Crypto Perpetual Futures Taxes (2026): A CPA's Guide to Perps on Every Platform, Funding, and Liquidations

By Garrett Taylor, CPA #133092

Reviewed by Leanne Grant, EA #00167954-EA

Key Takeaways

- ✓Where you trade decides your tax options. Offshore exchanges and DeFi perps fail Section 1256 at the threshold; the new onshore perps approved in May and June 2026 clear it, but 60/40 remains an unproven position and CME's lawsuit against the CFTC puts the core question in federal court.

- ✓With Section 1256 unavailable or unproven, perp gains fall into a capital-versus-ordinary fight with no IRS ruling. The common conservative default is short-term capital treatment on Form 8949, documented and applied consistently.

- ✓Funding payments cut both ways with no direct guidance: funding received is ordinary income under the conservative view, while funding paid is often a disallowed expense for investors.

- ✓A liquidation is a disposition, not a nothing: the margin you lose is a realized loss. And converting appreciated crypto into USDC collateral is a taxable disposal before the first trade opens.

- ✓Most perp venues report nothing to the IRS. Your first paper trail is usually the off-ramp exchange's 1099-DA showing proceeds with no basis, and your return has to explain it.

Quick answer: Crypto perpetual futures profits are fully taxable, and the rules depend on where you trade. Perps on offshore exchanges like Binance and Bybit, and on DeFi protocols like dYdX, GMX, and Hyperliquid, do not qualify for the 60/40 Section 1256 rate because those venues are not CFTC-registered; the real question there is capital versus ordinary treatment, and the IRS has never answered it. The new CFTC-approved onshore perps (Kalshi's BTCPERP, approved May 2026, plus the Bitnomial and Coinbase products that followed) have a genuinely stronger Section 1256 argument, but it is unproven and the core legal question is in federal court right now. Funding payments have no direct guidance, liquidations are taxable disposals, and converting appreciated crypto into stablecoin collateral is itself a taxable sale. Most perp venues send you no tax forms at all, which means the reporting burden is yours. This guide covers every tier, both directions of funding, a full worked year with real numbers, and the traps we fix most often.

Perpetual futures are how most crypto leverage actually trades. They dwarf spot volume on the big exchanges, they never expire, and until last year they lived entirely offshore, on venues that treat US tax forms as someone else's problem.

Then 2026 happened. The CFTC approved the first US-listed perpetual futures contract in May, more onshore perps followed within weeks, CME sued the CFTC over all of it in June, and suddenly the same instrument can exist on three different regulatory tiers with three different tax stories.

Here's the deal: crypto perpetual futures taxes are unsettled at almost every layer, and the venue you trade on determines which unsettled questions apply to you. We prepare returns for perp traders across every tier, and the pattern is always the same: no tax forms, no direct IRS guidance, thousands of taxable events, and a trader who assumed none of it counted because nothing hit a bank account.

In this guide we'll map the three platform tiers, walk the Section 1256 analysis for each one, handle funding payments in both directions, price a liquidation and the collateral events around a real trading year, and show you exactly what the IRS sees versus what you owe.

Let's dig in.

What a Perpetual Future Is (and Why the IRS Has Never Addressed One)

A perpetual future, a perp, is a leveraged derivative that tracks the price of an underlying asset with no expiration date. You post collateral (usually USDC or USDT), choose leverage, and go long or short. Because the contract never expires, there's no delivery date pulling its price toward spot. Instead, exchanges use funding payments: periodic transfers between longs and shorts, calculated from the gap between the perp price and the spot index, that keep the contract tethered to the real market.

That structure is the whole tax problem. A perp is not a traditional futures contract (no expiry, no delivery), not an option (no premium, no strike; crypto options have their own rulebook, which we cover separately), and not exactly a swap (it's exchange-listed and standardized, not a bilateral OTC contract), but it borrows features from all three. Congress never contemplated perps when it wrote the derivatives rules, and the IRS has issued no ruling, notice, or regulation on how they are characterized. Every position a US taxpayer takes on perp taxation is a position built from analogy.

The economics are still simple to tax in one respect: when you close a perp position, gain or loss is realized. The fights are about character (capital or ordinary), rate (does the 60/40 blend ever apply), and the treatment of the cash flows around the position: funding, margin, collateral, and liquidations. So let's take those in order, starting with the question that decides everything else: where do you trade?

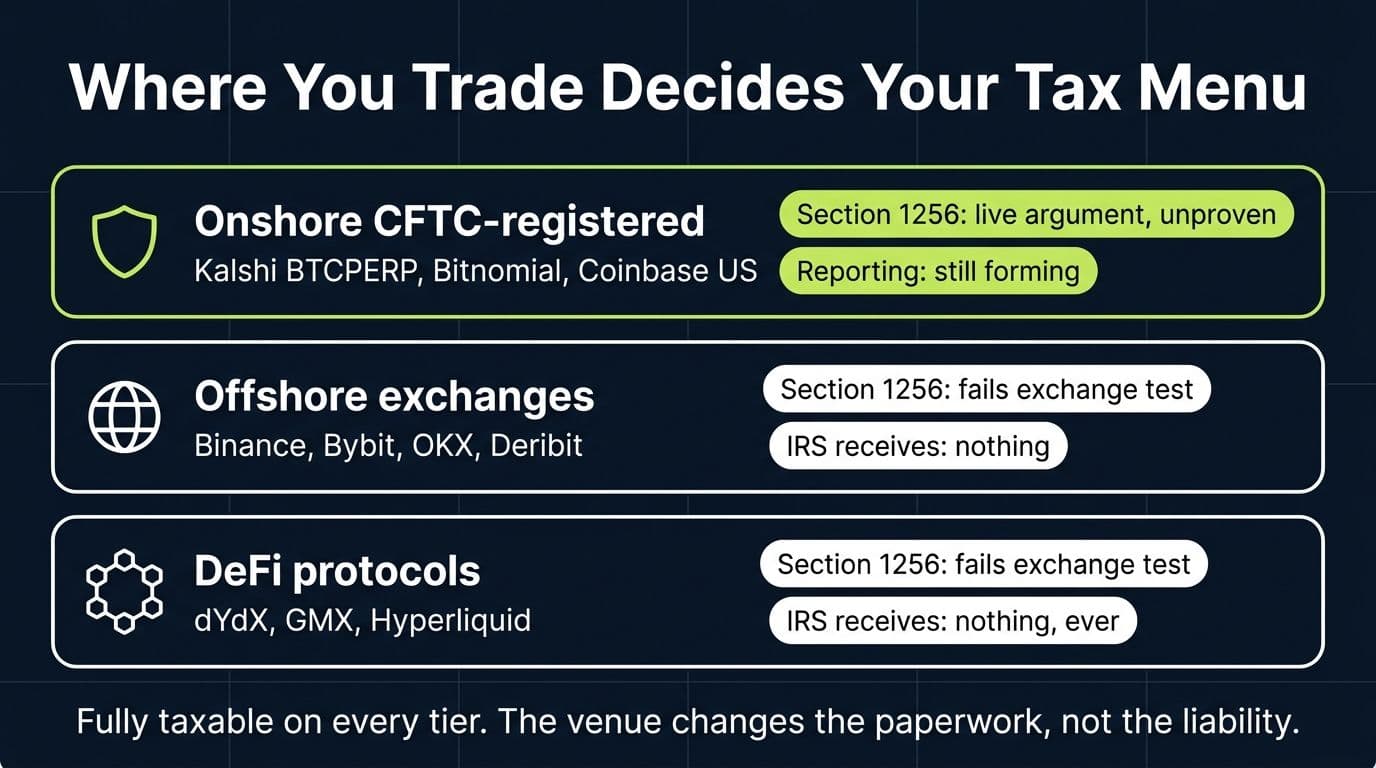

The Three Platform Tiers (and Why Your Venue Decides Your Tax Menu)

In 2026, crypto perps trade on three distinct regulatory tiers. The tax analysis is different on each one, and traders who use more than one tier (most active traders do) need to keep the records separated.

Crypto Perp Platforms by Regulatory Tier (2026)

| Tier | Examples | Regulatory Status | Section 1256 Argument | What Gets Reported |

|---|---|---|---|---|

| Onshore CFTC-registered | Kalshi BTCPERP, Bitnomial (Kraken) perps, Coinbase's US perp-style futures | Listed on CFTC-designated contract markets | Live but unproven; litigation pending | Reporting posture still forming; do not assume a 1256 1099-B |

| Offshore centralized exchanges | Binance, Bybit, OKX, Deribit | Not CFTC-registered; most exclude US persons by ToS | None; fails the exchange test | Nothing filed with the IRS |

| DeFi protocols | dYdX, GMX, Hyperliquid | No registration, no custodian, often no KYC | None; fails the exchange test | Nothing, and after the 2025 DeFi broker rule repeal, nothing is coming |

Tier one is brand new. On May 29, 2026, the CFTC approved Kalshi's BTCPERP contract, a cash-settled bitcoin perpetual listed as a futures contract on a designated contract market, the first US-listed perp ever. The same day it issued a policy statement on listing perpetual contracts generally. Bitnomial, the CFTC-regulated exchange Kraken acquired, launched onshore perps on BTC, ETH, SOL, and XRP in mid-June, and Coinbase announced its own US perp-style futures product for late July.

Tier two got a wrinkle this year. The CFTC's staff also confirmed that certain Deribit perpetuals can be treated as foreign futures for US customers accessing them through Coinbase's registered futures brokerage. That's meaningful market access news. It is not a tax upgrade, and we'll come back to why, because it's one of the most misunderstood points of the year.

Tier three is the DeFi world, where the protocol holds no customer file and files nothing, ever. Congress repealed the rule that would have forced DeFi front-ends to report like brokers when the President signed H.J.Res.25 in April 2025, and under the Congressional Review Act the IRS cannot reissue a substantially similar rule. We covered the deepest version of this tier in our Hyperliquid taxes guide, and everything there about invisible-but-taxable activity applies to dYdX, GMX, and the rest of the on-chain perp world.

One thing is identical across all three tiers: the profits are fully taxable to US taxpayers. Offshore terms of service, VPNs, and wallet pseudonymity change your paperwork trail, not your tax bill. US taxpayers owe US tax on worldwide income, and the IRS digital asset rules put the reporting obligation on you whether or not any form exists. If the property-and-disposal baseline underneath all of this is new to you, start with our complete crypto tax guide and come back; everything below assumes it.

Does Section 1256 Apply? The Per-Tier Analysis

Section 1256 is the prize everyone asks about: qualifying contracts are marked to market at year end and taxed on a 60/40 split, 60% long-term and 40% short-term regardless of holding period, which caps the top blended federal rate near 28% instead of 37%. We walked the full statute, both qualification doors, and the swap exclusion in our Section 1256 and event contracts guide. Here's how the analysis lands for perps, tier by tier.

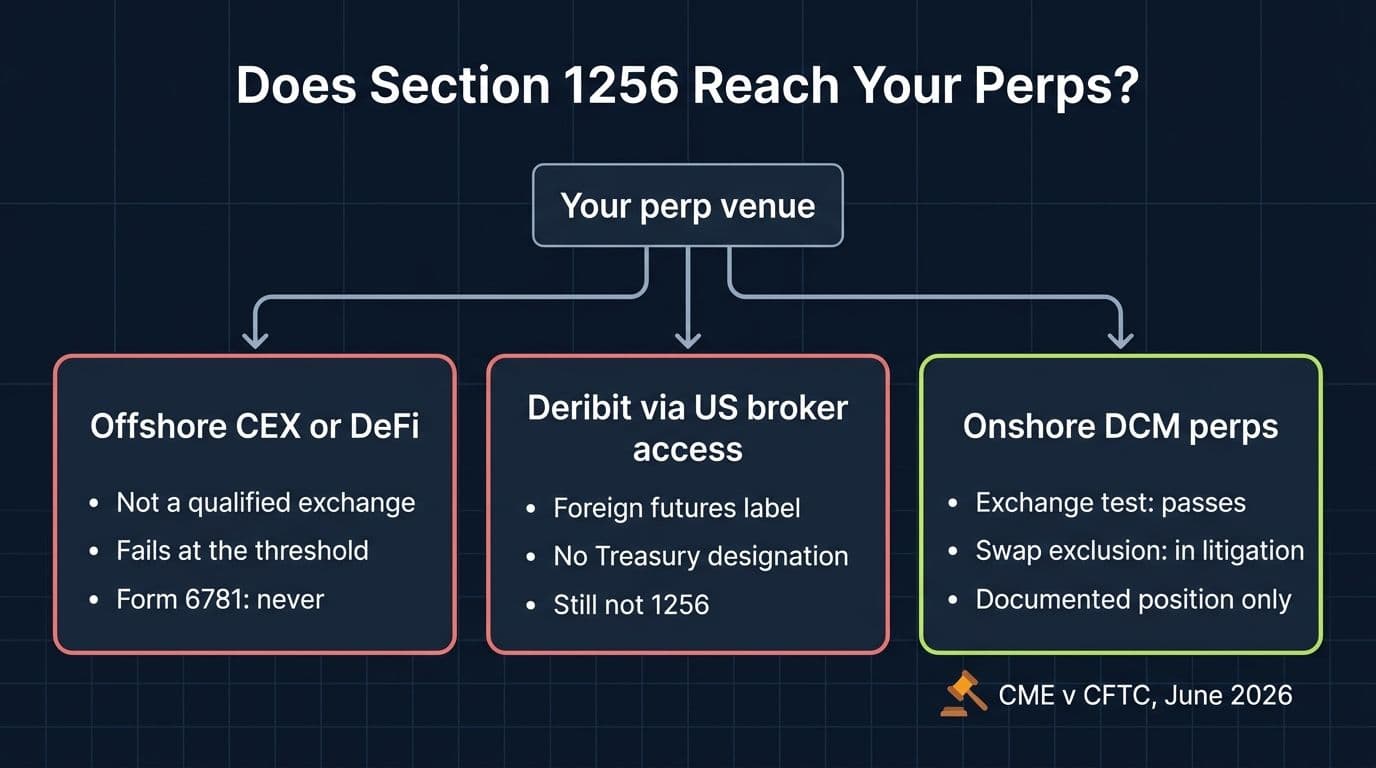

Offshore Exchanges and DeFi: Fails at the Threshold

Section 1256 requires the contract to trade on a qualified board or exchange: a CFTC-designated contract market, a registered national securities exchange, or a foreign exchange the Treasury has specifically designated. Binance is not one. Bybit is not one. Neither is dYdX, GMX, or Hyperliquid, none of which is registered with the CFTC in any capacity.

That's the whole analysis for tiers two and three. The contract-type questions never get reached, because the exchange test fails first. Reporting offshore or DeFi perps on Form 6781 as 60/40 is not an aggressive position; it's an error, and it's one we see on self-prepared returns every season.

The Deribit Foreign Futures Trap

Here's the 2026 misunderstanding worth its own subsection. When CFTC staff confirmed that certain Deribit perps can be treated as foreign futures for US customers routed through a registered broker, a wave of commentary concluded those trades now get futures tax treatment. They don't.

Foreign futures only reach Section 1256 if the foreign exchange has its own Treasury designation as a qualified board or exchange, a short list built over decades of specific rulings. Deribit has no such designation. A CFTC staff letter about market access does not create one, and Treasury has designated no crypto venue. So a Deribit perp traded through the new onshore access route is regulated market access to a non-1256 contract. The character analysis below applies to it exactly as if you'd traded it offshore.

Onshore Perps: A Real Argument, in Real Litigation

The new tier-one products are different. Kalshi's BTCPERP and Bitnomial's perps are listed on CFTC-designated contract markets, so the qualified exchange prong is satisfied cleanly. And unlike the fully collateralized event contracts we analyzed in the 1256 guide, perps are leveraged, margined instruments where cash moves with the mark. The regulated futures contract definition requires that deposits and withdrawals depend on a system of marking to market, and a margined perp with periodic funding and variation-style settlement fits that description far more comfortably than a binary contract ever did. The CFTC even approved BTCPERP explicitly as a futures contract.

So is it 60/40? Not so fast, for two reasons.

First, the swap exclusion. Section 1256(b)(2)(B) excludes swaps and "similar agreements" from Section 1256 entirely, and the argument that a perp is economically a swap (no expiry, periodic payments between two sides) is serious. It is so serious that CME Group sued the CFTC in June 2026 arguing exactly that: perpetual contracts meet the Dodd-Frank definition of swaps and cannot be listed as futures. The CFTC calls the suit meritless, and the tax statute doesn't automatically follow the regulatory label either way. But nobody should claim confidence about the tax character of an instrument whose legal classification is in active federal litigation.

Second, the paper trail. The reporting posture for these brand-new products is still forming. Traditional futures brokers report Section 1256 contracts in a dedicated section of the 1099-B with the aggregate profit or loss computed for you. Whether the new perp venues and their brokers will report that way for 2026 is not yet established, and a Form 6781 filed with numbers no broker corroborates is a position, not a default.

Our posture for onshore perp traders, and the same one we take for event contracts: treat 60/40 as a documented position, not a checkbox. That means a written analysis prepared before filing, consistent application across all qualifying positions including the year-end mark, and a serious conversation about a Form 8275 disclosure. For a high-bracket trader with six figures of onshore perp profit, the rate difference is worth real money and the apparatus is cheap. For a small account, it usually isn't.

Everyone Else: The Capital-Versus-Ordinary Fight

With Section 1256 unavailable (tiers two and three) or unproven (tier one), perp P&L falls into the same two-framework fight we detailed for Hyperliquid, and the frameworks travel with the instrument, not the venue.

The capital framework, the common conservative default, treats each closed position as a disposition producing capital gain or loss, short-term in practice, reported on Form 8949 and Schedule D. Section 1234A supports it: gain or loss from terminating a right or obligation with respect to property that would be a capital asset is capital gain or loss.

The swap framework characterizes the perp as a notional principal contract, with ordinary gains and losses and funding netted annually. It has economic logic and one practical advantage on funding (below), but it has to explain away the exchange-listed, standardized structure of the instrument, and ordinary characterization invites scrutiny exactly when it saves the most: in loss years.

Whichever framework you use, the discipline is the same. Pick it deliberately, write down why, apply it to every position on every venue, and don't switch years without advice. Consistency is the difference between a defensible unsettled position and an examination story.

3 tiers, 0 rulings

Crypto perps now trade on three regulatory tiers in the US market, and the IRS has issued direct tax guidance for none of them. Every filing position is built from analogy, which makes documentation the whole game.

Funding Payments: Both Directions, No Guidance

Funding is the defining cash flow of a perp, and it flows both ways: when the perp trades above spot, longs pay shorts; below spot, shorts pay longs. An active account accrues hundreds or thousands of small funding events a year, and the IRS has never said a word about them.

Three treatments show up in practice, and we walked them in depth in the Hyperliquid guide: ordinary income at receipt (the conservative default), netting funding into the position's P&L (operationally clean, arguably aggressive), and swap-style annual netting (only coherent inside the swap framework).

What deserves emphasis here is the asymmetry that hits investors. Under the conservative treatment, funding you receive is ordinary income in full. Funding you pay is an investment expense, and for individuals who are investors rather than trade-or-business traders, miscellaneous investment expenses are currently disallowed. Pay $2,000 of funding and receive $1,500 across the year, and the conservative reading picks up $1,500 of income with no deduction for the $2,000. You lost $500 economically and owe tax on $1,500. That's not a drafting exaggeration; it's how the disallowance mechanically works, and it's the strongest practical argument traders raise for the netting approaches. If funding is a material number for you, characterization is worth a professional conversation before you file, not after.

One more flag for the basis-trade crowd: delta-neutral funding capture (long spot, short perp) is a straddle in substance, with loss-deferral and recharacterization rules layered on top of everything above. That structure needs a professional, full stop.

Liquidations Are Disposals (Not Nothing, and Not Theft)

Leverage means liquidations, and liquidations confuse people at tax time more than any other perp event.

When your margin falls below maintenance and the engine force-closes your position, that closure is a disposition of the position, exactly as if you had closed it yourself at that price. The margin you lost is a realized loss: under the capital framework, a capital loss (almost always short-term) equal to what you put into the position and didn't get back, including the liquidation fee.

Two mistakes to avoid, one in each direction:

Mistake one: treating a liquidation as a non-event. Traders who track only voluntary closes systematically overstate their income, because the year's blowups never make it into the loss column. Your liquidation losses are real, deductible losses under the capital framework (against gains plus $3,000 of ordinary income per year, with carryforward). Losing them in bad recordkeeping means paying tax on profits you didn't keep.

Mistake two: deducting a liquidation as theft or casualty. A liquidation is not a hack, not a scam, and not a casualty. It's the contract working as designed. It produces a trading loss with trading-loss character, not a theft loss, and returns that dress liquidations up as something else draw exactly the attention you'd expect.

Partial liquidations follow the same logic at smaller scale: each force-closed slice is a disposition of that slice, with its share of basis.

Margin and Collateral: The Taxable Events Around the Trade

Perp taxation isn't just the positions. The collateral lifecycle generates its own events, and they're the ones traders miss most reliably.

Funding your margin account can be taxable before you ever trade. Moving USDC you already own onto a venue is not a taxable event; it's your own property changing location (though under Rev. Proc. 2024-28, its basis now lives wallet by wallet). But converting BTC or ETH into USDC to post as collateral is a disposal of the BTC or ETH, with gain or loss measured against your basis, at the moment of the swap. Traders who funded a margin account by rotating appreciated coins into stablecoins have realized a gain that exists whether or not the subsequent trading goes well. It's the single most expensive surprise we find in perp returns.

Stablecoin disposals themselves are technically reportable. Every USDC you spend on fees or settle losses with is a disposal of property. The gain or loss rounds to zero because the basis is a dollar, but the reporting obligation exists, and a year of perp activity can generate hundreds of these line items. This is a recordkeeping burden, not usually a tax bill, and it's one more reason perp histories need software or a professional rather than a spreadsheet built in April.

Profits paid in USDC start new basis clocks. Realized P&L credited to your account in USDC is a new lot of property with a dollar basis. It matters later, when that USDC moves, converts, or off-ramps.

Posting appreciated crypto directly as collateral (some venues take BTC or ETH margin) is murkier: posting alone shouldn't be a disposal while you keep ownership, but if the venue's mechanics settle your losses by taking the coin, each taking is a disposal of that coin at that moment's value. Cross-margin accounts on offshore venues can quietly generate dozens of these.

“Perp traders always want to talk about the character of their trading profits, and that's the right conversation. But the returns I end up amending usually went wrong before the first trade: an appreciated BTC stack rotated into USDC collateral, a five-figure gain realized on day one, and nobody noticed because it didn't feel like selling.”

, Leanne Grant, EA

Trader or Investor: The Status Question Under Everything

Almost every unsettled question above lands differently depending on whether you're an investor or a trader in the tax sense, so it's worth naming the line.

Most perp traders are investors for tax purposes, even very active ones. Investors get capital treatment, the $3,000 annual limit on net capital losses, and no deduction for investment expenses, including, under the conservative reading, funding paid.

Trader tax status requires activity that is substantial, continuous, and conducted like a business: near-daily trading, significant volume, and profit-seeking from short-term swings rather than long-term appreciation. Traders deduct business expenses (data, software, a home office) on Schedule C even though their trading gains stay capital by default.

The deeper layer is a Section 475(f) mark-to-market election, which converts trading gains and losses to ordinary and eliminates the capital-loss limit. Whether and how 475 reaches crypto derivative positions is its own unsettled analysis (the election's scope for commodities and the definitional questions around digital assets are genuinely intricate), and the election has to be made in advance, not retrofitted onto a bad year. If you traded at professional scale or took a large loss, this is a sit-down conversation with a CPA before year end, not a checkbox in filing software.

And a reminder that surprises people in profitable years: nothing was withheld. A good perp year means quarterly estimated payments, and the penalty for skipping them is a real interest charge, not a rounding error.

Wash Sales: Still Not Applicable, Still Not a Free Lunch

Under current law, the wash-sale rule applies to securities, and crypto held as property sits outside it. Cash-settled perp positions are even further from the rule's text. So realized perp losses are generally deductible even if you reopen the same position minutes later, and loss harvesting around perps remains mechanically available. Our crypto wash sale guide covers the rule, the pending proposals to extend it to digital assets, and the economic-substance doctrines that still apply to circular loss-generation patterns. Short version: the rule doesn't apply today, confirm that's still true for the year you file, and don't run harvesting patterns that have no substance beyond the deduction.

What Actually Gets Reported: 1099-DA, 1099-B, or Nothing

Here's the paper-trail map, tier by tier, for the 2026 filing season:

Who Sends What to the IRS (2026)

| Venue Type | Form You Get | Form the IRS Gets | Your Exposure |

|---|---|---|---|

| Onshore CFTC perps (Kalshi, Bitnomial, Coinbase US) | Posture still forming; may be futures-style statements | Same open question | Don't assume a 1256-formatted 1099-B; keep your own records |

| Offshore CEX (Binance, Bybit, OKX, Deribit) | Nothing | Nothing | Full self-reporting; account data can still surface via analytics and legal process |

| DeFi (dYdX, GMX, Hyperliquid) | Nothing | Nothing, permanently, after the DeFi broker rule repeal | Full self-reporting; the chain records everything forever |

| US spot exchange where you fund or cash out | 1099-DA | 1099-DA | Proceeds reported, often with no basis; the mismatch is on you to explain |

The last row is where invisible years become visible. The moment you convert BTC to USDC on a US exchange to fund a perp account, or off-ramp profits back through one, that exchange files a 1099-DA reporting the proceeds. For anything you acquired before 2026 or transferred in from an external wallet, the basis box will be blank, which makes the sale look like pure profit until your return explains otherwise. We covered exactly what to do with those forms, and the mismatch notices they generate, in our 1099-DA guide.

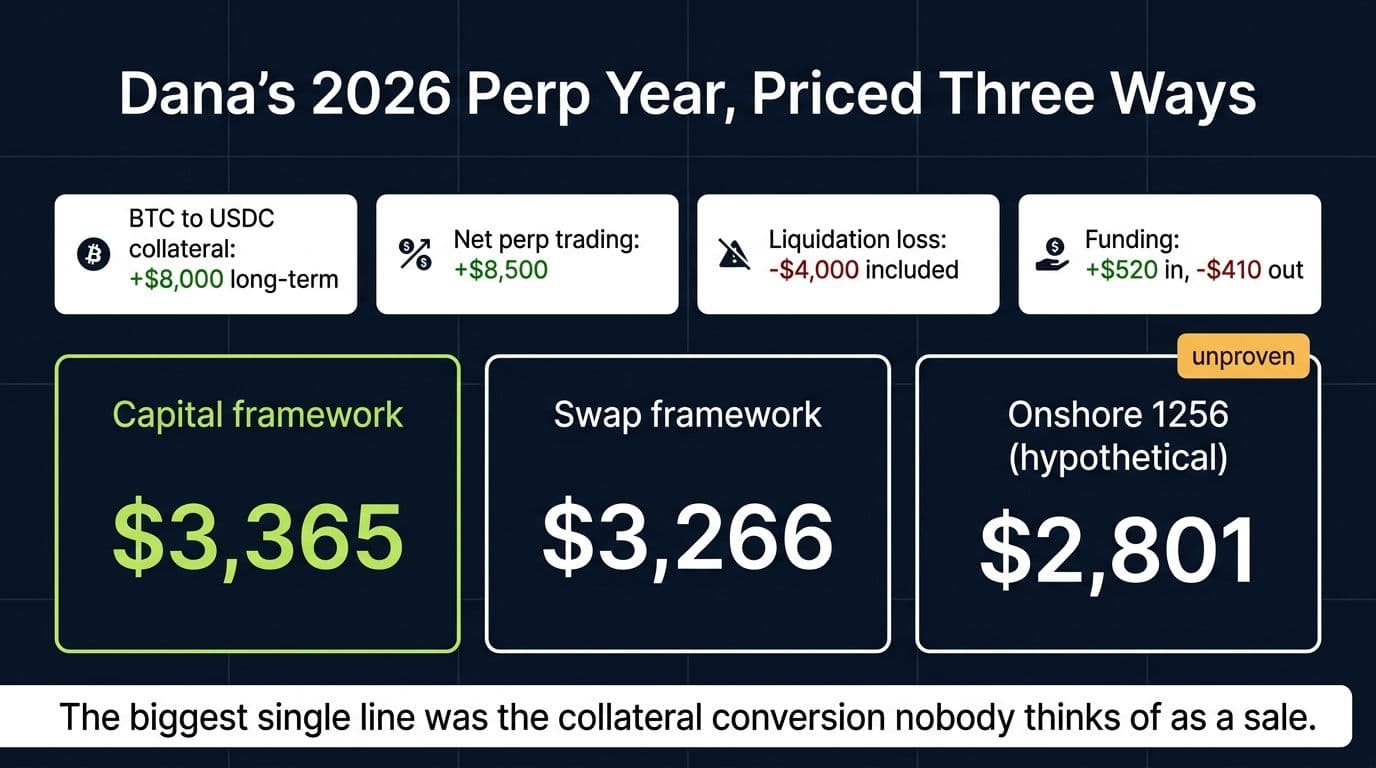

A Worked Example: Dana's Perp Year

Numbers make all of this concrete. Meet Dana: 24% federal bracket, 15% long-term capital gains rate, an investor (no trader status), trading perps on a DeFi venue during 2026.

Dana's 2026 Perp Year

| Event | Detail | Tax Consequence |

|---|---|---|

| Funds the account in February | Converts 0.5 BTC (basis $22,000, held since 2023) into 30,000 USDC on a US exchange, bridges it out | $8,000 long-term capital gain, realized on day one; the exchange files a 1099-DA |

| 58 closed perp positions | Gains $22,000, losses $9,500 on voluntary closes | Net +$12,500; character per framework |

| One liquidation in June | 5x ETH long force-closed; $4,000 of posted margin wiped, fee included | $4,000 realized loss, same character as other position losses |

| Funding, all year | Received $520, paid $410 | Method-dependent (see table below) |

| Fees settled in USDC | Hundreds of small USDC disposals at dollar basis | Roughly $0 gain, reportable, a recordkeeping item |

Dana's net perp P&L is $12,500 minus $4,000, so +$8,500, plus the $8,000 collateral gain she realized before the first trade. Here's her federal bill under the two live frameworks, plus a third column showing what the identical year would have looked like on an onshore venue if the Section 1256 position were taken and sustained:

Dana's Federal Tax, Three Ways (2026)

| Item | Capital Framework (conservative) | Swap / Ordinary Framework | Onshore 1256 (hypothetical, unproven) |

|---|---|---|---|

| Net perp P&L (+$8,500) | Short-term capital, 24% = $2,040 | Ordinary, netted with funding: $8,610 at 24% = $2,066 | $8,610 at 60/40 = $1,601 |

| Funding received ($520) | Ordinary, 24% = $125 | Netted above | Folded into contract P&L |

| Funding paid ($410) | No deduction (investor) | Netted above | Folded into contract P&L |

| BTC to USDC collateral conversion (+$8,000 LT) | 15% = $1,200 | 15% = $1,200 | 15% = $1,200 |

| **Total federal** | **$3,365** | **$3,266** | **$2,801** |

Three things to notice. First, the largest single tax item is the collateral conversion, $1,200 on a gain Dana realized before opening a single position. Second, the capital and swap frameworks land within $99 of each other in a profitable year, because short-term capital and ordinary rates match; the difference is the $410 of funding paid that the swap framework rescues from disallowance. Third, the 1256 column saves about $560 on these numbers, and at ten times the profit in the top bracket the same structure saves five figures, which is exactly why the onshore question matters and exactly why it should be taken as a documented position or not at all.

The asymmetry shows up in the bad year. Flip Dana's result to a $20,000 net perp loss: the capital framework deducts $3,000 a year against ordinary income and carries the rest forward, the ordinary framework could absorb far more if the characterization holds, and a sustained 1256 position would allow a three-year carryback against prior 1256 gains. Traders who pick a framework for one year's math and want a different framework's loss rules the next year are building the file an examiner dreams about. Pick once, document, stay consistent.

And the IRS's view of this same year in January 2027? One document: a 1099-DA showing $30,000 of BTC proceeds, basis blank, from the February funding conversion. Dana's actual taxable income is about $17,000 across three character categories. Her return either explains that cleanly, or the automated matching system asks her to.

Trading Perps Across Venues With No Paper Trail?

We reconstruct full perp histories across offshore, DeFi, and onshore venues: positions characterized and documented, funding handled, liquidations captured, collateral events priced, and every off-ramp dollar reconciled. Flat-fee, done by a crypto CPA.

Book a callFBAR, Form 8938, and the Offshore Account Question

Perp traders touch offshore infrastructure constantly, so the foreign-account rules deserve a straight summary.

Self-custodied wallets (your keys, DeFi venues): not an account with a foreign financial institution, and under current FinCEN guidance not FBAR-reportable, though FinCEN has signaled for years that it intends to bring crypto into the FBAR regime. Same posture we detailed for Hyperliquid.

Accounts at offshore centralized exchanges (Binance, Bybit, Deribit): a genuinely different analysis. You have an account, at an institution, that is foreign. Under current guidance, an account holding only crypto has not been FBAR-reportable, but an account that ever holds fiat currency can be, and the aggregate $10,000 threshold counts across all foreign accounts. Form 8938 has its own thresholds and its own broader definition of specified foreign financial assets, and the conservative posture for material offshore balances is disclosure. The penalties for getting FBAR wrong are disproportionate to the effort of filing it, so if you carried real money on an offshore venue at any point in the year, put this question in front of your preparer with your balance history, not after the fact.

How to Report Your Perp Year, Step by Step

- Export everything from every venue, now. Trade history, funding history, liquidation records, transfer logs, from the interface and API while access is easy. Offshore and DeFi venues owe you nothing in April.

- Price the collateral lifecycle first. Identify every conversion into and out of stablecoins, every deposit of appreciated crypto, and every disposal the margin mechanics forced. Establish basis per wallet and per account under Rev. Proc. 2024-28.

- Compute realized P&L per closed position, liquidations included. Gains and losses separately, liquidation fees in the loss column, and reconcile against funding so nothing double-counts.

- Pick your framework and write it down. Capital treatment on Form 8949 and Schedule D is the common conservative default for offshore and DeFi perps. Onshore 1256 treatment, if you take it, needs a written analysis, consistent application including year-end marks, and a Form 8275 conversation. Never 6781 for offshore or DeFi venues.

- Report funding under your documented method. Conservative: net funding received as ordinary income on Schedule 1, no deduction for funding paid if you're an investor.

- Reconcile every 1099-DA. Whatever a US exchange reported has to tie to your return, with basis documented from your own records, because the form's basis box is blank or wrong for anything that predates 2026 or arrived from an external wallet.

- Answer the digital asset question "Yes" and pay estimates. Nothing was withheld. A profitable year means quarterly payments in the year you earn it.

Pro Tip

Reconcile quarterly, not annually. A perp account generates thousands of micro-events across positions, funding ticks, and stablecoin disposals, and every venue's export gets harder to pull as time passes. The traders who hand us clean quarterly exports pay for hours; the ones who hand us a wallet address in April pay for a reconstruction.

When to DIY and When to Bring In a Pro

Straight talk:

Handling crypto perpetual futures taxes yourself is workable if: you traded modest size on one venue, your software ingests the full history including funding and liquidations, you're comfortable with short-term capital treatment and ordinary funding income, and your off-ramp 1099-DAs reconcile to your records.

Get professional help if: you traded across tiers (onshore plus offshore plus DeFi), you're weighing the onshore Section 1256 position, you funded margin with appreciated crypto, you got liquidated at size, you're considering trader status or a 475 election, funding is a material number in either direction, you carried balances on offshore exchanges (FBAR territory), or a mismatch notice already arrived. Here's what a crypto-specialized CPA costs and how to think about the buy-versus-build decision on your own time.

The perp market moved onshore faster than the tax law did. Until the IRS speaks, the trader with documented methods, complete records, and consistent positions holds every good card, on every tier.

Get Your Perp Year Filed Right

Flat-fee preparation for derivatives traders: every venue reconstructed, framework documented, funding and liquidations handled, onshore 1256 analysis done properly or ruled out honestly, and a return that survives the mismatch machine.

Book a callFAQ: Crypto Perpetual Futures Taxes

Frequently Asked Questions

How are crypto perpetual futures taxed in the US?

Profits are fully taxable, but the character is unsettled. The common conservative position treats each closed position as short-term capital gain or loss on Form 8949; an alternative framework treats perps as swaps producing ordinary income. On offshore and DeFi venues, Section 1256 60/40 treatment is not available. Pick a framework, document it, and apply it consistently.

Do crypto perps qualify for Section 1256 60/40 treatment?

Not on offshore exchanges or DeFi protocols, which fail the qualified-exchange requirement outright. The new CFTC-approved onshore perps (Kalshi's BTCPERP, Bitnomial, Coinbase's US product) satisfy the exchange test, but whether perps clear the statute's swap exclusion is unproven and is being litigated. Onshore 60/40 is a documented position for some traders, not a default.

Did the 2026 CFTC approval of perpetual futures change how perps are taxed?

It changed the question, not the answer. Onshore perps listed on designated contract markets now clear the exchange prong of Section 1256, which offshore perps never could. But the IRS has issued no guidance, the swap-exclusion question is in federal court after CME sued the CFTC, and no established broker reporting practice exists yet.

How are funding payments on perps taxed?

There is no direct IRS guidance. The conservative treatment reports net funding received as ordinary income, while funding paid is generally a disallowed investment expense for investors. Alternative approaches net funding into position P&L or into a single annual ordinary figure. Document whichever method you use and stay consistent.

Is getting liquidated a taxable event?

Yes. A liquidation is a forced disposition of your position, and the margin you lost (including liquidation fees) is a realized loss with the same character as your other perp losses. It is not a theft or casualty loss, and skipping liquidations in your records overstates your taxable income.

Is converting BTC to USDC to fund a margin account taxable?

Yes. Converting any appreciated crypto into a stablecoin is a disposal of the crypto, with capital gain or loss measured against your basis at that moment. Funding a perp account this way can create a large taxable gain before you place a single trade, and a US exchange will report the proceeds on a 1099-DA.

Do Binance, Bybit, or dYdX report my perp trading to the IRS?

No. Offshore exchanges that exclude US persons file nothing with the IRS, and DeFi protocols file nothing and never will after the DeFi broker rule was repealed in 2025. Your activity is still fully taxable, and your first paper trail is usually a 1099-DA from whatever US exchange you fund or cash out through.

Will I get a 1099 for trading the new onshore perps like Kalshi's BTCPERP?

The reporting posture for the 2026 onshore perp products is still forming. Traditional futures get a 1256-formatted 1099-B from brokers, but do not assume the new perp venues will report that way for 2026. Keep complete records of your own regardless of what arrives in January.

Does the wash sale rule apply to crypto perps?

Under current law, no. The wash-sale rule covers securities, and both crypto held as property and cash-settled perp positions sit outside it, so losses are generally deductible even with immediate re-entry. Proposals to extend the rule to digital assets keep circulating, so confirm the current-year status before harvesting.

Do I need to file an FBAR for a Binance or Bybit account?

Maybe. Under current guidance, a foreign exchange account holding only crypto has not been FBAR-reportable, but an account that ever holds fiat can be, and FinCEN has long signaled it intends to bring crypto accounts into the regime. Form 8938 is a separate, broader analysis. For material offshore balances, disclosure is the conservative posture; review it with your preparer.

What if I never withdrew my perp profits to a bank?

You still owe tax. Gain is realized when positions close, funding is received, and collateral is converted, not when dollars reach your bank account. Never cashing out changes your visibility, not your liability, and the blockchain and exchange records preserve the history indefinitely.

What tax forms do I use to report perpetual futures?

Under the conservative capital framework: Form 8949 and Schedule D for position P&L and collateral disposals, Schedule 1 for net funding received, and a Yes on the Form 1040 digital asset question. Form 6781 only enters the picture for a documented Section 1256 position on onshore contracts, ideally paired with a Form 8275 disclosure.

About the author

Garrett Taylor, CPA

Former Big Four CPA. CPA #133092. Garrett answers his phone. Led by expertise. Powered by precision.

Related Articles

Hyperliquid Taxes (2026): A CPA's Guide to Perps, Funding Payments, and the Airdrop the IRS Never Saw

Hyperliquid issues no tax forms and the IRS has no perp guidance. A CPA covers perps, hourly funding, the HYPE airdrop, and a full worked year with real numbers.

Section 1256 and Event Contracts (2026): Do Kalshi and Prediction Markets Get 60/40 Treatment?

Section 1256's 60/40 rate could cut a prediction market trader's federal bill by a quarter, but no platform reports event contracts that way. A CPA walks the statutory test, the math, and the Form 6781 and Form 8275 mechanics.

I Got a 1099-DA, Now What? A CPA Walks Through Every Box (2026)

Form 1099-DA reports your crypto proceeds to the IRS, usually with no cost basis. A CPA explains every box, what to do before filing, and when to amend.

Crypto Options Taxes (2026): A CPA's Guide to Premiums, Exercise, Assignment, and the 60/40 Question

Deribit options, IBIT covered calls, and CME futures options are taxed three different ways. A CPA prices premium, exercise, expiry, and assignment, and settles the 60/40 question per instrument.