premiums, not when money reaches a bank. Keeping everything on the platform changes your visibility, not your liability.

What are the straddle rules and do they apply to my hedged BTC?

Section 1092 targets offsetting positions in actively traded personal property, and holding BTC while buying BTC puts likely qualifies. Losses on one leg defer to the extent of unrecognized gain on the other, holding periods can terminate and restart, and carrying costs capitalize. Hedged crypto positions need professional review before losses are claimed.

Does the wash sale rule apply to crypto options?

Split answer. Bitcoin ETF shares and their listed options are securities, so the wash-sale rule fully applies. Crypto-native coins and offshore crypto options are property under current law, so it does not, though proposals to change that keep circulating. Trading both books on the same underlying stacks the two regimes and deserves professional attention.

What forms do I use to report crypto options?

Form 8949 and Schedule D for standard option outcomes and the crypto legs of offshore trades; Form 6781 for Section 1256 instruments (CME futures options, and ETF options if that classification applies). Answer the Form 1040 digital asset question Yes if you touched crypto-settled instruments.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Crypto Perpetual Futures Taxes (2026): A CPA's Guide to Perps on Every Platform, Funding, and Liquidations

Perps now trade on three regulatory tiers with three tax stories. A CPA maps Section 1256 per tier, funding both directions, liquidations, collateral traps, and a full worked year.

Section 1256 and Event Contracts (2026): Do Kalshi and Prediction Markets Get 60/40 Treatment?

Section 1256's 60/40 rate could cut a prediction market trader's federal bill by a quarter, but no platform reports event contracts that way. A CPA walks the statutory test, the math, and the Form 6781 and Form 8275 mechanics.

Hyperliquid Taxes (2026): A CPA's Guide to Perps, Funding Payments, and the Airdrop the IRS Never Saw

Hyperliquid issues no tax forms and the IRS has no perp guidance. A CPA covers perps, hourly funding, the HYPE airdrop, and a full worked year with real numbers.

The Ultimate Guide to Crypto Tax (2026 Edition)

The most comprehensive crypto tax guide online, written by a CPA who files 500+ crypto returns a year. Every taxable event, form, strategy, and 2026 update.